AXOS Financial: Leveraging Regional Focus and Capital Strength to Drive Growth in Q2 2026

AXOS Financial’s strong Q2 2026 earnings underscore its robust regional banking moat, fueled by solid capital and loan momentum despite sector headwinds.

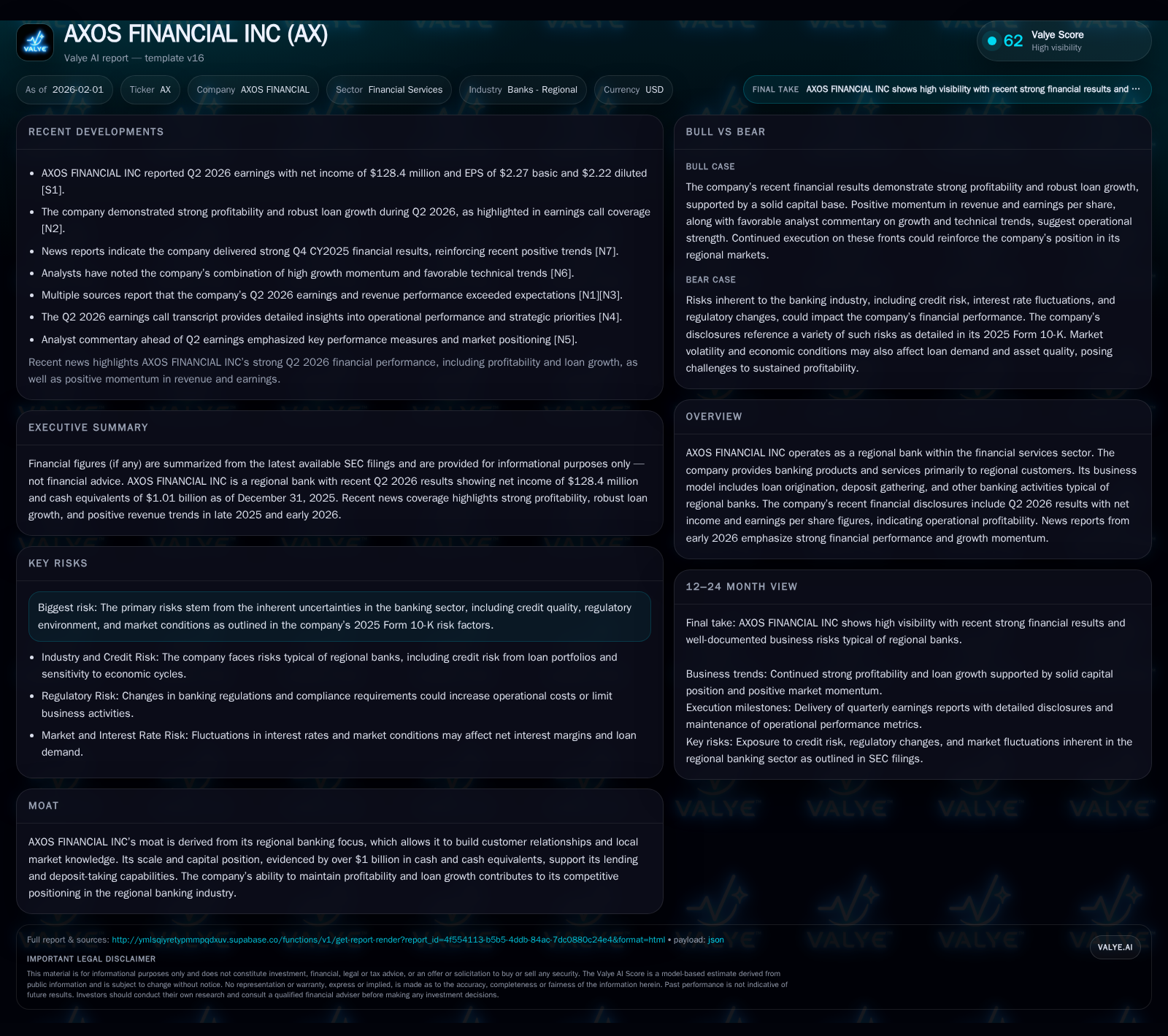

AXOS Financial Inc delivered a significant Q2 2026 earnings beat, driven by strong net income growth and healthy operational momentum. The bank’s niche as a regional player with deep customer relationships and over $1 billion in liquidity bolsters its competitive standing. While regulatory and credit risks remain inherent, AXOS’s capital strength supports ongoing loan origination and deposit growth. Market analysts generally view the bank’s trajectory positively relative to regional peers, with strategic outlook pointing to continued growth amid evolving industry challenges.

Defining a Regional Banking Powerhouse: AXOS’s Niche and Moat

At the core of AXOS Financial Inc’s growth is a focused strategy as a regional bank, which fosters enduring customer relationships deeply rooted in local markets. This niche positioning is more than geographic — it translates into nuanced underwriting capabilities tailored to the unique economic dynamics of their served regions. The company’s latest filings reveal cash and equivalents standing at just over $1.01 billion at the end of 2025 [F1]. This sizable liquidity reserve not only signals operational prudence but also underpins its ability to originate loans aggressively without immediate funding constraints. Such financial flexibility forms a key pillar of AXOS’s competitive moat — a balance between scale sufficient to compete effectively while nimble enough for personalized service.

Complementing this capital strength is AXOS's dedication to building trust through consistent service delivery, often cited by management during the recent Q2 2026 earnings call as a differentiator against larger national players [N1]. This integrated approach of leveraging both quantitative resources and qualitative market knowledge allows AXOS to sustain profitable growth avenues amid an evolving banking landscape.

Q2 2026 Earnings: What Surpassed Expectations?

AXOS's Q2 earnings release delivered an impressive performance that outpaced forecast estimates by roughly 11% on revenue growth [N3]. Net income surged to approximately $128 million for the quarter ending December 31, 2025 [F1], reflecting not only operational efficiency but also effective credit management during periods of interest rate normalization. Earnings per share similarly gained traction beyond consensus views.

Key drivers included accelerated loan originations paired with solid fee income streams from ancillary services like transaction processing — factors highlighted prominently during the earnings call transcripts [N2][N5]. Management emphasized robust underlying demand for lending products across small-to-mid-sized enterprises alongside sustained consumer deposit inflows, creating positive feedback loops for revenue generation [N6]. Additionally, improved cost controls contributed marginally to margin enhancements noted post-results [N7][N13].

This quarterly outcome reinforced market confidence in AXOS's business model execution, positioning them well above several peers who face more acute margin pressures or slower top-line expansions.

Capital Strength and Cash Reserves: The Financial Backbone

AXOS exhibits strong capital adequacy supported by liquidity exceeding $1 billion — a figure referenced repeatedly across recent SEC disclosures [F1][S2]. Such reserves serve dual purposes: providing buffers against unforeseen credit shocks while enabling sustained credit extension into attractive sectors.

By maintaining this financial backbone, AXOS can tactically deploy funds toward higher-yield loans or strategic acquisitions without diluting shareholder value or compromising regulatory thresholds. The presence of substantial cash holdings also imparts operational agility in navigating volatile environments, a frequent challenge within regional banking contexts due to varied economic cycles across local geographies.

Recent filings illuminated confidence from regulators regarding AXOS's capital ratios amid tightened supervisory scrutiny post-pandemic recovery phases [S2]. This further underscores how well-positioned the firm stands to weather cyclical headwinds while continuing disciplined growth trajectories.

Loan Origination and Deposit Growth: Engines of Momentum

The primary impetus behind AXOS’s recent surge links back fundamentally to increased loan origination activity coupled with healthy deposit growth [N2][N5][N11]. Loan velocity accelerated notably during Q2 2026 as borrowers sought financing amid stable interest rate conditions combined with broader economic recovery.

Management commentary stressed continued focus on diversified lending across commercial real estate, small business loans, and consumer credit lines — enabling risk dispersion while capturing multiple market segments [N1]. Furthermore, deposit gathering maintained strong inflows driven by retention strategies emphasizing digital platforms tailored for tech-savvy customers within target demographics.

These dynamics create self-reinforcing financial momentum; rising deposits lower funding costs directly benefitting net interest margins while abundant loan pipelines promise future interest revenue visibility. The synchronized growth in both assets and liabilities signals operational health rare among smaller regional banks currently grappling with uneven credit demand patterns.

Navigating Risks: Regulatory and Credit Challenges in Focus

Amid this growth narrative lies an unvarnished reality underscored by comprehensive risk disclosures within AXOS's SEC filings [S2]. Key vulnerabilities include sensitivity to shifts in credit quality — reflective of possible economic downturn impacts on borrower repayment capacity — as well as evolving regulatory frameworks affecting capital requirements and compliance costs.

The firm openly acknowledges inherent uncertainties categorized under "Risk Factors" which address potential adverse macro-financial developments or policy changes that could curtail earning potential or intensify provisioning needs [S2]. Such transparency is crucial for balanced assessment given banking industry cyclicality.

Regulators have signaled ongoing scrutiny concerning liquidity ratios and stress testing results applicable to mid-sized institutions like AXOS. Navigating this complex regulatory terrain requires continuous monitoring alongside adaptive governance structures implemented recently per management remarks during earnings discussions [N1].

Market Sentiment and Analyst Outlook: What the Latest Calls Reveal

Post-Q2 results witnessed an overwhelmingly positive reception among analysts documented by platforms such as SimplyWall.St and Yahoo Finance reports referencing market calls [N3][N4][N8][N12]. Sentiment coalesced around themes of sustained profitability improvements combined with structural advantages embedded within the regional banking model.

Some analysts highlighted AXOS's superior revenue beat compared to peers as indicative of better-than-expected operational efficiency and resilience [N3]. Chartmill analysis pointed toward high growth momentum coupling technical uptrends with favorable fundamental developments [N12]. However, cautious voices reminded investors that macroeconomic uncertainties—including inflationary pressures or geopolitical events—could temper near-term forecasts [N4].

Overall, the consensus reflects belief in continued execution discipline balanced pragmatically against sector-wide headwinds.

AXOS Financial in Context: Comparing Regional Peers

Placed within the broader universe of regional banks, AXOS distinguishes itself through hybrid advantages combining scale (notably >$1B liquid assets) with localized market expertise—a combination sometimes elusive at this tier industry-wide. Many regional competitors face challenges such as slower digital adoption or constrained capital buffers limiting loan portfolio expansions.

While national banks benefit from sheer size, they often lack the agility or personal client touch that defines successful regional strategies. Conversely, smaller community institutions typically cannot marshal resources comparable to AXOS’s cash reserves or technology investments.

This intermediate positioning provides AXOS with enhanced resilience against volatility experienced by peers balancing tightening regulations alongside fluctuating credit environments — consistent with competitive moats articulated in Valye's sector overview [Valye_report_excerpt].

Future Outlook: Strategizing Growth Amid Industry Trends

Looking ahead, strategic considerations for AXOS pivot on sustaining earnings beats demonstrated most recently [N9][N10] amidst an unpredictable economic backdrop. While growth may moderate relative to prior quarters owing to anticipated tightening or macro uncertainties, management appears committed to leveraging digital transformation initiatives aimed at scaling customer acquisition efficiently.

Continued emphasis on diverse lending sectors coupled with prudent risk management frameworks derived from recent SEC disclosure insights will likely enable measured but persistent loan book enhancements [S2]. Expansion efforts could entail selective geographic extensions or product innovations targeting niches less penetrated by larger incumbents.

Importantly, regulatory vigilance remains paramount given historic banking episodes reminding stakeholders of latent vulnerabilities [S2]. Thus balancing aggressive profit ambitions against sustainable risk appetite will define much of AXOS's near-to-medium term trajectory.

This analysis is based on information publicly available as of early February 2026 including company disclosures, recent earnings call transcripts, market commentary, and industry reports. It aims solely to provide a detailed overview without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments