Biodesix Inc Advances Cancer Diagnostics with Nodify CDT Integration Amid Profitability Challenges

Biodesix’s latest quarterly results highlight revenue growth driven by proprietary diagnostics alongside persistent net losses and regulatory uncertainties.

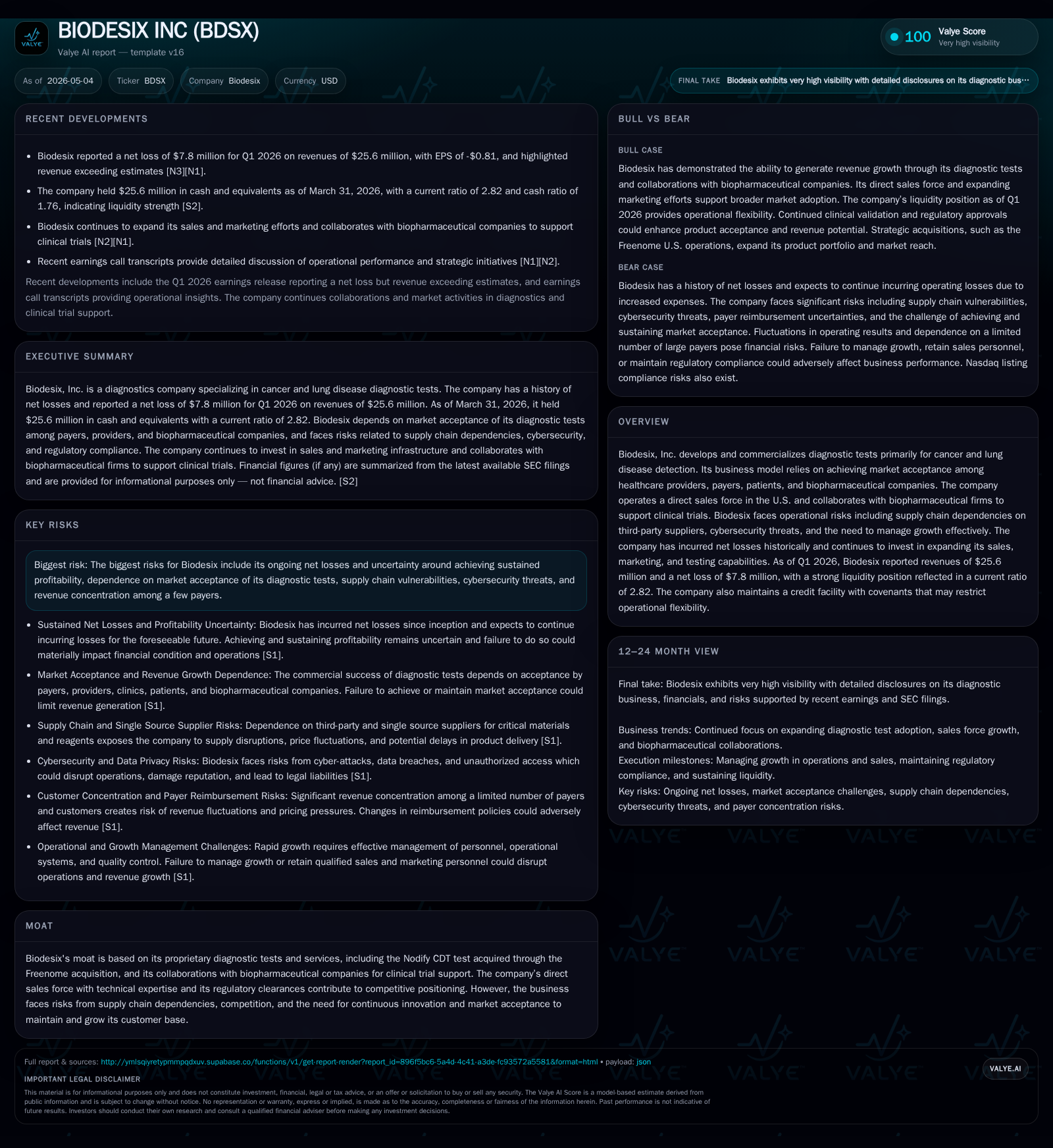

Biodesix, a diagnostic company specializing in cancer and lung disease tests, reported first-quarter 2026 revenues of $25.6 million with ongoing net losses reflecting investments in sales and R&D. Its business model revolves around proprietary diagnostic tests including the Nodify CDT platform acquired from Freenome, combined with a U.S.-based direct sales force and biopharma collaborations. While the company benefits from regulatory clearances and payer coverage, it faces risks from reimbursement shifts, supply chain dependencies, and competition. Growth hinges on expanding market acceptance among providers and payers, scaling sales capabilities, and advancing clinical trial support services.

Recent Operating Update

Biodesix’s first quarter 2026 results filed on May 4 signal incremental progress but also reinforce its current growth challenges [S2]. Reported revenue for Q1 stood at $25.6 million, narrowly surpassing analyst estimates per earnings transcripts [N3], yet the company posted a net loss of $7.8 million reflecting ongoing investments in commercial scaling and R&D. This reflects a continuation of the company’s trend of incurring losses while building out core capabilities established over prior years.

Liquidity remains sound with $25.6 million in cash and equivalents against total debt of approximately $50 million as of March 31, resulting in a current ratio of 2.82—a comfortable buffer that supports operations as Biodesix pursues longer-term commercialization objectives [F1]. No recent amendments to debt covenants or credit facility terms were noted that materially constrain near-term flexibility [S2][S3].

From an operational perspective, Biodesix continues to prioritize expansion of its sales force focused on driving adoption of its differentiated lung cancer diagnostics through provider engagements across the U.S., while maintaining partnerships with biopharmaceutical companies to support clinical trials that incorporate its biomarker testing services [S1]. The acquisitions completed previously have been integrated into the product portfolio to enhance service offerings including notably the Nodify CDT test platform originally from Freenome.

Business Model

Biodesix generates revenue primarily through the sale of proprietary diagnostic tests designed for cancer and lung disease detection offered to healthcare providers who order these tests based on clinical judgment. Their key differentiators lie in delivering molecular diagnostic assays that provide risk stratification beyond standard imaging or biopsy methods.

The company’s revenue mechanics involve monetizing per-test fees paid either directly by providers or indirectly via reimbursements from public (Medicare/Medicaid) and private payers. Contractual relationships with payers dictate coverage levels and price points which combined with test volume determine top-line performance. Adoption depends heavily on clinician education, perceived clinical utility, reimbursement reliability, and patient access.

An important element is Biodesix’s dual approach leveraging both direct sales efforts—engaging pulmonologists, oncologists, and other physicians—and collaboration agreements with biopharma firms who utilize Biodesix's tests for biomarker-driven clinical trial enrollment criteria or monitoring therapeutic responses. This dual channel provides somewhat diversified demand streams but also complexity in managing growth across different customer segments.

Margins are influenced by test complexity (lab reagents and processing), scale efficiencies within their centralized CLIA-certified laboratory operations, third-party reagent costs, and reimbursement rates negotiated with payers. Investments in R&D to innovate next-generation assays coupled with sales expansion pressures have resulted in operating losses historically [S1].

Industry Structure and Competitive Position

The precision oncology diagnostics space is rapidly evolving with players ranging from early-stage startups to large established diagnostics firms expanding into liquid biopsy and genomic profiling technologies. Biodesix occupies a niche focused initially on lung cancer risk assessment via proprietary protein biomarker panels like Nodify CDT combined with sequencing-based solutions.

Key competitive advantages include regulatory clearances that enable clinical adoption without requiring full FDA premarket approval due to current Laboratory Developed Test (LDT) categorization under CLIA regulations [S24]. Ownership of patented biomarker signatures supports intellectual property moat though patent disputes remain an industry-wide threat looming over smaller innovators as detailed in risk disclosures [S19].

Furthermore, Biodesix’s investment in technical sales personnel familiar with oncology workflows enhances customer retention potential—these are high-touch relationships critical where switching costs can be moderate.

Nevertheless, competition is intensifying not only from competitor diagnostics developers but also evolving regulatory policy that threatens to subject LDTs to greater FDA scrutiny which would raise compliance burdens significantly if enacted going forward [S24]. Additionally, larger players including those focusing on multi-cancer early detection tests pose risks of displacing legacy assays.

Growth Drivers

Biodesix’s growth hinges on multiple measurable factors:

- Market Adoption: Increasing awareness among pulmonologists and oncologists drives test volume growth; penetration into integrated health systems or Accountable Care Organizations (ACOs) could accelerate uptake.

- Payer Coverage Expansion: Securing broader insurance coverage especially from large private payers improves revenue predictability; recent CMS initiatives focusing on program integrity introduce uncertainty but broad acceptance remains critical.

- New Product Launches: Developing enhanced versions or complementary diagnostic products addressing additional indications such as other cancers or disease states expands addressable market.

- Clinical Trial Services: Growing contract research collaborations with biopharmaceutical firms creates recurring revenues tied to drug development pipelines.

- Sales Force Scalability: Effectiveness and scale of direct sales team correlate closely to commercial success given physician education requirements.

KPI metrics relevant here include test volumes ordered/processed quarterly, payer reimbursement rates achieved versus list price, frequency of clinical trial partnership wins/bookings, sales headcount growth rates alongside geographic penetration progress.

Risks / Watchpoints / Growth Constraints

Despite promising technological positioning, significant risks temper Biodesix’s outlook:

- Sustained Profitability Uncertainty: History of continued net losses underscores ongoing challenges balancing growth investments against cost control; sustained profitability remains elusive per disclosures [S1].

- Reimbursement Volatility: Changes in payer policies including aggressive audits or “CRUSH” initiatives may lead to delayed payments or claim denials adversely impacting cash flow timing [S2].

- Regulatory Shifts: Potential FDA rule changes could revoke enforcement discretion over LDTs introducing costly premarket submission requirements inhibiting test launches or increasing expenses substantially [S24].

- Supply Chain Dependencies: Reliance on specialized third-party reagents exposes operation to risks around availability disruptions or price inflation affecting margins.

- Competitive Pressure: Accelerating innovation by competitors coupled with expanding use of multi-cancer screening platforms may reduce demand for legacy tests like Nodify CDT.

- Customer Concentration: Revenue dependence on limited number of payers increases vulnerability if contracts are lost or pricing diminished [S16].

- Cybersecurity Threats: Sensitive patient data handled exposes company to regulatory penalties or reputational harm if breaches occur.

Constrained financial resources place premium on efficient capital deployment without compromising go-to-market strategy execution amid these headwinds.

What To Watch Next

Investors and analysts should monitor:

- Quarterly test volume trends particularly for Nodify CDT along with horizon pipeline test launches announced providing clarity on commercialization traction.

- Updates regarding reimbursement landscape changes including CMS policy announcements impacting molecular diagnostics payments.

- Regulatory developments concerning future FDA oversight framework for LDTs; any signals toward increased regulation warrant close attention as potentially material cost driver.

- Sales force expansion plans disclosed during earnings calls indicating ability to continue scaling provider engagement effectively.

- New partnerships or clinical trial collaborations signaling diversification of revenue streams beyond direct consumer diagnostic testing.

- Financial guidance revisions reflecting operating leverage improvements or shortfall risks tied to payer delays or competitive pressures.

Financial Profile Snapshot (As of Q1 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $26mm | |

| 2026-03-31 | ||

| Total debt | $50mm | |

| 2026-03-31 | ||

| Net debt | $24mm | |

| 2026-03-31 | ||

| Current assets | $41mm | |

| 2026-03-31 | ||

| Current liabilities | $14mm | |

| 2026-03-31 | ||

| Current ratio | 2.82x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Revenue | $25.6 million | |

| 2026-03-31 | ||

| Net Loss | $(7.8) million | |

| 2026-03-31 | ||

| Cash & Equivalents | $25.6 million | |

| 2026-03-31 | ||

| Total Debt | $50.0 million | |

| 2026-03-31 | ||

| Current Assets | $40.9 million | |

| 2026-03-31 | ||

| Current Liabilities | $14.5 million | |

| 2026-03-31 | ||

| Current Ratio | 2.82 | |

| 2026-03-31 |

This snapshot confirms robust liquidity enabling short-term operational funding despite negative earnings reflecting continuing scale-up investments supported by manageable leverage levels consistent with sector norms for emerging diagnostics firms [F1].

This analysis synthesizes Biodesix Inc’s latest quarter filing alongside annual contextual disclosures highlighting its evolving business model centered on proprietary cancer diagnostics amid sector-specific regulatory dynamics and market acceptance challenges. The path forward demands balancing innovation-driven growth against financial discipline within an increasingly complex reimbursement landscape. No investment recommendation is implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments