BioCardia’s Clinical Progress and Financing Challenges Shape Its Future

BioCardia advances innovative cardiovascular therapies while confronting critical capital constraints impacting near-term operations.

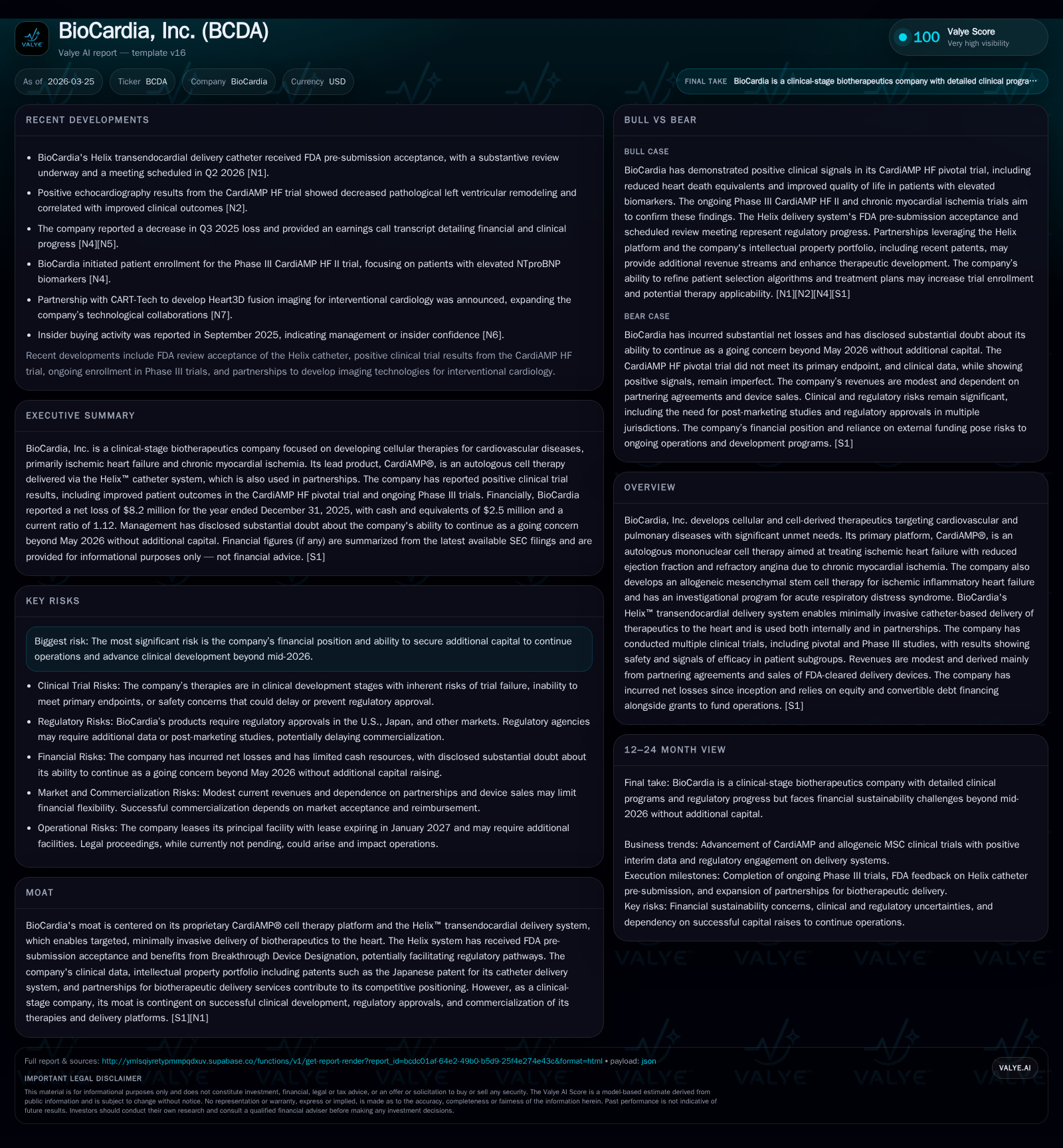

BioCardia, Inc. remains a clinical-stage biotech focused on cellular therapies for cardiovascular diseases, anchored by its CardiAMP® platform and Helix™ delivery system. Historical financials reveal a pattern of consistent net losses and minimal revenues, characteristic of the capital-intensive R&D phase typical in this sector. Recent positive trial data and FDA progress mark important clinical milestones; however, the company faces a liquidity cliff with cash runway only into mid-2026, necessitating urgent capital raises that pose dilution risks. Investors should monitor pivotal CardiAMP trials, regulatory approvals, and partnership developments closely as they will critically influence BioCardia’s execution of its commercialization vision.

From Lab to Clinic: BioCardia’s Growth Drivers and Historical Performance

BioCardia's historical financial footprint underscores the classic trajectory of a clinical-stage biotechnology company, characterized by persistently minimal revenues largely derived from collaboration agreements rather than product sales. The top-line peaked modestly at $576,000 in fiscal year 2016 but declined to $479,000 by the end of 2017 [F1]. Since then, revenue figures have been essentially nominal or non-existent as the focus shifted heavily toward advancing clinical candidates.

Operating income has remained deeply negative attributable to intensive investments in research and development (R&D) required for ongoing cell therapy trials and regulatory submissions. Losses narrowed somewhat from approximately -$11.6 million in 2023 to -$8.3 million in 2025, signaling cost control efforts amid expensive pivotal phase activities [F1]. Net income followed a near parallel trend with a loss of -$8.2 million last fiscal year [F1]. Operating cash flows also improved slightly from a negative $10 million range in prior years to about -$7.4 million most recently [F1], reflecting tight management despite clinical expenditures.

Capital expenditures remain minimal relative to operating expenses, hovering at around $7,000 in 2025 [F1]. The company's balance sheet reveals modest current assets relative to liabilities yielding a current ratio near 1.12 as of year-end 2025 [F1], indicative of strained liquidity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -8 | -7 | -8 | 7000 | -3.5% |

| 2024 | -8 | -8 | -8 | 6000 | +31.3% |

| 2023 | -12 | -10 | -12 | 12000 | +2.8% |

| 2022 | -12 | -11 | -12 | 70000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -919.3 |

| 2024 | -8 | -949.3 |

| 2023 | -10 | 721.8 |

| 2022 | -11 | -243.4 |

Source: SEC companyfacts cache [F1].

This financial summary encapsulates BioCardia's capital-intensive journey focused on pioneering cardiovascular cellular therapies amidst limited commercial revenues.

Pipeline and Platforms: CardiAMP®, Allogeneic Therapies, and Delivery Systems

BioCardia's innovation hinges primarily on its CardiAMP® platform — an autologous mononuclear cell therapy targeting ischemic heart failure with reduced ejection fraction along with refractory angina due to chronic myocardial ischemia [S1][N1]. This personalized cellular approach leverages patients’ own concentrated progenitor cells aimed at stimulating myocardial repair mechanisms.

Complementing this is the Helix™ transendocardial delivery system designed for minimally invasive catheter-based therapeutic administration directly into cardiac muscle tissue [S1][N1]. Recognized by the FDA with Breakthrough Device Designation status, Helix accelerates regulatory interaction timelines while enhancing precision delivery — an essential component given the complexity of cardiac therapeutic applications in interventional cardiology.

Beyond CardiAMP®, BioCardia is developing an allogeneic mesenchymal stem cell candidate targeting ischemic inflammatory heart failure states alongside exploratory programs focused on acute respiratory distress syndrome (ARDS) treatment options [S1]. These pipelines emphasize both autologous and off-the-shelf therapeutic strategies with shared infrastructure leveraging the Helix technology.

The integration of proprietary biologics with advanced catheter platforms creates significant barriers for competitors due to combined intellectual property protections including patents like the Japanese patent on their catheter system [S1][N1]. Additionally, partnering collaborations involve provision of delivery services further embedding BioCardia’s footprint within cardiovascular therapeutic innovation ecosystems.

Interpreting Recent Clinical Trial Data and Regulatory Developments

Key near-term value drivers are rooted in recent favorable clinical signals from the CardiAMP HF trial where echocardiography endpoints indicated safety along with efficacy trends in select patient subgroups [N1]. Such outcomes support the ongoing pivotal Phase III efforts validating performance benchmarks required for marketing authorization.

Regulatory developments extend to the Helix transendocardial delivery system which achieved FDA review acceptance status as of March 2026 [N2]. The Breakthrough Device Designation previously granted facilitates interactive communication pathways with regulators potentially expediting final clearance if endpoint achievements are met.

These milestones collectively form critical inflection points bolstering BioCardia’s transition prospects from clinical evaluation toward commercialization readiness [N1][N2]. Nonetheless, ultimate success depends on conclusive trial readouts confirming statistically robust efficacy alongside acceptable safety profiles.

Capital Structure Realities and the Urgency of Financing Beyond Mid-2026

BioCardia confronts acute financial challenges underscored by an end-of-2025 cash balance near $2.5 million sufficient only until May 2026 absent new capital infusion [S4][S7][S8]. This precarious liquidity position creates substantial doubt concerning the company's ability to continue operations without prompt financing measures.

Management contemplates various funding avenues encompassing equity offerings alongside convertible debt arrangements; however, these typically carry dilutionary effects or onerous covenants impacting shareholder value and operational flexibility [S4][S8]. Moreover, strategic partnerships or licensing deals might be negotiations avenues wherein BioCardia could assign rights relinquishing portions of intellectual property or future revenue streams to secure non-dilutive capital injections.

Given these conditions reflected in 'going concern' disclaimers within official filings, stakeholders must carefully weigh progression risks intertwined with capital access uncertainties typical for clinical-stage biotechs reliant on public markets or institutional investors for survival beyond pivotal development phases [S4][S7][S8].

Forecasting Milestones: What to Watch in Trials, FDA Reviews, and Partnerships

Important upcoming events poised to influence BioCardia’s outlook include:

- Completion status updates from pivotal Phase III CardiAMP HF trials enrolling targeted patient cohorts utilizing refined CPA algorithms for enhanced responder selection [S13][N1].

- Final FDA determinations regarding marketing clearance for Helix catheter systems building upon Breakthrough Device status facilitating commercial adoption [N2].

- Potential expansion or introduction of collaborative partnerships based on delivery system expertise driving recurring revenue streams independent from proprietary therapeutics development [S15][S27].

While no explicit company projections have been disclosed publicly concerning precise timelines or financial impacts associated with these milestones, expert attention should center around trial enrollment accelerations and evidence generation supporting safety/efficacy endpoints constituting regulatory approval requisites .

Assessing Operational Efficiency: R&D Investment, Cash Flows, and Capital Allocation

Operational spending patterns reveal elevated research and development expense trajectories aligned with advancing multiple cell therapy pipelines alongside critical regulatory interactions; R&D outlays escalated to approximately $5 million in fiscal 2025 from $4.4 million prior year reflecting trial closeout activities plus new enrollment initiations and international regulatory submissions [S10][F1].

Selling general & administrative expenses showed moderate reduction mainly attributable to lowered professional service fees together with decreased share-based compensation expense totaling roughly $3.3 million versus $3.7 million last year indicating tightening overhead discipline amidst funding constraints [S10][F1].

Cash flow management reflects predominantly negative operating cash flow trending favorably from previous annual outflows near -$8 million consistent with net loss magnitudes yet constrained by limited capital reserves requiring stringent cost focus without compromising critical clinical milestones execution capability [F1][S23].

The absence of dividend payments or share repurchases aligns logically with a reinvestment strategy necessary during this high-burn stage while share-based compensation programs continue supporting talent retention albeit representing a measured non-cash expense recognized over vesting periods using Black-Scholes valuation methodologies standard within biotechnology sectors [S9][S18].

Return on equity approximates -919%, emphasizing persistent net losses outweighing equity base characteristic of companies still pre-commercial launch where profitability is deferred pending product approvals [F1].

Risk Profile: Navigating Financial Uncertainties and Clinical-stage Industry Norms

BioCardia's primary risk matrix centers around its impending cash depletion timeline juxtaposed against protracted clinical development inherent uncertainties including potential late-stage trial failures or regulatory delays which can materially impair valuation propositions ([S5][S6][S18]). The competitive landscape for cardiovascular cell therapies remains intense involving other emerging biologics entities pursuing similar indications raising the bar for differentiation based on efficacy/safety advancements combined with delivery modalities.

Furthermore, even with Breakthrough Device Designation for Helix catheter advantages industrially recognized barriers such as manufacturing scale-up complexities and reimbursement hurdles persist potentially influencing market penetration speed once eventual approvals arrive (). Legal contingencies appear currently negligible per management disclosures though ordinary course business litigation always represents latent variables within biotech settings ([S3]).

Overall moat sustainability depends heavily on achieving commercial viability through successful late-phase trial conclusions coupled with securing adequate funding enabling timely execution thereby mitigating liquidity risks threatening continuity beyond mid-2026 ([S4]). This intersection delineates BioCardia’s strategic inflection zone where biotech developmental science meets harsh financial realities requiring prudent stakeholder appraisal.

Disclaimer: This analysis is based solely on publicly available information provided through SEC filings and recent news sources as cited. It reflects historical performance indicators and reported facts without offering investment advice or forecasts beyond documented disclosures or grounded analytical perspectives.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments