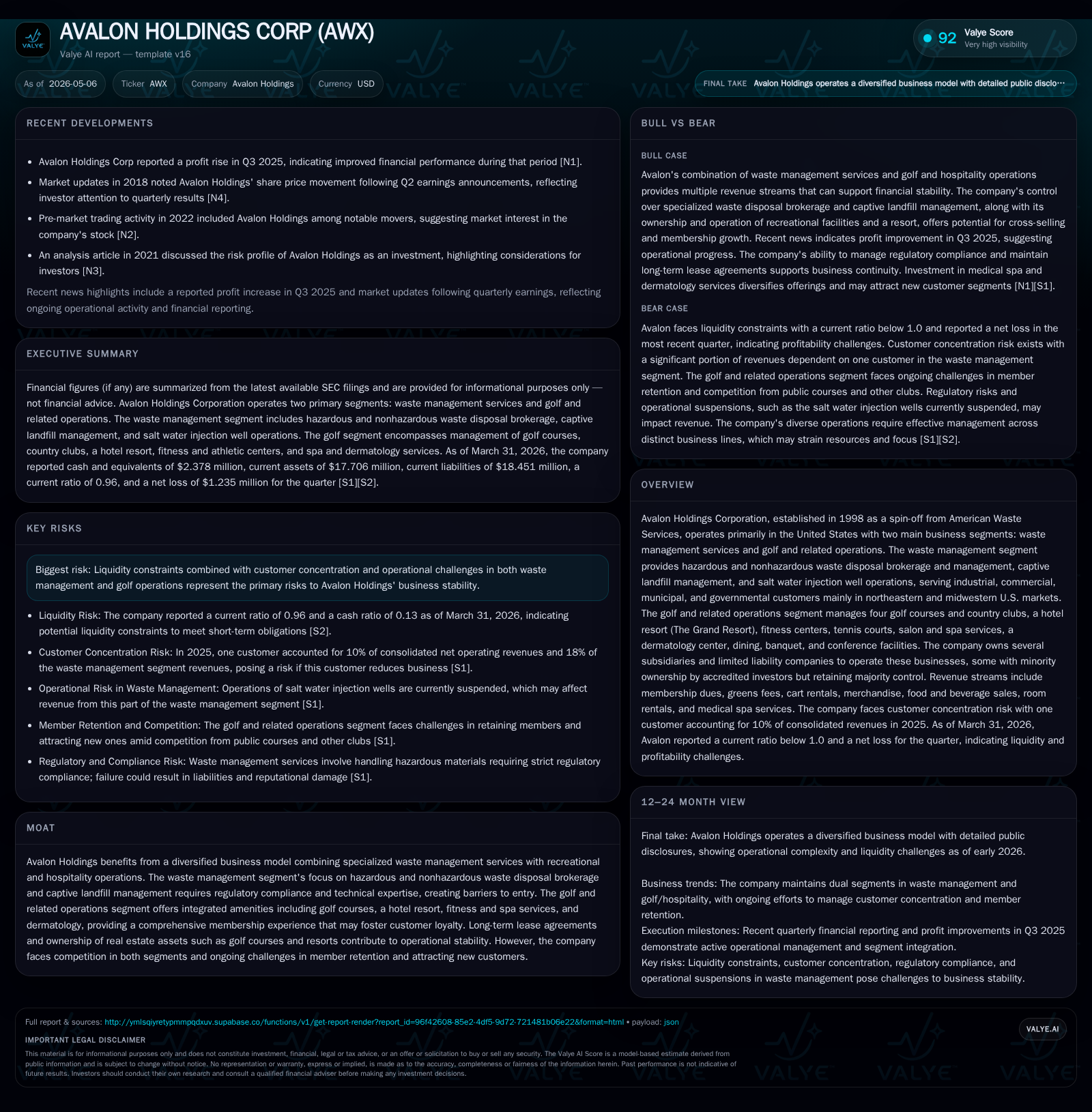

Avalon Holdings Q1 2026: Stable Membership Revenues Offset Competitive Waste Management Pressures

Avalon Holdings reports steady golf membership revenue amid ongoing challenges in waste services, maintaining operational focus and debt compliance.

Avalon Holdings Corp’s Q1 2026 report reveals continued strength in its golf and related operations segment, which benefits from deferred membership dues and a no-initiation-fee structure that supports stable revenue recognition. Meanwhile, the company’s waste management services remain highly competitive and face pressure due to customer concentration and fragmented market dynamics. Avalon maintains compliance with debt covenants under its 2022 Term Loan and holds moderate liquidity as of March 31, 2026. The dual-segment business model provides diversification but also requires balancing operational complexities between recreation/hospitality and specialized environmental services.

Recent Operating Update

Avalon Holdings Corporation's first quarter 2026 filing (10-Q dated May 5, 2026) provides new disclosures emphasizing deferred revenue treatment for its golf membership dues [S2]. Specifically, membership dues are collected annually without upfront initiation fees or mandatory spending commitments. As such, Avalon records deferred revenue when cash is received prior to satisfying its 'stand ready' performance obligation, classifying these as current liabilities based on expected timing of revenue recognition within the annual membership period. This approach anchors near-term operating cash flow stability for the golf segment.

The filing reiterates that ancillary services such as food, beverage, spa treatments, and merchandise do not factor into membership dues pricing; members pay for these separately with no discount obligations. This structure caps membership revenue growth potential but may support retention by lowering barriers to entry for new members who prefer flexible spending on amenities [S2].

Simultaneously, the company confirms that its waste management segment continues competing in a highly fragmented environment dominated by brokerages and facility owners alike. Successful competition depends on price competitiveness augmented by technical knowledge and service quality to tailor disposal solutions unique to industrial or commercial customers' needs. Regulatory compliance remains a significant aspect of operations given hazardous waste handling requirements [S1].

Business Model

Avalon's dual-segment model comprises:

Waste Management Services: Specialized brokerage for hazardous and nonhazardous waste disposal plus captive landfill management. The division sources cost-efficient disposal options tailored per client demand often in northeastern and midwestern U.S. markets. Additionally, Avalon runs salt water injection wells through wholly owned subsidiaries funded partly by accredited investors. This segment relies heavily on regulatory expertise and bespoke service delivery.

Golf and Related Operations: Management of four golf courses via subsidiaries including Avalon Golf and Country Club established in 2003. Facilities encompass a flagship resort (The Grand Resort), fitness centers, tennis courts, salons/spas including a dedicated dermatology center, along with dining and conference venues designed to create an all-encompassing recreational environment.

Revenue is generated primarily through annual golf club memberships (without upfront fees), green fees reduced for members reflecting loyalty incentives, room rentals at the resort, food & beverage sales at affiliated dining venues, plus sales of spa treatments. Waste management revenues derive from brokerage fees charged on contracts secured for third-party waste disposal coupled with income streams from captive landfill operations.

Profit margins are influenced by service mix—golf operations operate with steady but margin-constrained recurring dues plus variable revenues from ancillary sales; waste management margins can be volatile due to price competition but benefit from captive facility ownership reducing disposal costs.

Industry Structure & Competitive Position

Waste Management Segment:

This segment faces intense competition given many regional brokers vying alongside large treatment/disposal operators who sometimes bundle services directly to customers. Avalon's advantage lies in regulatory expertise managing hazardous waste logistics plus ability to identify economically attractive disposal solutions customized per client needs.

However, heavy reliance on major clients creates customer concentration risk evidenced by one prominent customer accounting for a material portion of sales. Market fragmentation complicates scale advantages but allows nimble brokerages like Avalon to carve out niche offerings.

Golf & Related Operations:

Avalon's golf businesses compete regionally with public courses plus more traditional country clubs offering initiation fees and minimum spend requirements absent here. The company's approach favors simplified access via no-initiation fee annual memberships supplemented by extensive amenities integrated around the flagship resort hub.

This ecosystem potentially fosters customer loyalty through bundled lifestyle experiences (golf + fitness + spa + dining). Nevertheless, member renewal rates require careful management given ease of exit without contractual minimums.

Ownership/long-term leases of key real estate assets underpin operational stability providing fixed-location advantages uncommon among smaller operators.

Growth Drivers

Golf Segment Membership Expansion: Growing the base through enhanced amenities integration—leveraging fitness/treatment facilities alongside golf—and targeting broader demographics seeking flexible club access without high upfront costs.

Ancillary Revenue Scaling: Incrementally increasing ancillary spending per member through targeted promotions on spa services, dining experiences, banquet hosting benefitting from resort traffic.

Waste Management Brokerage Optimization: Deepening penetration among industrial clients by expanding technical advisory capabilities to design cost-effective disposal packages amid tightening environmental regulations.

Salt Water Injection Well Operations: Monetization of owned injection sites through offering capacity to third parties driven by energy sector demand for enhanced oil recovery techniques requiring environmental expertise.

Risks & Constraints

Customer Concentration: Heavy dependence on singular or limited customers within waste management exposes Avalon to contract losses materially impacting quarterly results.

Competitive Pricing Pressure: In both brokering waste disposal contracts and attracting golf members sans initiation fees or minimum spend thresholds limits margin expansion levers.

Regulatory Compliance Costs: Ongoing evolving environmental regulations impose operational cost burdens especially in hazardous waste handling exposing breach risks.

Liquidity & Leverage: Net debt stands near $29.7 million against $2.4 million cash equivalents with a current ratio just below parity (0.96), signifying tight working capital conditions requiring prudent cash flow management to meet fixed charges on term loans expiring in 2032 [F1], [S2].

Member Retention Risk: With no contractual lock-ins beyond annual dues payments, member attrition could accelerate if competing local courses offer superior bundled value propositions.

What to Watch Next

Key milestones that will signal shifts include:

- Quarterly updates covering membership retention rates or growth trends reflecting effectiveness of amenity bundling strategies;

- Enhanced disclosure or commentary about customer diversification progress within the waste services segment opening avenues beyond concentrated credit exposures;

- Capital expenditure announcements aimed at golf property enhancements or new capability additions within waste brokerage technology platforms;

- Debt servicing metrics reported in subsequent quarters confirming stable covenant compliance amid macroeconomic interest-rate environments;

- Regulatory developments affecting hazardous waste disposal costs or salt water injection well capacity utilization impacting segment profitability.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $2mm | |

| 2026-03-31 | ||

| Total debt | $32mm | |

| 2026-03-31 | ||

| Net debt | $30mm | |

| 2026-03-31 | ||

| Current assets | $18mm | |

| 2026-03-31 | ||

| Current liabilities | $18mm | |

| 2026-03-31 | ||

| Current ratio | 0.96x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

At quarter-end March 31, 2026, Avalon recorded $2.38 million in cash and equivalents versus total debt near $32.06 million leaving net debt around $29.7 million [F1]. Current assets totaled approximately $17.7 million against current liabilities close to $18.45 million resulting in a current ratio under one (0.96), highlighting tight short-term liquidity [F1].

The 2022 Term Loan Agreement requires monthly principal plus interest payments scheduled over twenty-five years concluding August 2032 bearing a fixed rate of 6% until reset after seven years [S2]. Covenants include a fixed charge coverage ratio minimum tested annually which Avalon was compliant with as of recent fiscal year-end filings.

Operating income most recently reported stood slightly above $2 million annually ending December 2025 while net income registered near $321 thousand; reflecting the modest profitability profile balanced across diverse operations [F1].

Capital expenditure investments continue in supporting both segments' property upkeep and service capacity enhancements consistent with maintaining asset utility for both recreation venues and environmental infrastructure maintenance.

This analysis integrates the latest quarterly disclosures and contextualizes Avalon Holdings’ operating environment across distinct business lines without offering investment guidance or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments