ASPAC II Acquisition Corp.: Evaluating SPAC Viability in High-Tech Acquisition Targets

An analysis of ASPAC II Acquisition Corp.’s financial and operational profile amid a challenging SPAC environment focused on technology-driven ESG targets.

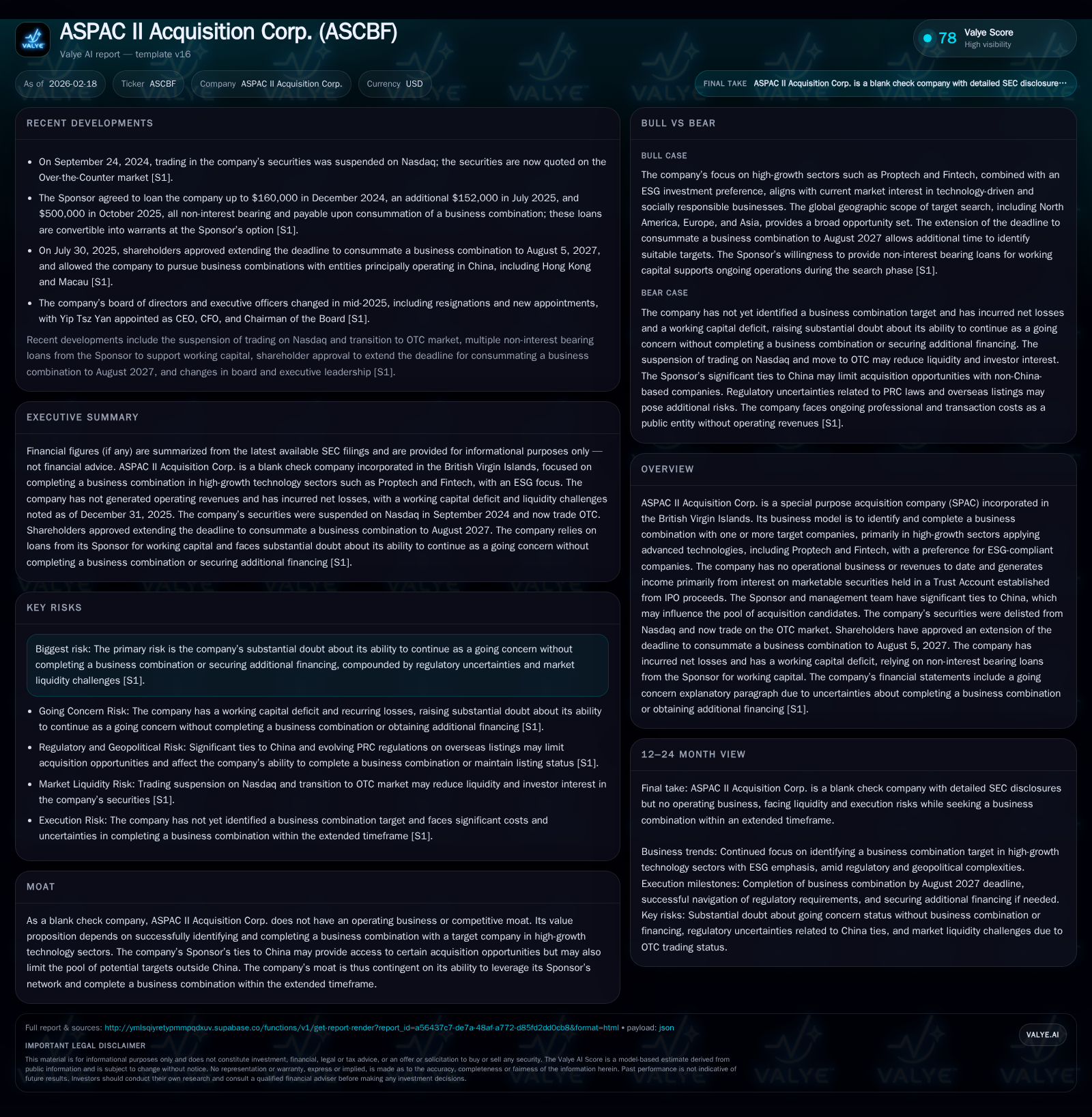

ASPAC II Acquisition Corp., a British Virgin Islands-incorporated SPAC with strong China ties, targets high-growth Proptech and Fintech sectors emphasizing ESG compliance. The company faces significant hurdles including regulatory uncertainties stemming from China’s tightened oversight of overseas listings, ongoing liquidity strains, and management changes that reflect strategic recalibration. Despite an extension to August 2027 to complete a business combination, the absence of announced targets and working capital deficits raise concerns about viability without additional financing or a successful deal. Monitoring forthcoming deal announcements and shareholder votes will be critical to assessing ASPAC II’s prospects.

Profile of a SPAC with China Ties and ESG Focus

ASPAC II Acquisition Corp. is a special purpose acquisition company incorporated in the British Virgin Islands designed exclusively for effecting one or multiple business combinations. Its mandate prioritizes technology-driven industries—principally Proptech and Fintech—with an explicit Environmental, Social and Governance (ESG) focus. This thematic selection aims to capitalize on continuous breakthroughs at the intersection of innovation and sustainability principles.

Crucially, the company's sponsor group maintains significant connections to mainland China; all officers and directors are based there. This geographic affiliation uniquely positions ASPAC II to access certain acquisition targets embedded within or affiliated with China’s high-tech ecosystem. However, it simultaneously narrows the overall candidate universe due to geopolitical tensions and investor skepticism toward China-linked SPACs. Consequently, ASPAC II's growth potential depends heavily on its sponsor network's effectiveness amidst complex cross-border transaction dynamics [S1].

Historical Operating Performance and Financial Trends

As a blank check entity without active operational assets or revenues, ASPAC II generates income primarily from interest accrued in its Trust Account established at IPO. Over time, operating losses have slightly receded—from $842k negative in FY2023 down to $347k negative by FY2025—indicating incremental control over administrative burn rate but persistent structural costs related to maintaining public status and pursuit activities [F1].

Net income shows notable volatility: while calendar year 2023 reflected an anomalous profit largely attributable to nonrecurring factors ($5.4m positive), subsequent reporting reverted to net losses of $224k in FY2025. This oscillation underlines inherent unpredictability absent business combination proceeds or recurring operations.

Operating cash flow (CFO) remains consistently negative (-$363k in 2025), emphasizing ongoing cash burn exceeding inflows despite interest income from safe government securities investment yielding modest returns constrained by historically low Treasury yields post-IPO capital deposition [F1][S9].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 0 | -363076 | -347251 | -244.8% |

| 2024 | 0 | -461166 | -610857 | -97.1% |

| 2023 | 5 | -621690 | -842030 | +122.5% |

| 2022 | 2 | -438591 | -424790 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 2.9 |

| 2024 | -2.1 |

| 2023 | -81.4 |

| 2022 | -41.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue data is not available in provided tags; dividend payments and capital expenditures are also not disclosed.

Management Overhaul and Corporate Governance Shifts

Mid-2025 marked a pronounced governance pivot when four board members resigned simultaneously along with the CEO and CFO stepping down subsequently. Their replacements included individuals closely linked with the Sponsor's base in Asia, consolidating control under new CEO/Chair Yip Tsz Yan (appointed concurrently as CFO). Indemnity provisions were renewed consistent with prior filings.

These leadership changes are interpreted as strategic recalibrations reacting to operational setbacks— notably the Nasdaq delisting due to insufficient shareholder count—and the pressing need to revitalize acquisition initiatives under heightened regulatory headwinds [S1]. The refreshed board composition underscores intent for tighter oversight but also concentrates decision-making authority within a narrow sponsor-aligned group.

Capital Structure: IPO Proceeds, Trust Account Holdings, and Sponsor Loans

ASPAC II’s $203.5 million IPO proceeds plus private placement warrant financing are held largely in a U.S. Treasury-backed Trust Account yielding nominal interest income dedicated solely to fund an eventual business combination or redeem outstanding public shares if liquidated.

Sponsor-provided non-interest-bearing promissory notes totaling approximately $292k outstanding as of year-end 2025 offer incremental liquidity for operating expenses ahead of a closing deal; these loans carry conversion provisions into warrants at $1 per unit mirroring Public Warrants' terms—an arrangement typical of "sponsor bridge loans" serving as backstop working capital with attendant dilution risk upon conversion.

No long-term debt exists beyond these elements; however, cash externally available (outside Trust Account) is minimal (~$135 at YE25), evidencing compressed runway amid continuing professional costs associated with remaining public status and deal pursuit activity [S4,S6,S7,S9].

Business Combination Prospects: Opportunities and Constraints

Target sector preference remains fixed on tech-enabled Proptech and Fintech ventures that align with global ESG trends—a thematic attractive both strategically and for investment appeal. Geographically diversified searches span North America, Europe, and Asia; yet regulatory constraints tied to PRC policies limit operational flexibility through compliance gatekeeping mechanisms.

Meaningful challenges arise from the interplay between geopolitical risk overlay affecting China-focused transactions and tightened regulatory gating factors demanding upfront filings for overseas listings triggered by CSRC’s New Administrative Rules effective March 31st 2023—introducing procedural complexity seldom faced by western peers [S1]. This crimp on target deal flow adds execution uncertainty.

Regulatory Landscape Influence on Acquisition Scope

Recent PRC reforms establish stringent oversight over domestic entities planning overseas offerings—including those potentially acquired via foreign structures like SPACs—mandating CSRC approval filings plus confidentiality obligations on accounting archives not previously codified formally.

These rules increase compliance burdens exponentially for any merger partner rooted or heavily exposed within China’s jurisdictional ambit. Noncompliance risks range from transaction delays to outright prohibition or reputational fallout impacting investor appetite post-acquisition announcement [S12].

Such legal environments critically shape ASPAC II’s ability to complete a qualifying business combination without extensive due diligence delays or governmental intervention.

Liquidity Challenges and Financial Sustainability Risks

The company’s balance sheet reveals acute working capital deficits (~$645k negative at year-end 2025) against negligible liquid cash outside Trust Account reserves designed exclusively for shareholder redemptions absent combination closure. Operating outflows into professional fees persist unabated requiring external lender support solely via Sponsor promissory notes.

Absent timely completion of a business combination or fresh capital injections from secondary financings—which currently lack commitment—the Company faces triggering automatic wind-up clauses mandated under its amended charter upon expiration of the extended deadline (August 5, 2027). This represents classic "runway compression" wherein funding scarcity intersects ticking deadline-induced "wind-down triggers" absent transformative corporate events [S6,S12,F1].

What to Monitor: Key Milestones Ahead of the August 2027 Deadline

ASPAC II shareholders have ratified a deadline extension granting nearly two additional years beyond initial windows—a recognition of market turbulence particularly impacting China-oriented SPACs post regulatory clampdowns.

Critical near-term milestones include announced identification of viable merger candidates matching sector/geography filters coupled with formal proxy solicitations for shareholder votes required under SEC tender offer rules if redemption opt-outs arise. Failure to identify credible merger target(s) sufficient to secure equity-backed financing would precipitate forced trust liquidation deleterious both financially and reputationally [S1].

Thus deal pipeline visibility becomes paramount alongside observing related party loans usage patterns signaling liquidity health.

Capital Allocation Framework Under Uncertainty

With no operating revenues or dividend distributions—typical across SPAC lifecycle pre-combination—capital allocation has been conservatively confined mainly to covering sustained G&A expenses funded either by trust interest income or incremental working capital loans provided by sponsors convertible into options/warrants representing future dilution vectors where investments remain unconsummated.

Redemption rights embedded within Public Shares further imply potential rapid unwinding upon failure scenarios restricting surplus deployment flexibility maintaining capital preservation strategy via strict expenditure controls until definitive merger closure outcomes materialize [F1,S17,S22,S25]. Note that specific dividend payments or share buyback programs are not disclosed in available data.

Conclusion: Strategic Imperatives for Survival and Value Creation

ASPAC II Acquisition Corp.’s current snapshot outlines an archetype SPAC contending with compounded challenges across governance reset phases, regulatory tightening particularly affecting Chinese ties, operational liquidity headwinds evidenced by widening working capital deficits paired with slender external cash buffers.

While extension till August 5, 2027 offers breathing room uncommon among early-deal SPACs forcibly wound down sooner, absence of disclosed acquisition targets alongside deteriorating operating metrics elevates execution risks markedly.

Success requires astute management leveraging sponsor relationships effectively coupled with timely identification of synergistic high-growth ESG-compliant businesses robust against jurisdictional scrutiny pressures—otherwise liquidation looms inevitable as foundational financial fragility persists unmitigated beyond planned deadlines [S1,F1].

Disclaimer: This analysis is based solely on publicly available information including SEC filings as of February 18, 2026. It does not constitute investment advice or recommendations regarding ASPAC II Acquisition Corp.'s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments