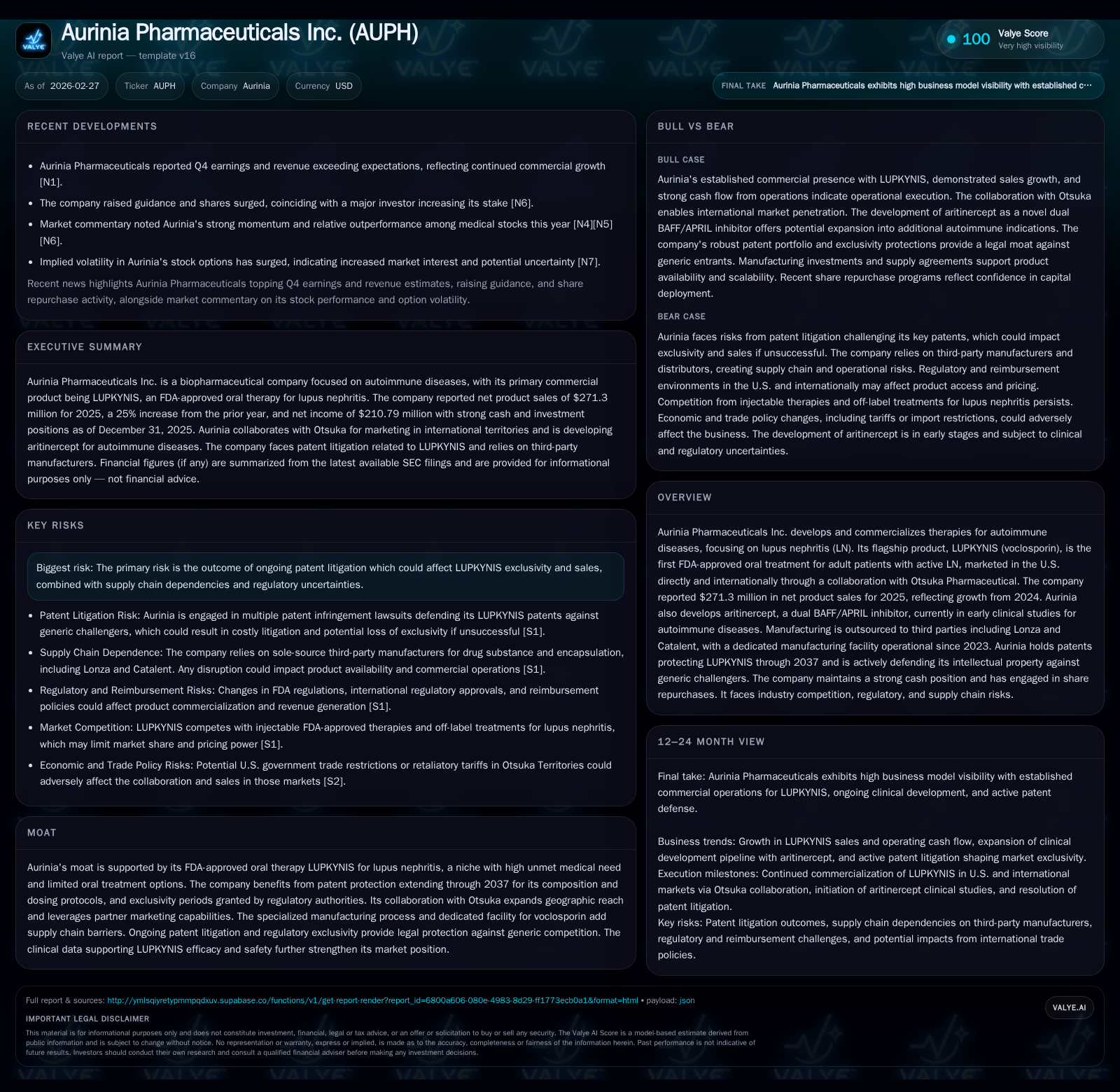

Aurinia Pharmaceuticals’ Growth Driven by LUPKYNIS Sales and Intellectual Property Defense

The company’s 2025 results reflect expansion in lupus nephritis treatment amid patent litigation and supply chain risks.

Aurinia Pharmaceuticals Inc. achieved a significant financial turnaround in 2025 with net product sales of LUPKYNIS up 25% year-over-year to $271.3 million, fueling its first positive operating and net income since prior losses. The oral lupus nephritis therapy benefits from patent protection through 2037 and collaboration with Otsuka for international commercialization, though ongoing patent litigation poses risk. Strong operating cash flow and aggressive share repurchases spotlight effective capital allocation but depend on maintaining sales growth and regulatory compliance.

Historical Performance and Revenue Drivers

Aurinia Pharmaceuticals’ financial trajectory highlights a pivotal shift in 2025 driven by its flagship product LUPKYNIS (voclosporin), an oral calcineurin inhibitor approved for the treatment of active lupus nephritis (LN) in adults. After several years of operating losses stretching back to at least 2022, the company reported operating income of $33.2 million and net income of $210.8 million for fiscal year ended December 31, 2025 [F1]. These figures represent a stark turnaround from losses recorded in prior years (operating losses ranging approximately -$29M to -$1.7M between 2022-24).

This change was underpinned primarily by surging net product sales: Aurinia posted $271.3 million for the year ended 2025 compared to $216.2 million in 2024—a robust growth rate of roughly +25% [N1][S25]. Revenues reflect both U.S.-based direct commercial efforts and shipments under collaboration agreements with Otsuka Pharmaceutical Co., Ltd., which handles marketing in Japan, Europe, and additional territories [S25]. The Otsuka relationship includes upfront payments plus royalties ranging from 10% to 20% based on net sales from those regions [S25].

Operating cash flow also swung positive materially to $135.7 million from $44.4 million in the prior year, indicating improved cash realization from growing sales alongside operational efficiencies [F1]. The current ratio of approximately 5.25 (current assets of $492M vs current liabilities of $93.7M) signals strong liquidity entering 2026 [F1]. Aurinia further reinforced shareholder returns by repurchasing $98.2 million worth of common shares during the calendar year—more than doubling from $40.2 million repurchased in 2024 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 211 | 136 | 33 | +14651.2% |

| 2024 | 1 | 44 | -2 | +105.3% |

| 2023 | -27 | -33 | -30 | -3.2% |

| 2022 | -26 | -80 | -28 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 98 | 36.3 |

| 2024 | 40 | 0.4 |

| 2023 | -7.1 | |

| 2022 | -6.4 |

Source: SEC companyfacts cache [F1].

*Revenue not disclosed within recent filings past initial years; main growth traced via reported figures.

Market Positioning and Moat Analysis

LUPKYNIS holds distinction as the first oral therapy approved by the FDA specifically for adult patients with active LN—a rare but severe manifestation of systemic lupus erythematosus affecting kidney function [S25]. The company markets LUPKYNIS directly within the U.S., while international rights are licensed to Otsuka who has secured approval in Japan, EU countries including the UK and Switzerland [S25]. This geographical spread broadens market exposure and leverages Otsuka's established commercial infrastructure.

The product enjoys patent protection extending through December 2037 covering composition claims and dosing regimens as listed in the FDA Orange Book; however, this exclusivity is actively challenged by generic entrants who have submitted Abbreviated New Drug Applications (ANDAs), invoking paragraph IV certifications alleging invalidity or non-infringement [S12][S20]. The resulting litigation is material; Aurinia has filed multiple patent infringement lawsuits in U.S district court defending these rights against large generics players like Hikma, Teva, Dr Reddy's and others [S12][S24].

Specialized manufacturing constitutes another moat element: outsourcing production primarily through Lonza Ltd., augmented by a dedicated voclosporin manufacturing facility activated since mid-2023 enhances supply chain resilience but also concentrates dependency on select partners [S25]. Any disruption could materially impair product availability.

On competition, despite LUPKYNIS being an oral option unique for LN, injectable treatments such as BENLYSTA (belimumab) by GSK and GAZYVA (obinutuzumab) by Genentech represent alternative FDA-approved therapies for LN patients often used alongside standard immunosuppressive regimens like mycophenolate mofetil (MMF) plus corticosteroids or tacrolimus off-label [S24]. Evolving prescribing habits favoring oral convenience versus parenteral administration will partially dictate growth velocity.

Future Growth Prospects

The future scalability rests on multiple levers:

- Market Penetration: Increased awareness and adoption within nephrology and rheumatology specialists could push expanded use beyond early adopters who have driven initial uptake onto stable LUPKYNIS prescriptions.

- Geographic Expansion: Maximizing commercialization efforts with Otsuka across Europe and Asia-Pacific regions where regulatory approvals exist will contribute incremental revenue streams.

- Pipeline Development: Aritinercept, a dual BAFF/APRIL inhibitor under early clinical evaluation targeting autoimmune diseases represents potential diversification beyond LN though it remains early stage without guaranteed commercial viability or timeline disclosures yet public [S25].

- Patent Litigation Outcomes: Maintaining exclusivity is paramount; adverse determinations could prompt generic launch accelerating price erosion sharply reducing LUPKYNIS’s revenue base.

- Health Policy Environment: Pricing pressures arising from legislation such as the Inflation Reduction Act impose new rebate obligations and pricing controls potentially constraining margins [S18][S19], while third-party payor reimbursement dynamics fluctuate amidst evolving formularies.

Regulatory Compliance and Risk Factors

Aurinia's operations are heavily regulated globally with compliance obligations spanning clinical trial conduct under Good Clinical Practice standards to marketing restrictions per FDA-approved labeling [S17]. The focus on an orphan indication limits market breadth but leverages expedited regulatory pathways facilitating initial launch speed.

Operational risks include dependence on third-party contract manufacturers whose cGMP compliance is subject to inspections that if failed could trigger recalls or sanctions impacting supply continuity [S17][S22][S24]. The company’s reliance on specialty pharmacies and distributors for patient access adds layers where contractual breaches or compliance failures could dampen sales performance.

Legal contingencies encompass:

- Product liability suits due to adverse reactions tied to LN severity or medication effects despite insurance coverage limitations possibly imposing financial strain should claims arise extensively [S13][S18].

- Intellectual property challenges threatening exclusivity duration given ongoing Hatch-Waxman litigations leveraging paragraph IV certifications filed since early 2025 against multiple generic drugmakers [S12][S20].

- Political-economic shifts such as investigations into pharmaceutical import security impacting cross-border supply chains given Aurinia's Canadian incorporation but reliance on Swiss-made APIs add geopolitical uncertainty [S14][S21].

Capital Allocation and Returns Analysis

Aurinia’s strong cash flow generation at $135.7 million CFO has supported aggressive repurchase programs totaling nearly $98 million during fiscal year-end December 31, 2025 [F1]. The balance sheet shows cash equivalents near $80 million complemented by significant liquid current assets granting operational flexibility into new development initiatives or continuing litigation expenses.

Return metrics reveal approximate return-on-equity near 36%, calculated as net income over equity base ($210.8M/$581M) reflecting highly profitable scale attained post-launch turnover improvements within a few short years after FDA approval [F1]. No dividend distributions are indicated suggesting prioritization of capital reinvestment along with buybacks for shareholder value enhancement.

Summary Assessment: What to Watch Forward

While explicit guidance is scarce beyond published milestones for aritinercept clinical progression or updates on patent litigation timelines, investors should monitor:

- Jury decisions or settlements regarding Hatch-Waxman litigations impacting LUPKYNIS exclusivity window.

- Sales trajectory quarter-over-quarter signaling deepening market penetration beyond early commercialization phases.

- Otsuka partnership progress reflected in royalty streams or milestone achievements expanding geographic reach.

- Regulatory developments altering drug pricing policies both domestically and internationally that could depress realized prices.

- Clinical advancement updates on pipeline assets expanding therapeutic breadth beyond lupus nephritis.

Maintaining competitive advantages rooted in intellectual property validity coupled with steady operational execution will be critical amid intensifying competition within autoimmune treatment modalities.

This report is prepared solely for informational purposes about Aurinia Pharmaceuticals Inc.’s business performance and industry context without providing any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments