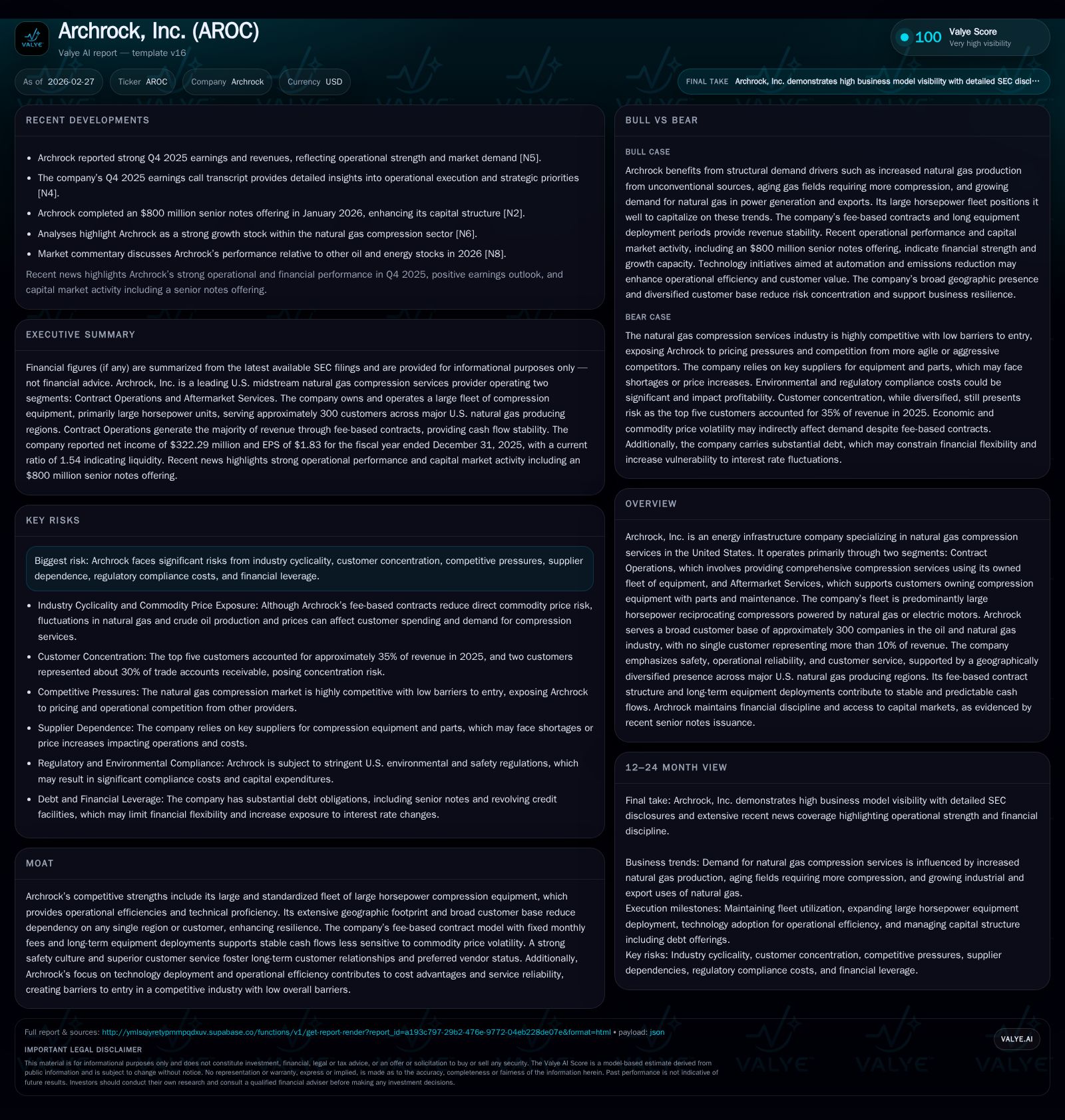

Archrock, Inc. Expands Stable Fee-Based Operations Driving Strong Cash Flow Amid Market Volatility

Archrock leverages its large horsepower fleet and diversified customer base to capitalize on natural gas compression demand growth, supported by robust capital discipline.

Archrock, Inc. specializes in natural gas compression services with a focus on a fee-based contract model that provides revenue stability and resilience against commodity price fluctuations. The company has delivered steady profitability growth and substantial improvements in operating cash flow, underpinned by operational efficiencies and strategic fleet management. Archrock plans to grow contract operations organically and through acquisitions while maintaining financial strength and investing in technology to enhance reliability. Capital allocation prioritizes dividends and share repurchases, reflecting confidence in long-term cash flows despite cyclicality inherent in the energy industry.

Company Overview

Archrock, Inc. is an established energy infrastructure company focused on midstream natural gas compression services across the United States. Its primary business segments include Contract Operations—which involves designing, sourcing, owning, installing, operating, servicing, repairing, and maintaining a large fleet of natural gas compression equipment under fixed-fee contracts—and Aftermarket Services that support customers owning their own compression equipment through maintenance and parts sales [S1][S6][S16].

The company's compressor fleet is predominantly composed of large reciprocating compressors powered by natural gas or electric motors, with approximately 74% of operating horsepower sourced from units rated above 1,000 horsepower [S13][S16].

Serving around 300 customers primarily within the oil and natural gas sectors, Archrock benefits from a diversified revenue base where no single customer accounted for more than 10% of consolidated revenues in 2025. Its geographic footprint spans key U.S. producing basins including the Permian and Eagle Ford shales, enabling flexible equipment redeployment and mitigating regional concentration risks [S7][S8].

Historical Performance and Growth Drivers

Financial data reveals strong growth momentum over recent years:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 322 | 622 | 502 | +87.1% |

| 2024 | 172 | 430 | 359 | +64.0% |

| 2023 | 105 | 310 | 299 | +137.0% |

| 2022 | 44 | 203 | 240 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 37 | 70 | 120 |

| 2024 | 31 | 13 | 71 |

| 2023 | 24 | 9 | 12 |

| 2022 | 2 | -36 |

Source: SEC companyfacts cache [F1].

Net income increased approximately 87% year-over-year from $172 million in 2024 to $322 million in 2025 [F1], driven by increased service volumes and operational leverage within contract operations [N3][N4]. Operating cash flow similarly surged nearly 45%, supporting significant capital investments that raised capex by almost 40% [F1]. This expansion aligns with management’s strategy to redeploy idle compressor units profitably and add new horsepower responding to growing natural gas production trends in unconventional plays [S20][S26].

Business Model: Fee-Based Contract Operations

Archrock’s contract operations segment relies on a fee-based model where customers pay fixed monthly fees over an average six-year compressor deployment period regardless of commodity price fluctuations or intermittent production downtime. During periods of limited gas flow, reduced fees apply but contracts remain intact ensuring stable revenue streams [S6][S8].

This approach minimizes direct exposure to oil and natural gas price volatility—a notable advantage given the cyclical nature of the energy sector—and enhances predictability for both Archrock’s cash flows and its customers’ operating costs [S6][S17].

The Aftermarket Services segment complements contract operations by providing maintenance services and parts sales to customers who own their compressors directly, contributing roughly 15% of total revenue recently [S13][S16].

Competitive Strengths

Archrock holds a leading position as the largest owner/operator of large horsepower outsourced compression equipment in the U.S., benefiting from a standardized fleet design that reduces maintenance complexity and cost while improving uptime [S13][S16]. The predominance of units exceeding 1,000 HP aligns well with industry demand driven by increasing associated gas volumes from shale production.

The company’s geographically diversified asset base—including major basins such as Permian and Eagle Ford—reduces concentration risk while enabling operational flexibility [S8][S13]. A strong safety culture reflected in a low total recordable incident rate (TRIR) of 0.22 during 2025 enhances customer confidence and supports preferred vendor status amid competitive pressures characterized by low entry barriers but high technical requirements [S13][S27].

Technological investments focus on integrating telematics for predictive maintenance along with digital tools for field technicians aimed at increasing labor productivity and reducing fuel consumption through optimized routing—measures that improve operational margins [S26].

Industry Context & Dynamics

Natural gas compression is essential midstream infrastructure facilitating continuous transport through gathering systems challenged by declining reservoir pressures as fields mature alongside pad drilling trends requiring larger capacity units. Rising gas-to-oil ratios further support aggregate compression demand despite upstream activity cyclicality .

While commodity price fluctuations impact upstream producer budgets indirectly affecting service volumes, Archrock’s fee-based contracts provide insulation against direct price exposure though maintaining high fleet utilization remains critical for growth [S27]. Regulatory developments focused on emissions reductions pose compliance costs but may also stimulate aftermarket service opportunities.

Financial Position & Capital Structure

Archrock demonstrates solid liquidity with a current ratio near 1.54 at December 31, 2025 indicating sufficient short-term asset coverage over liabilities [F1]. The company’s debt profile includes multiple senior note issuances maturing primarily between the late-2020s and early-2030s providing manageable refinancing schedules without near-term spikes in obligations [S4][S5][S14].

Its revolving credit facility offers working capital flexibility supporting operational needs and potential acquisitions . Prudent leverage management balances investment requirements against cyclicality risks inherent to its sector.

Growth Prospects & Outlook

Management expresses optimism regarding sustained demand growth driven by increasing U.S. unconventional natural gas production paired with emerging consumption applications such as power generation for AI data centers and LNG exports [N2][N6][N7][S20][S26]. The strategy focuses on organic expansion via reactivation of idle horsepower assets complemented by targeted acquisitions that densify geographic presence or enhance aftermarket capabilities [N3][N4][S26].

Technological enhancements are expected to further improve asset availability supporting volume growth without proportional cost increases.

No formal forward guidance is provided at this time; however, key metrics to monitor include contract renewal rates for large horsepower units across core shale regions and margin improvements linked to technology adoption.

Capital Allocation Review

Free cash flow generated (~$120 million after capex) supports disciplined capital returns comprising incremental dividend increases alongside materially expanded share repurchases ($70 million versus $13 million the prior year) signaling confidence in sustainable earnings power underpinned by fee-based contracts [F1][S15].

Capital expenditures have increased substantially (~40% YoY), primarily directed towards expanding operational fleet capacity consistent with favorable market fundamentals while investing in technology upgrades enhancing efficiency profiles [F1][S10][S26].

There is no indication of recent large-scale inorganic transactions beyond prior NGCS acquisition integrations; organic growth remains a priority.

Risks To Monitor

Key risks include exposure to industry cyclicality despite mitigants from fixed fee arrangements; customer concentration risk albeit moderated by diversified client base; supplier dependencies balanced against alternative sourcing; evolving regulatory frameworks potentially increasing compliance costs; and financial leverage necessitating ongoing liquidity vigilance amid market volatility [S27][S7][S9][S17][S19].

Environmental regulations introduced recently present uncertainty regarding cost impacts though current compliance status appears robust without imminent material adverse effects projected [N1][S27].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments