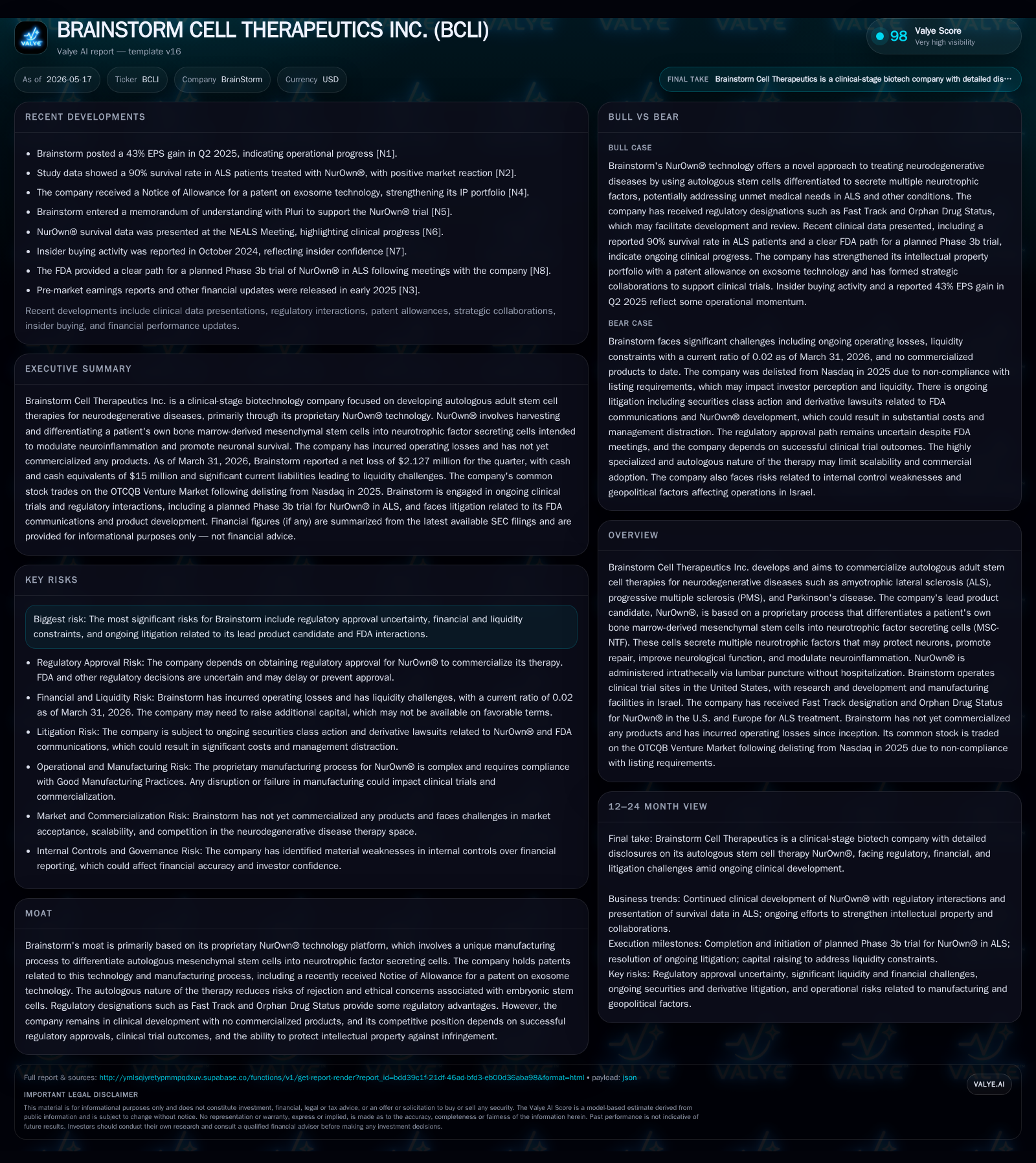

BrainStorm Faces Liquidity Strain While Advancing NurOwn® for Neurodegenerative Diseases

BrainStorm's recent quarter highlights ongoing development challenges amid severe liquidity constraints with potential regulatory catalysts ahead.

BrainStorm Cell Therapeutics remains focused on commercializing its lead autologous stem cell therapy NurOwn® for ALS and progressive multiple sclerosis, leveraging proprietary neurotrophic factor-secreting MSC technology. The latest quarterly filing reveals severe liquidity pressures, with cash of only $15K against current liabilities exceeding $11 million, reinforcing reliance on external financing to continue operations. Regulatory progress such as the FDA Special Protocol Agreement (SPA) for the Phase 3b trial and patent allowances underpin its clinical moat, though risks around approval uncertainty and financial sustainability persist.

Recent Operating Update: Acute Liquidity Stress Amid Clinical Progress

BrainStorm Cell Therapeutics disclosed in its Q1 2026 10-Q filing a critical deterioration in its liquidity position, with cash and equivalents at a mere $15,000 against current liabilities totaling approximately $11.7 million [S2], [F1]. The company remains pre-revenue, continuing to burn cash to fund its research and development efforts on NurOwn®, its leading autologous mesenchymal stem cell therapeutic platform targeting amyotrophic lateral sclerosis (ALS) and progressive multiple sclerosis (PMS). Management has recently raised gross proceeds near $325,000 from private placements and convertible promissory notes carrying high interest rates (12%), indicating tight financing conditions [S11]. Despite these efforts, BrainStorm emphasizes that substantial doubts persist about its ability to sustain operations without new funding [S4].

On the regulatory front, BrainStorm builds upon momentum established by FDA granting a Special Protocol Agreement (SPA) for the Phase 3b ALS trial in April 2024. Its wholly owned Israeli subsidiary holds exclusive commercialization rights licensed from Ramot at Tel Aviv University [S14]. The company’s proprietary NurOwn® stem cell technology retains Fast Track designation and Orphan Drug status from both the FDA and EMA for ALS indications [S14]. These designations facilitate potential expedited review pathways but regulatory approval remains uncertain.

Business Model: Autologous Stem Cell Therapy Licensing with Focused Pipeline Assets

BrainStorm generates value principally through development and future commercialization of NurOwn®, an autologous adult stem cell therapy designed for debilitating neurodegenerative diseases including ALS, PMS, Parkinson's disease, and potentially Alzheimer’s disease [S1], [S14]. The core innovation stems from harvesting a patient’s own bone marrow-derived mesenchymal stem cells (MSC), expanding them ex vivo under a proprietary protocol inducing differentiation into neurotrophic factor secreting cells (MSC-NTF) [S20]. These differentiated cells produce several neuroprotective cytokines — including VEGF, GDNF, BDNF — which are hypothesized to modulate neuroinflammation and support neuronal survival [N2] (analysis: these factors have been widely explored in CNS disorders for trophic support).

NurOwn® is administered intrathecally via lumbar puncture without hospitalization requirements—a key procedural advantage intended to improve patient convenience and enable repeated treatments from a single bone marrow harvest due to cryopreservation capabilities [S20].

The commercial rights belong primarily to Brainstorm Cell Therapeutics Ltd., headquartered in Israel where the R&D facilities and contract manufacturing under Good Manufacturing Practices (GMP) operate [S24]. This subsidiary also oversees late-stage clinical execution primarily at U.S.-based trial sites [S14]. Manufacturing occurs at an Israeli GMP center within Sourasky Medical Center in Tel Aviv allowing niche control but capacity constraints may limit near-term scale-up potential [S15], (analysis: biotech manufacturing scale often bottlenecks cell therapies ahead of commercialization).

Revenue mechanics remain undeveloped until product approvals are secured; sales would likely derive from direct marketing or partnerships licensing NurOwn® post-approval. Pricing dynamics will pivot largely on competitive positioning against other emerging ALS therapies (e.g., small molecules like AMX0035 or antisense oligonucleotides), reimbursement frameworks for orphan indications, and demonstrated efficacy/safety profiles backed by pivotal trials. Margins could be influenced significantly by high manufacturing costs for individualized autologous therapies versus biological potency.

Industry Structure and Competitive Position

BrainStorm operates within a highly specialized biotechnology niche focused on advanced cellular therapeutics for neurodegenerative diseases—a segment characterized by high scientific complexity, stringent regulatory demands, long clinical cycle times, and significant capital intensity. The market opportunity for ALS remains unmet by durable disease-modifying treatments; existing approved drugs provide modest symptomatic relief rather than transformative benefit.

Competitors range from other autologous/allogeneic cell therapy developers to gene therapy companies targeting CNS diseases. However, BrainStorm’s NurOwn® platform distinguishes itself via the proprietary MSC differentiation methodology that releases multiple neurotrophic factors simultaneously—a potential multi-modal mechanism not offered by conventional single-target agents [S20]. The exclusivity provided by intellectual property protections—including recently allowed patents related to exosome technologies derived therefrom—fortifies competitive barriers.

Nonetheless, as BrainStorm remains uncommercialized with clinical-stage status only through completed Phase 3 ALS and Phase 2 PMS trials showing nuanced results thus far, its competitive strength ultimately depends on achieving regulatory approvals bolstered by confirmatory efficacy outcomes. Delisting from Nasdaq in mid-2025 after non-compliance with minimum equity rules may also impair investor confidence and reduce share liquidity relative to peers still listed on major exchanges [S8], [S14].

Growth Drivers

- Regulatory Approvals: Receipt of U.S.

These drivers are realized through measurable KPIs such as clinical trial enrollment rates, completion of enrollment targets for Phase 3b trials under the SPA agreement [N2], regulatory submission timelines monitored by FDA correspondence updates [S2], patent grant announcements, capex deployment at manufacturing sites reflected in R&D spend thresholds ([F1]), and fundraising transaction closings disclosed in filings.

Risks / Watchpoints / Growth Constraints

- Financial Viability: The most immediate risk emerges from severely constrained liquidity—operating deficits necessitate prompt access to substantial capital for continuation beyond a limited runway window. Failure to raise additional funds may force operational curtailment or restructuring [S2], [F1].

- Regulatory Approval Uncertainty: Despite Fast Track designation and SPA arrangements facilitating review pathways, FDA rejection or request for extensive additional trials remains a tangible risk given novel therapy modality.

- Litigation Exposure: Ongoing legal disputes involving shareholder derivative suits tied to data review processes impose potential financial drains and management distraction [S1].

- Market Competition: Emergence of alternative therapeutics with stronger clinical profiles or more scalable commercial models could erode market potential.

- Manufacturing Scale-Up Challenges: Capacity limitations at key Israeli facilities coupled with technical complexity may hamper timely supply chain readiness post-approval.

- Stock Liquidity & Market Perception: OTCQB listing decreases visibility among institutional investors compared to Nasdaq presence; stock volatility adds speculative uncertainty.

- Clinical Trial Risks: Delays or failures in ongoing studies could negatively impact valuation and financing capabilities.

- Geopolitical Factors: Adverse regional events affecting Israeli R&D/manufacturing centers may disrupt operations unexpectedly.

What To Watch Next

- Release of top-line results from ongoing NurOwn® Phase 3b ALS study under FDA SPA guidance.

- Updates on FDA evaluation regarding the Citizen Petition requesting re-review of supporting data for NurOwn®.

- Additional financing events such as private placements or debt issuances providing fresh capital runway extensions.

- Announcements of patent grants especially relating to platform adjuncts like exosome tech enhancing IP moat.

- Progression on PMS indication trials potentially expanding therapeutic reach beyond ALS.

- Regulatory submissions filed in U.S., Europe or other markets indicating commercialization acceleration.

- Manufacturing capacity expansion initiatives essential for commercial supply readiness.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $15000 | |

| 2026-03-31 | ||

| Total debt | $1329000 | |

| 2026-03-31 | ||

| Net debt | $1314000 | |

| 2026-03-31 | ||

| Current assets | $184000 | |

| 2026-03-31 | ||

| Current liabilities | $11764000 | |

| 2026-03-31 | ||

| Current ratio | 0.02x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, BrainStorm reported total assets amounting to approximately $755K dominated by minimal cash ($15K) alongside current liabilities standing at $11.7 million resulting in a precarious current ratio near 0.02 denoting short-term solvency concerns [F1], [S2]. Total debt stood around $1.33 million primarily comprising short-term loans including convertible promissory notes bearing high interest rates issued recently [S2], [S11].

Operating expenses remain predominantly associated with research & development alongside general administrative outlays sustaining clinical efforts without revenue generation yet evident [S2]. Net losses continue deeply negative reflecting early-stage biotech attributes heavily skewed towards product development expenditures rather than monetization.

Capital raising activities during early 2026 via private placements garnered gross proceeds near $200K plus issuance of secured convertible debt infusing incremental liquidity but dependent on further infusions going forward to maintain continuity given exhausted working capital reserve balances underlined by accounts payable exceeding $7 million reflecting deferred supplier payments obligating attention promptly [F1], [S2].

Overall financial dynamics highlight acute operating risk balanced cautiously against nascent clinical validation advances making financing access pivotal in bridging developmental gaps toward approval-driven value realization.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments