Broadcom Inc: Strategic Advances and Financial Maneuvers in a Competitive Semiconductor Landscape

Broadcom is actively reshaping its AI and connectivity portfolio while managing elevated debt to capitalize on expanding AI infrastructure demand.

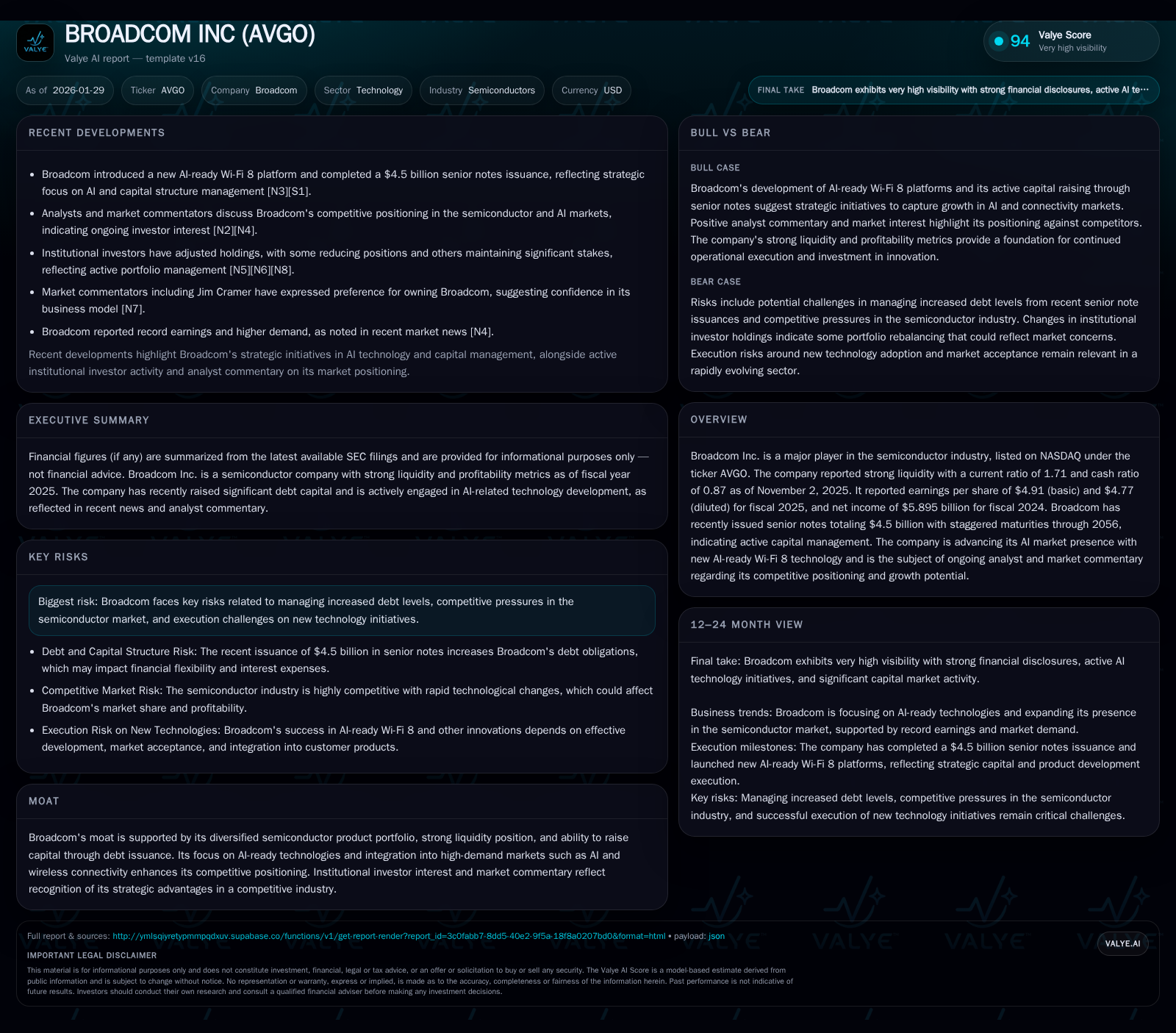

Broadcom reported record earnings driven by robust demand for its AI and connectivity chips, complemented by a sizable $4.5 billion senior notes issuance to support long-term capital needs. The company's business model synthesizes diverse semiconductor product lines with a focus on AI-ready solutions like Wi-Fi 8, targeting rapid growth segments. Its competitive strength derives from a broad product portfolio and integration into AI compute infrastructure, positioning it to capture a leading share of the custom AI chip market by 2027. Key risks include managing elevated leverage and execution on new technology rollouts amid intense semiconductor industry competition.

What Changed Recently

Broadcom has demonstrated strong operational momentum entering 2026, highlighted by record earnings reported in early January, driven by heightened demand in AI compute and networking infrastructure [N1]. Concurrently, the company completed a $4.5 billion senior notes offering across four tranches with staggered maturities from 2031 to 2056, reflecting a proactive approach to managing its capital structure and securing long-term liquidity [S6, S8]. This debt issuance underpins Broadcom’s strategic investments, particularly in AI-ready technologies such as its new Wi-Fi 8 platform designed to support next-generation AI workloads [N6].

Market commentary and analyst reports emphasize Broadcom’s strengthening position in the AI ecosystem, including projections that it will capture a dominant 60% share of the custom AI chip market by 2027, driven by its ASIC shipments expected to triple, signaling a significant ramp in production and design wins [N2, N3, N4]. However, there is also discourse cautioning against excessive valuation inflation driven by AI hype, reflecting a mixed but engaged investor base [N8, N9, N12].

Business Model as a System

Broadcom operates a complex semiconductor platform focused on designing, manufacturing, and selling a diversified portfolio of products spanning connectivity chips, custom ASICs, and infrastructure semiconductors. While detailed segment disclosures are limited in the latest filings, the company’s product mix is oriented toward high-value, specialized solutions integrated deeply into customers’ supply chains, notably in data centers, wireless infrastructure, and AI compute platforms [S1, S2].

This system leverages Broadcom’s proprietary design capabilities and scale manufacturing partnerships to deliver AI-ready technologies such as its Wi-Fi 8 platform, which supports increased bandwidth and low latency critical for AI data flows [N6]. The business model benefits from long-term contracts and strong customer relationships with hyperscalers and telecom operators, enabling predictable revenue streams and facilitating collaborative innovation. The issuance of senior notes serves as financial fuel to sustain R&D investments and capacity expansion necessary for competing in AI and next-generation semiconductors [S6, S8].

The integration of custom ASICs tailored for AI workloads positions Broadcom as both a chip designer and systems enabler, creating a moat through technology specialization and customer lock-in. Additionally, its broad product portfolio creates cross-selling and bundling opportunities across different hardware layers, enhancing its competitive advantage [Valye excerpt].

Industry Map & Competitive Battlefield

Broadcom operates within the highly competitive semiconductor industry characterized by rapid innovation cycles, high capital intensity, and significant customer concentration. Key competitors include established semiconductor giants and emerging AI chip startups targeting data center and edge compute markets. The AI semiconductor space is particularly dynamic, with customers demanding high-performance, energy-efficient custom chips and networking solutions.

Within this context, Broadcom’s competitive battlefield involves:

- Custom AI Chips: Positioned as a leading player targeting 60% market share by 2027, Broadcom competes with companies like Nvidia, AMD, and specialized ASIC providers. Its strategy focuses on leveraging scale and deep customer integration [N3].

- Connectivity & Infrastructure: Broadcom’s AI-ready Wi-Fi 8 platform and other connectivity solutions address growing demand for low-latency, high-throughput networking in AI applications, competing with companies like Intel and Qualcomm [N6].

- Capital and R&D Intensity: Maintaining technology leadership requires continuous investment in R&D and manufacturing capacity, often necessitating large capital raises and debt financing, which Broadcom has managed through recent senior note issuances [S6, S8].

The semiconductor industry’s cyclicality and supply chain dynamics also influence competitive positioning, with companies that can effectively manage capacity, costs, and customer relationships gaining advantage. Broadcom’s diversified product set and established ecosystem partnerships provide resilience against market volatility.

Where the Economics Become Real

Broadcom’s unit economics hinge on its ability to design specialized semiconductors that command premium pricing due to performance and integration benefits. Custom ASICs for AI workloads involve complex design cycles and high non-recurring engineering costs but yield higher margins once in volume production. The company’s scale and intellectual property portfolio help dilute these fixed costs over larger shipments, improving profitability.

Connectivity products, such as AI-ready Wi-Fi 8 chips, operate in competitive markets with pressure on ASPs (average selling prices) but benefit from increasing demand driven by AI infrastructure deployment. Margins here depend on manufacturing efficiency and supply chain optimization.

Financially, Broadcom’s liquidity position—with a current ratio of 1.71 and substantial cash reserves ($16.18 billion)—provides operational flexibility [Valye excerpt]. However, the recent $4.5 billion senior notes issuance adds leverage, exposing the company to interest expense and refinancing risks, especially in a rising rate environment [S6, S8]. The notes carry coupons from 4.3% to 5.7%, maturing over 30 years, reflecting a long-term debt tenor designed to balance current capital needs with future repayment profiles.

Execution risks involve scaling ASIC production rapidly amid supply constraints, sustaining R&D productivity to stay ahead in AI innovation, and managing pricing dynamics in a highly competitive semiconductor market.

Diligence Questions / Disconfirming Signals

- How sustainable is Broadcom’s projected 60% share in the custom AI chip market given intensifying competition from incumbents and startups?

- What are the operational risks and timelines associated with scaling ASIC shipments to triple, and how might supply chain disruptions impact this?

- How effectively can Broadcom integrate new AI-ready products like Wi-Fi 8 into existing customer ecosystems without cannibalizing legacy revenue?

- What is the company’s strategy and risk management approach to servicing and refinancing the $4.5 billion senior notes amid potential macroeconomic shifts?

- How resilient is Broadcom’s revenue base to semiconductor cyclicality, and what are the customer concentration risks, particularly in hyperscaler accounts?

- Are there any early signals of margin pressure from pricing competition or rising input costs that could challenge profitability?

- How does Broadcom’s R&D expenditure compare to peers in the AI semiconductor space, and is it sufficient to maintain technology leadership?

This analysis is based solely on publicly available information and recent news disclosures. It does not constitute investment advice or recommendations. Readers should consider multiple sources and conduct independent due diligence before forming conclusions about Broadcom Inc or the semiconductor industry.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments