Baxter International's 2025: Navigating Recall Crisis and Supply Chain Turbulence

Baxter’s operational setbacks in 2025 exposed vulnerabilities yet underscored resilient financial and strategic responses shaping its recovery trajectory.

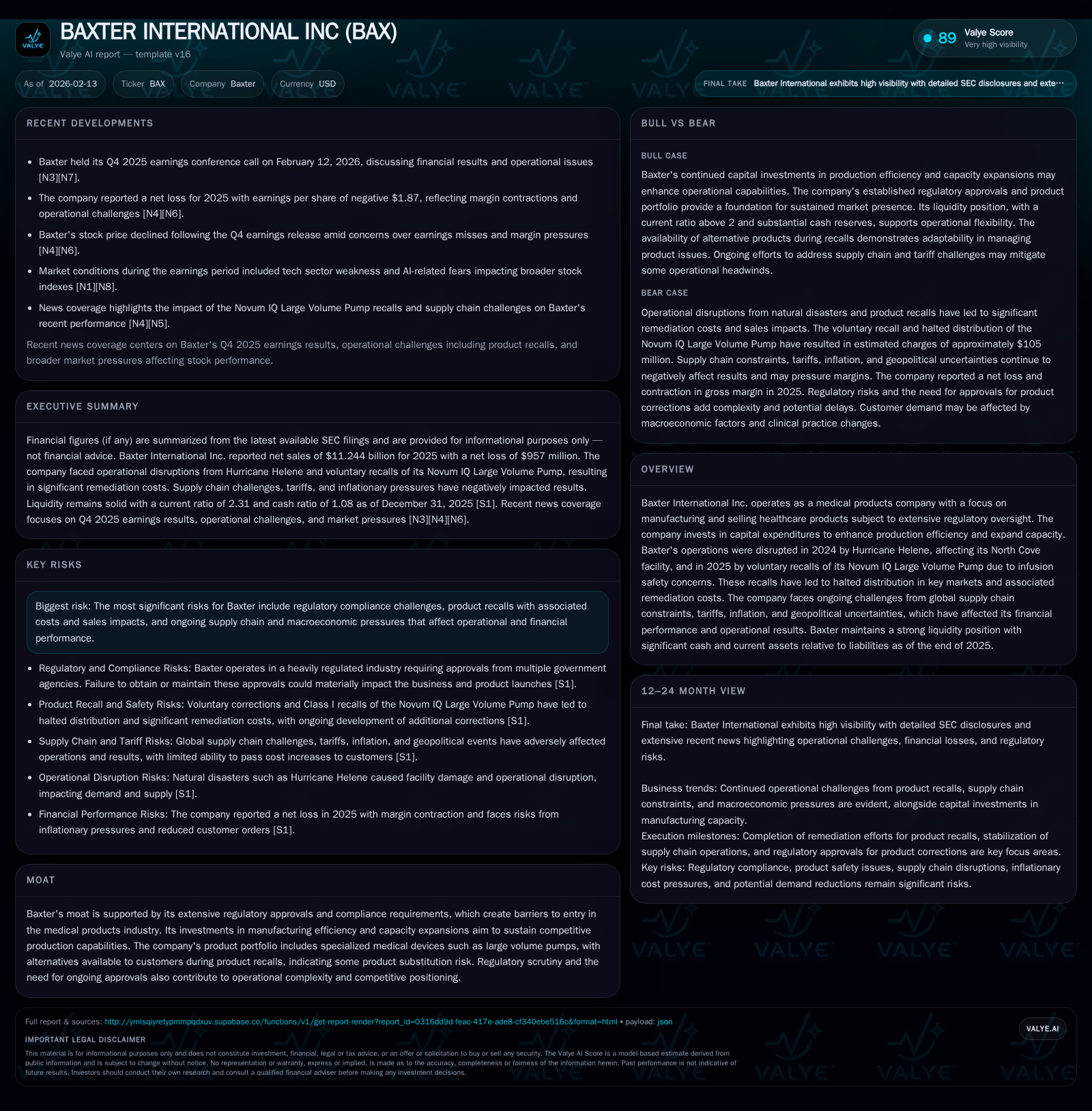

In 2025, Baxter International faced significant operational disruptions from the aftermath of Hurricane Helene and a major voluntary recall of its Novum IQ large volume pump (LVP), leading to halted sales in key markets and remediation costs. These challenges coincided with persistent supply chain constraints and macroeconomic pressures that compressed margins and weighed on earnings. However, robust liquidity, measured capital investments aimed at enhancing manufacturing efficiency, and a regulatory moat continued to provide Baxter with a defensive shield. Market reaction was sharply negative following the Q4 earnings miss, reflecting investor concerns but the company remains focused on navigating uncertainty through disciplined resource allocation and innovation.

Turbulence at Baxter: Floods and Recall Fallout

Baxter International’s operational landscape in 2025 was heavily shaped by external shocks that unfolded over the preceding year. The most notable event was Hurricane Helene which struck Western North Carolina in September 2024 causing substantial flooding at Baxter’s North Cove production facility in Marion, N.C. This facility disruption reverberated into early 2025 — only achieving full operational stability by the end of Q1 — affecting critical intravenous (IV) solutions manufacturing capacity. As Baxter management noted during their Q4 earnings call, certain customers responded with fluid conservation practices embedded within clinical protocols, reducing demand downstream for IV solutions products [N1][S1].

Compounding these production setbacks was the voluntary recall initiated in April 2025 involving Baxter’s proprietary Novum IQ Large Volume Pump (LVP). Initially prompted by reports of under-infusion risks when the device entered standby mode for extended periods, subsequent recalls expanded in July to address additional infusion rate anomalies including risks of over- or under-infusion due to software or set misloading errors. The U.S. FDA classified these recalls as Class I — signaling the highest severity level — compelling Baxter to halt commercial distribution and installations of Novum IQ LVP units across the U.S. and Canada barring medical necessity exceptions [S1]. This stark interruption removed a key revenue driver from Baxter’s portfolio amidst an already strained operating environment.

The sequential timing of the flooding aftermath followed closely by extensive product recalls dismantled Baxter’s sales momentum particularly in its device division linked to infusion therapies. Although Baxter has deployed corrective actions — including ongoing product software updates pending regulatory clearance — the timing for lifting shipment restrictions remains uncertain, exacerbating revenue volatility [S1].

Supply Chain Strains and Macroeconomic Crosscurrents

The fallout from these operational issues was intensified by wider industry-wide pressures impacting cost structures throughout Baxter’s global supply chain network in 2025. Persistent constraints driven by disrupted logistics channels, elevated freight rates, tariff impositions on cross-border components, and inflationary wage pressures collectively inflated manufacturing expenses [S1][N2]. Geopolitical tensions further complicated import dependencies for certain raw materials needed at key facilities.

Baxter’s latest financial disclosures reveal gross margin contraction aligning with these cost headwinds despite revenue growth — net sales increased modestly from $10.6 billion in 2024 to $11.2 billion in 2025 but at the expense of profitability [F1]. Management commentary highlighted margin compression as a material factor contributing to operating losses during a period when supply reliability challenges impeded optimal production scheduling [N1]. This constellation of macroeconomic factors added gravity to Baxter’s recovery efforts, demanding careful balancing between price adjustments, cost containment initiatives, and capital project advancement.

Financial Fortitude: Liquidity Amid Earnings Declines

While earnings performance suffered — posted net loss attributable to common stockholders reached $957 million for full-year 2025 compared with a $649 million loss prior year — underlying financial position demonstrated resilience rooted in ample liquidity reserves [F1][S1]. Cash and cash equivalents rose to nearly $2 billion by year-end while current assets ($6.87 billion) comfortably exceeded current liabilities ($2.97 billion), yielding a healthy current ratio of approximately 2.31 illustrating strong near-term solvency [F1].

Additionally, connector debt reduction efforts were evident: short-term debt shrank dramatically from $2.13 billion at end-2024 to only $1 million at end-2025 alongside maturing portions of long-term debt steadily managed downward from prior years [S1]. This improving leverage profile provided management flexibility amidst ongoing capital needs.

Dividend payments totaling $348 million reflected continued commitment to returning value despite broader profit pressures—a positive signal about confidence in medium-to-long term cash flow recovery prospects [S1]. Overall financial articulation during earnings calls conveyed a tone emphasizing preparedness against uncertainty through conservative balance sheet stewardship while maneuvering through cyclical losses [N13].

Product Portfolio Under Pressure: The Novum IQ LVP Impact

The Novum IQ Large Volume Pump recall stands out as a defining product challenge for Baxter in 2025 given its direct sales interruption coupled with remediation spending requirements. Classified as Class I recalls by FDA— reserved for defects posing serious adverse health consequences or death risk— such regulatory actions underscore both clinical risk sensitivity inherent to Baxter's product line and attendant reputational impact [S1].

During the recall period starting July 2025, Baxter voluntarily ceased shipments and installations within core North American markets significantly shrinking active pump placements contributing to infusion therapy revenues [S1]. This void drove customer migration towards the company’s Spectrum IQ pump offerings as alternative solutions; however, Spectrum IQ commands smaller market penetration resulting in diminished replacement revenue scale.[S1]

Financially, settlement provisions related to estimated lost sales volumes alongside costs for software patches, quality system audits, engineering updates, customer communications, and regulatory submissions have cumulatively pressured margins further in late-2025 results [S1]. Meanwhile, executive statements acknowledged ongoing dialogues with regulators aiming for timely approval cycles but candidly noted continued timeline uncertainties precluding near-term normalization [N1].

This episode crystallizes product substitution risk amid specialized medical device portfolios where technology-specific recalls can quickly divert customer loyalty or contract renewals toward competitors or alternative treatments.

Regulatory Moat vs. Market Realities

Baxter’s entrenched position owes much to its extensive network of regulatory clearances essential for marketing complex medical devices globally—a moat forged through prolonged clinical trials, rigorous compliance systems, ongoing FDA oversight, and post-market surveillance obligations [valye_report_excerpt][S1]. Such barriers represent formidable entry obstacles for new competitors aiming at high-stakes intravenous therapeutic segments.

Yet this regulatory complexity carries a dual-edged sword attribute; it enhances customer switching costs yet simultaneously heightens exposure to compliance-related interruptions when system deficiencies arise—as witnessed following the Novum IQ LVP recall necessitating comprehensive quality upgrades alongside corrective action implementations [valye_report_excerpt][S1].

Management is tasked with balancing proactive innovation investments against responsive risk mitigation measures which invariably impose operating expenses and elongate product development cycles under tightened scrutiny.

Longer term moat durability hinges on maintaining robust quality assurance infrastructure while accelerating agility around product lifecycle risk management—essential under evolving healthcare regulations worldwide.

Capital Investment: Building Efficiency in Disrupted Times

Amid turbulence on multiple fronts—including natural disaster recovery effects and product recall fallout—Baxter invested $513 million in capital expenditures during 2025 focused strategically on enhancing production efficiency, augmenting quality control systems beyond compliance minima, and expanding manufacturing capacity poised for eventual demand rebound [S1][valye_report_excerpt].

Such investments are not merely maintenance related; they represent forward-looking bets on operational scalability designed to reduce unit costs through automation upgrades and process optimization while embedding resilience against future supply interruptions.

Drawing from earnings disclosures, this CapEx spend juxtaposed against profitability declines illustrates deliberate prioritization of longer-term structural gains even if short-term financial metrics remain pressured [S1]. It signals management confidence that industrial modernization will underpin sustainable differentiation once disruptive headwinds subside.

Investor Sentiment and Market Reaction to Q4 2025

The capital markets responded emphatically following Baxter’s announcement of Q4 2025 results marked by an adjusted EPS miss relative to consensus estimates compounded by lowered fiscal year guidance—the company’s stock price plunged roughly 14.6% amid broader tech sector weakness observed concurrently [N2][N12][N13].

Analysts cited margin contraction from inflated cost bases coupled with ongoing Novum IQ LVP shipment suspensions as primary driver concerns whereas bearish revisions reflected caution regarding timing normalization scenarios intrinsic to regulatory-dependent product pipelines.

Investor skepticism also appeared tethered to uncertainties about how swiftly supply chain complexities might ease—a narrative consistent with other medtech peers grappling with analogous macro conditions around inflationary inputs and transportation delays [N9][N10]. Nevertheless, pockets of optimism remained referencing robust cash positions supporting strategic flexibility [N14].

This kneejerk selloff reflects market prioritization of short-term earnings visibility over medium-term strategic execution plans potentially positioning shares well off recent highs but with scope for repricing once recovery milestones surface.

Strategic Outlook: Navigating Through Uncertainty

Looking forward into 2026 and beyond, Baxter faces a multifaceted challenge landscape merging operational execution risks with persistent macroeconomic headwinds balanced against protective moats formed via regulatory licensing and manufacturing investments.

Management acknowledges continued caution citing external demand softness tied partly to changed clinical fluid usage patterns post-Hurricane Helene plus lingering impacts from Novum IQ LVP corrective actions which could extend meaningful revenue headwinds into at least mid-year timeframe [S1][N14]. Yet their message simultaneously highlights leveraging capital projects underway aimed at operational scalability paired with prudent financial stewardship evidenced by manageable leverage ratios.

Industry analysis suggests these dynamics typify medtech sectors where innovation cycles coexist alongside faster-moving policy-driven risk scenarios necessitating agility without sacrificing compliance rigor.[Analysis] Maintaining competitive footholds demands both diligence on product safety imperatives integrated seamlessly with R&D pipelines accelerating next-generation devices addressing emerging patient care needs.

While quantified forecasts carry wide variance amid uncertainties surrounding stimulus triggers or competitive developments overall indication is one of calibrated resilience rather than retreat highlighting potential latent value embedded in strategic positioning amid cyclical adversity.

Disclaimer: This analysis is based on publicly available information including SEC filings and news sources as of February 13, 2026. It does not constitute investment advice or recommendations but serves informational purposes concerning Baxter International Inc.'s business dynamics and industry context.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments