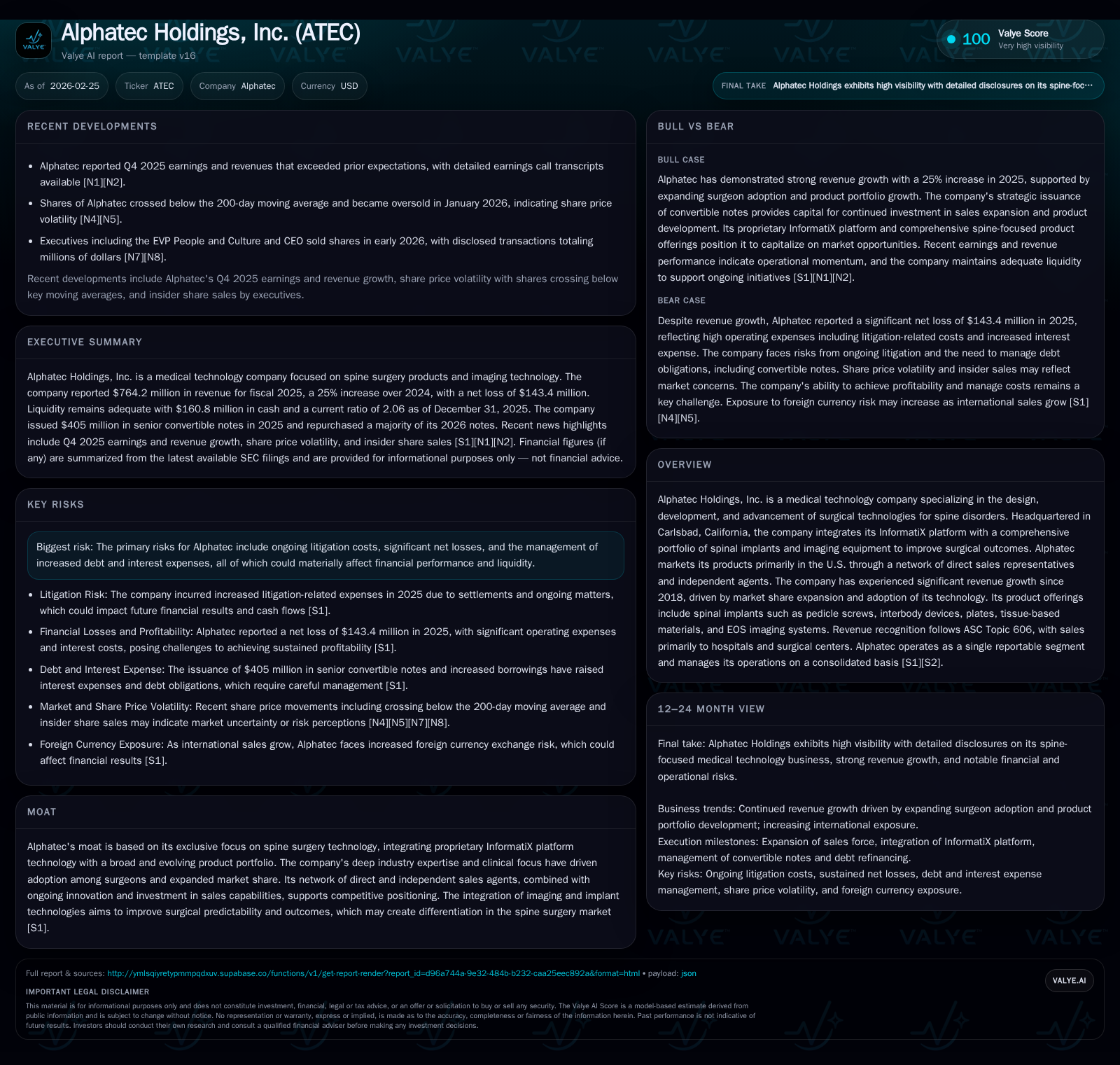

Alphatec Holdings' Revenue Rebound and Innovation Edge in Spine Surgery

Alphatec’s specialized spine surgery platform delivers strong revenue growth and improving cash flows amid capital structure complexities.

Since its 2018 transformation, Alphatec Holdings has accelerated revenue growth at a roughly 35% CAGR, powered by clinical adoption of its InformatiX platform integrated with a broad portfolio of spinal implants and EOS imaging systems. The company has made significant strides in narrowing operating losses and generating positive operating cash flow in 2025, signaling operational leverage despite ongoing net losses. Its capital structure features $405 million senior convertible notes due 2030 alongside a revolving credit facility and term loans, all of which drive interest expense pressures. Looking ahead, Alphatec's success hinges on expanding surgeon access via exclusive sales teams and managing litigation costs and debt servicing challenges—key milestones to monitor include quarterly earnings updates and convertible note conversion dynamics.

Historical Growth Catalysts and Revenue Momentum Since 2018

Alphatec Holdings’ transformation beginning around 2018 set the stage for an impressive revenue trajectory characterized by approximately 35% compound annual growth. This acceleration is underscored by reported revenue growth from $23 million in Q3 2018 ([F1]) to a run-rate exceeding $700 million by FY2025 ([F1]). Central to this momentum is the expansion and adoption of its integrated InformatiX platform aligned with a comprehensive spine-focused product portfolio including pedicle screws—critical load-bearing implants used for spinal fixation—interbody devices, plates, tissue-based materials, and EOS imaging systems offering full-body weight-bearing x-rays enhancing surgical planning accuracy [S1].

The company's dual sales strategy leverages direct representatives supplemented by independent agents allowing broader national account penetration while maintaining clinical support effectiveness—this layered distribution network contributes to consistent market share gains [S1]. As surgeons increasingly validate Alphatec’s approach through clinical outcomes enhanced by embedded InformatiX decision support algorithms, adoption feeds a virtuous cycle boosting both unit volume and expanding aftermarket service revenue streams [S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -143 | 45 | -82 | 42 | +11.6% |

| 2024 | -162 | -45 | -136 | 83 | +13.1% |

| 2023 | -187 | -78 | -173 | 81 | -22.7% |

| 2022 | -152 | -75 | -147 | 49 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | -1153.7 | |

| 2024 | -128 | 1144.2 | |

| 2023 | 25 | -159 | -238.9 |

| 2022 | 25 | -125 | 414.4 |

Source: SEC companyfacts cache [F1].

Note: Operating cash flow YoY changes not computed due to negative-to-positive transition; CapEx reflects acquisitions of property, plant & equipment.

Innovative Spine-Centric Platform Fueling Market Share Gains

Alphatec’s strategic moat lies in its dedicated spine-only focus married with deep operational expertise driving clinical distinction—a term denoting meaningful improvements in patient outcomes based on precise surgical intervention metrics measured intraoperatively and post-op monitoring [S1]. The proprietary InformatiX platform integrates pre-operative planning data with intraoperative navigation enhancing surgeon confidence in implant placement accuracy (notably pedicle screw trajectory) while fostering predictability in complex cases.

Complementing software capabilities is an expansive hardware portfolio combining mechanical implants such as pedicle screws and interbody cages with advanced imaging devices like EOS systems that uniquely capture patient-specific spinal alignment under functional load conditions—a critical innovation not standard across most orthopedic firms [S1]. This integration addresses surgeons’ demand for comprehensive ecosystem solutions rather than piecemeal kits.

The company’s sales model emphasizing exclusive relationships engages clinically experienced sales personnel who understand nuanced procedure differentiation required for convincing high-volume spine surgeons to switch implants or adopt new instrumentation sets—a crucial driver behind market share gains in an otherwise commoditized implant sector where pricing transparency increases competitive pressures [N2][F1].

Financial Recovery: Operating Income and Cash Flow Improvement

Alphatec’s financial results reveal steady operational improvement with operating losses narrowing dramatically from -$173M in FY2023 to -$82M in FY2025 ([F1]). This roughly halving of the operating loss over two years evidences pronounced operating leverage as revenues scale faster than combined research & development plus selling/general administrative expenses.

Operating cash flow transitioned from negative $44.7 million in FY2024 to positive $45.2 million in FY2025 ([F1]), indicating improved collections efficiency and inventory management despite continued net losses (-$143M in FY2025) reflective of still significant investments into commercial infrastructure, litigation accruals, and interest expense burdens [N1][F1].

Capital expenditures reduced nearly by half year-over-year ($83M to $42M), reflecting a shift towards operational stability after prior heavy investment phases supporting new product launches and manufacturing capacity builds ([F1]). This suggests better free cash flow potential going forward though net income remains under pressure—calculating rough annualized return on equity yields strongly negative figures (~-1150%), highlighting the distance yet to profitability recovery [F1].

Dividends paid are not available from the provided tags; similarly, recent common stock buyback data are only available up to FY2023 and do not extend into the latest periods analyzed here ([F1]).

Debt Structure and Capital Raising: Navigating Convertible Notes and Credit Facilities

A pivotal element shaping Alphatec's financial flexibility is the issuance of $405 million senior convertible notes in March 2025 bearing an exceptionally low coupon rate of 0.75%, maturing March 2030 [S1][S19]. These notes replaced older higher-coupon convertible debt maturing sooner (2026 Notes), with partial repurchases reducing those obligations substantially (approximately $268 million repurchased). The new notes carry conversion terms starting around $15.54/share backed by capped call options that mitigate shareholder dilution upon conversion—an important feature for capital structure management [S24].

Further liquidity support stems from a revolving credit facility arranged with MidCap Financial Trust offering initial capacity of $50 million with an accordion up to $75 million secured principally by accounts receivable and inventory assets—the key working capital components within medical device firms managing complex instrument inventories and customer billing cycles [S4][S5]. Interest expense on this revolver approximated SOFR +3.5%, translating into about a mid-single-digit effective borrowing cost amid rising short-term rates ([S4]).

Additionally, the company carries a term loan facility totaling $200 million with Braidwell Transaction Holdings bearing SOFR plus roughly a 5.75% spread yielding over 9% effective rates as of late-2025 ([S16],[S17]). With combined outstanding debts exceeding half a billion dollars after discounts/issuance cost amortization (~$566 million net), interest burden absorbs substantial portions of cash flow leading to persistent net losses despite operational improvements [F1][S19].[S26]

The credit agreements include customary covenants focused on maintaining minimum liquidity levels along with lockbox arrangements on collections tied to the revolver ensuring lender protection but constraining financial agility somewhat—typical for specialized medtech companies balancing growth investments against financing costs [S4][S8].

Future Growth Potential and Key Operational Constraints

Looking forward, Alphatec seeks continued expansion primarily through adding clinically trained exclusive sales team members tailored towards penetrating underserved surgeons, hospitals, and national accounts across U.S markets—all vital for sustaining the momentum captured since the transformation began in 2018 [N2][S1]. Market access improvements are expected to increase surgeon adoption rates driving higher implant volumes.

Clinical distinction remains a core competitive advantage pushing surgeons’ preference for Alphatec’s integrated solutions over competitors providing isolated implant or imaging offerings alone—a sector nuance leveraging procedural efficacy as marketing leverage rather than pure price competition alone.

However, this growth vector competes against constraints linked to ongoing litigation costs which remain inherently uncertain both financially and timing-wise potentially weighing on resource allocation decisions alongside servicing rising debt-related interest obligations hampering near-term profitability expansions [S6][S1]. Sustained investment requirements for research & development plus commercial infrastructure imply continued capex outlays will be necessary though likely moderated given recent reductions ([F1]).

Without explicit forward guidance provided publicly ([N2]), monitoring emerging quarterly earnings details alongside evolving clinical adoption metrics will provide critical signals on whether Alphatec can maintain scalable growth absent further external funding or significant margin expansion.

Governance Signals: Insider Sales vs. Market Optimism

Notably, recent insider activity showed CEO selling shares valued above $2 million during a period when Alphatec’s stock surged approximately +126%, reflecting robust market enthusiasm possibly driven by operational momentum or refinancing optimisms ([N4]). Additionally, executive-level share disposals occurred around similarly strong price action including EVP People & Culture offloading approximately $679K worth of shares ([N8]).

Such insider liquidations must be assessed carefully within governance contexts: they may reflect personal portfolio diversification or tax planning rather than lack of confidence; still they provide balanced lens suggesting insiders perceive current valuations as opportunity points while retaining strategic stakes given no widescale board-level exits reported ([N7]). Stock price technicals showed periods crossing below long-term moving averages such as the 200-day moving average recently ([N6]) indicating some volatility amid optimism.

Monitoring Milestones: What to Watch in Upcoming Earnings and Market Penetration

In absence of formal forward guidance beyond historical disclosures ([N2],[S3]), investors should prioritize upcoming quarterly earnings reports focusing on revenue trends for newly launched implant lines plus utilization rates for EOS imaging systems evidencing deeper surgical integration or volume penetration gains ([N1],[N2]). Operating income versus consensus expectations will indicate if operating leverage gains persist.

Convertible notes conversion activity will also bear watching given potential share dilution implications versus balance sheet debt reduction merits discussed in recent filings ([S19],[S24]). Meanwhile, progression or resolution within litigation arenas normally disclosed during SEC periodic filings could materially affect contingency provisions impacting near-term earnings volatility ([S6]).

Cash flow generation relative to capex will remain essential benchmark guiding financial health alongside scrutiny of borrowing base utilization levels within the revolving credit facility indicative of working capital cycle dynamics—critical determinants for liquidity runway appraisal ([S4],[F1]).

Disclaimer: This analysis is intended solely for informational purposes derived from publicly available sources without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments