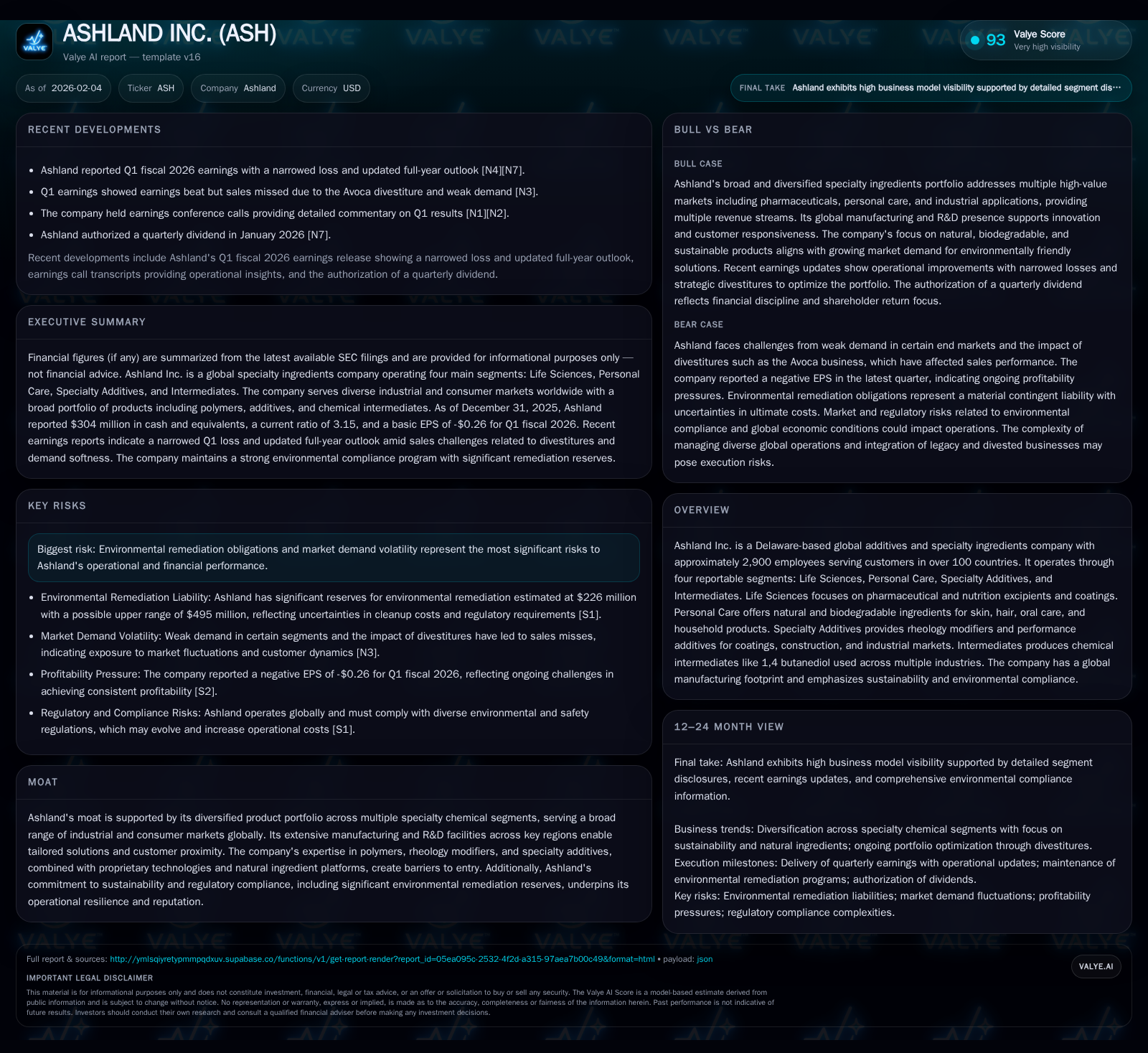

Assessing Ashland Inc.'s Resilience Amid Market Volatility Post-Q1 2026 Earnings

Ashland demonstrates operational robustness through diversified specialty chemical segments despite sales pressures and environmental cost considerations.

In Q1 2026, Ashland Inc. reported earnings that exceeded expectations, counterbalancing weaker sales impacted by the Avoca divestiture and softer demand in industrial markets. The company’s four distinct segments—Life Sciences, Personal Care, Specialty Additives, and Intermediates—provide a portfolio balance that buffers volatility inherent in raw material and end-market cycles. Sustained innovation in Life Sciences and a strategic pivot towards sustainability in Personal Care underscore Ashland’s adaptive approach amid sector headwinds. Meanwhile, environmental remediation obligations present ongoing financial and reputational challenges. Looking ahead, Ashland narrows its full-year outlook but remains focused on technology-driven differentiation, regulatory compliance, and capital discipline.

Decoding Q1 2026: Earnings Beat but Sales Headwinds

Ashland Inc.’s latest quarterly disclosure revealed a nuanced performance picture: earnings came in ahead of consensus expectations even as sales missed estimates primarily due to the completed divestiture of its Avoca nutritional ingredient business and sluggish demand in cyclical industrial markets [N1][N3][N5][N6][N9][S2]. The Avoca divestiture trimmed aggregate revenue but sharpened the company’s focus on higher-margin core segments. Operational excellence and cost controls enabled Ashland to maintain profitability above forecasts despite these headwinds.

During the Q1 earnings call, management emphasized resilience rooted in diversified end-markets and detailed how margin management partly offset volume softness [N1][N3]. This dynamic underscores a key theme: while certain top-line pressures persist, Ashland's agile segment mix enables sustained earnings quality.

Segment Spotlight: Life Sciences Through the Lens of Innovation and Challenges

The Life Sciences division remains a cornerstone for Ashland, delivering pharmaceutical excipients such as controlled release polymers, disintegrants, tablet coatings, binders, thickeners, and solubilizers that serve a broad spectrum of drug formulation needs [S1][F1]. Despite the August 2024 nutraceutical business sale reducing segment scale somewhat, the focus has intensified on innovation within pharmaceutical excipients—where tailored solutions meet stringent regulatory standards.

This segment’s exposure to pharmaceutical manufacturers ensures continued demand stability relative to more cyclical markets yet is not immune to pricing pressures or product lifecycle risks. Ongoing R&D investment into polymer chemistry aims to deepen differentiated offerings while addressing evolving patient-centric drug delivery modalities.

Personal Care’s Pivot: Sustainability Meets Consumer Trends

Ashland’s Personal Care unit exemplifies strategic alignment with global megatrends emphasizing naturalness and biodegradability [S1][F1]. The segment's portfolio includes biofunctionals, microbial protectants (preservatives), skin care ingredients, sun care components, oral care actives, hair care formulations, and biodegradable household solutions.

This shift toward nature-derived rheology modifiers and environmentally conscious additives not only resonates with consumer preference shifts but dovetails with Ashland's broader environmental compliance ethos. The unit services both multinational brand formulators and boutique innovators seeking high-performance yet sustainable ingredients.

Specialty Additives and Intermediates: Navigating Industrial Market Volatility

Specialty Additives provide rheology modifiers critical for architectural paints, coatings, construction compounds like dry mortars and joint compounds, as well as industrial applications spanning automotive components to ceramics used in electronics [S1][F1][N3]. Meanwhile, Intermediates chiefly produces 1,4-butanediol (BDO) and related derivatives integral across chemical manufacturing chains.

Both segments remain vulnerable to cyclicality inherent in construction activity levels and industrial capex cycles. Q1 softness reflected this exposure as global macroeconomic uncertainties restrained end-demand [N3]. Nonetheless, products’ technical complexity offers some insulation versus commoditized chemicals.

The Moat Unpacked: Technology, Global Reach, and Regulatory Fortitude

Ashland’s competitive advantage emerges from a confluence of proprietary technologies—especially in polymers and rheology modifiers—a geographically diverse manufacturing footprint providing customer proximity globally, and deep expertise navigating complex regulatory landscapes [valye_report_excerpt.moat][S1].

The company’s investment in patented formulations secures differentiated performance benefits that support pricing integrity. Moreover, sustainability commitments reinforced by substantial environmental remediation reserves build trust among customers increasingly focused on supply chain transparency and legal compliance.

Together these factors form tangible barriers deterring new entrants or commoditization risks within core specialties.

Balancing Act: Environmental Liabilities Amid Growth Ambitions

A pivotal tension for Ashland resides in balancing ambitious growth targets against substantial environmental remediation obligations [S1][valye_report_excerpt.risks]. The company maintains sizeable reserves earmarked for cleanup activities linked to legacy operations—a reflection of proactive risk management yet a source of financial strain.

These liabilities impose additional costs which could pressure margins or capital deployment flexibility if remediation efforts extend or escalate unexpectedly. However, transparent acknowledgement of these responsibilities buttresses corporate reputation among regulators and stakeholders sensitive to sustainability credentials.

Capital Discipline: Dividend Policy and Financial Health Analysis

At fiscal year-end 2025 closing on December 31st, Ashland reported strong liquidity with cash & equivalents totaling approximately $304 million USD against current liabilities near $366 million USD—yielding a robust current ratio around 3.15 [F1]. This solid position enabled confidence in maintaining dividend payments per recent board authorization despite narrowed full-year guidance [F1][N10].

Management’s capital allocation reveals discipline: prioritizing shareholder returns balanced against reinvestment opportunities aligned with long-term strategy execution amid uncertain macro conditions.

Outlook in Focus: Narrowed Guidance and Strategic Responses

Following Q1 disclosures highlighting sales softness amid external headwinds including the Avoca divestiture effect and cyclical weakness within industrial-facing segments, Ashland revised its full-year outlook downward [N6][N9].

Management commentary articulated intentions to emphasize operational efficiency improvements while selectively advancing innovation pipelines within Life Sciences and Personal Care units. Caution permeates forecasts given persistent demand unpredictability; nonetheless strategic recalibration aims to shield core profitability drivers from broader volatility.

Risks Revisited: Volatility, Acquisitions, and Operational Disruptions

Reaffirming previous disclosures from the FY2025 Annual Report [S1], key risks center on market demand swings exacerbated by geopolitical tensions or macroeconomic slowdowns impacting customer sectors such as construction or pharmaceuticals. Additional concerns stem from potential acquisition integration hurdles that may dilute anticipated synergies or impose unexpected expenses.

Operational risks warrant particular attention given natural catastrophe exposures inherent in chemical production environments combined with supply chain fragilities illuminated during recent global disruptions [S1]. Although insured against certain events, insurance coverage gaps remain possible.

Overall risk management remains integral to safeguarding ongoing financial performance beyond near-term results.

This analysis is based on information available as of early February 2026 including Q1 earnings reports, SEC filings through the latest quarterly results filing, company disclosures, and relevant industry context. It does not constitute investment advice or recommendations but aims to provide an informed synthesis reflecting Ashland Inc.'s current positioning amid evolving market dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments