BEL Fuse's Growth Rebound and Tariff Challenges in Connectivity Solutions

A surge in BEL Fuse’s 2025 earnings contrasts with ongoing tariff-related supply chain risks amid global operational shifts.

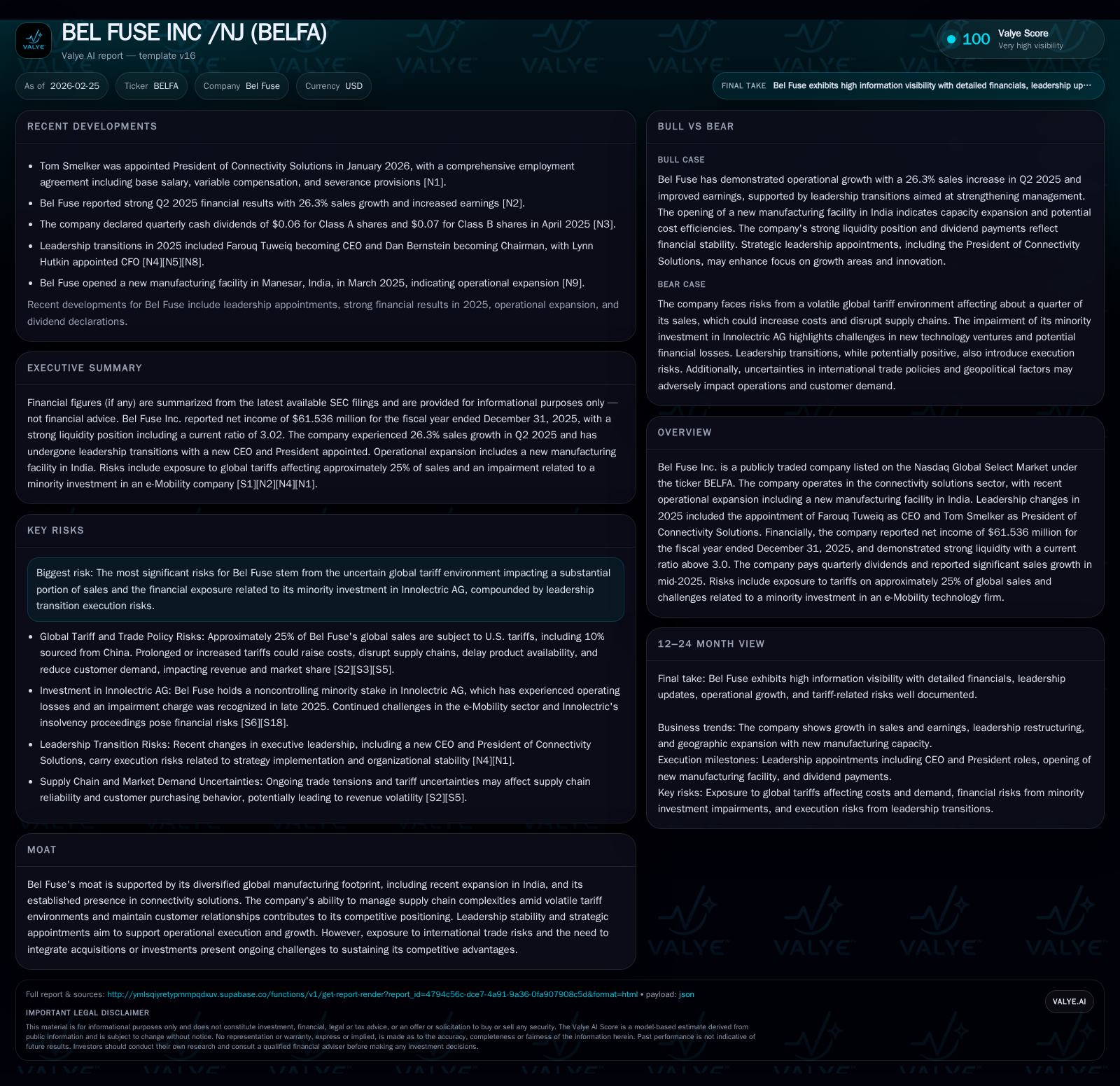

BEL Fuse Inc. demonstrated a notable profitability rebound in 2025 driven by steady revenue growth and significant operating leverage, supported by strategic leadership changes and expansion of its manufacturing footprint, including a new facility in India. However, about a quarter of its global sales remain exposed to volatile U.S. tariffs, particularly on imports from the PRC and Israel, complicating supply chain management and customer demand patterns. The company’s capital allocation prioritized dividends over buybacks in 2025 while maintaining strong liquidity. Going forward, key focus areas include tariff policy developments, integration of recent minority investments, and navigating demand cyclicality within connectivity markets.

2025 Financial Performance: Return to Strong Profitability

BEL Fuse’s fiscal year 2025 results marked a substantial rebound in profitability after several years of more modest earnings performance. Revenue edged up modestly by approximately 1.2% year-over-year to around $121 million [F1], indicating stable top-line conditions despite external uncertainties. The standout metric was operating income which climbed sharply by nearly 73% year-over-year to $110.996 million [F1], signaling significant margin improvement likely driven by operational efficiencies and favorable product mix shifts in the connectivity solutions segment.

This operating leverage translated into net income growth of about 50%, rising from $40.96 million in the prior year to $61.536 million for FY 2025 [F1], delivering an estimated return on equity near 14.5%. Operating cash flow also increased moderately by nearly 9%, totaling $80.6 million, supporting strong free cash generation after subtracting capex spending of $12 million—a slight decrease from prior years [F1]. This improvement showcases BEL Fuse's effective cost control alongside revenue stability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 62 | 81 | 111 | 12 | +50.2% |

| 2024 | 41 | 74 | 64 | 14 | -44.5% |

| 2023 | 74 | 108 | 88 | 12 | +40.1% |

| 2022 | 53 | 40 | 65 | 9 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 3 | 0 | 69 |

| 2024 | 3 | 16 | 60 |

| 2023 | 3 | 0 | 96 |

| 2022 | 3 | 0 | 31 |

Source: SEC companyfacts cache [F1].

Note: Specific data for certain years omitted due to lack of complete metrics.

Leadership Renewal Driving Operational Focus

Key leadership changes occurred during the year with Farouq Tuweiq appointed CEO and Tom Smelker installed as President of Connectivity Solutions early in January 2026 [N1][S1]. These appointments reflect a deliberate intent to accelerate operational execution and realign management focus amid ongoing external headwinds such as tariffs and supply chain disruptions.

Under this refreshed leadership team, BEL Fuse prioritized expanding its global manufacturing footprint while enhancing supply chain agility, reflecting tactical responses designed to offset tariff impacts and customer procurement shifts due to increased trade uncertainties.

Expanding Global Manufacturing: The India Facility and Beyond

The strategic addition of a manufacturing plant in India formed part of the company’s efforts to diversify production capacity geographically [N1][S8]. This new facility strengthens the company’s offshoring footprint which is crucial given about a quarter of its global sales are subject to U.S.-imposed tariffs ranging from moderate to very high rates on imports originating mainly from China (10%), Israel (8%), Slovakia (3%), Dominican Republic (1.5%), among others [S2][S7][S15].

Expanding local content through such investments not only helps reduce unit costs but facilitates mitigation against tariff passthrough challenges by enabling supply closer to end markets or circumventing specific tariff triggers through alternate regional sourcing—practices increasingly critical given volatile international trade policies impacting connectivity product components.

Tariff Exposure and Trade Risks Impacting the Supply Chain

Approximately one-quarter of BEL Fuse’s consolidated global sales currently incur tariffs when imported into the U.S., notably including products sourced from China where tariffs can reach up to 55% [S2][S4][S7]. Additional exposure arises from Israel (8%) and Slovakia (3%) origin products which face tariffs typically between 10%–20% [S2][S15].

Tariffs increase cost-of-goods-sold pressures directly while also inducing indirect effects such as downstream customer procurement adjustments—customers may delay shipments or reduce orders due to price elasticity sensitivities when costs escalate abruptly under tariff regimes.

BEL Fuse has attempted mitigation through negotiations with suppliers to share cost burdens, adjusting pricing strategies where allowable without significantly hurting demand elasticity, and seeking alternative sourcing markets whenever feasible [S14][S15]. However, these efforts require time and entail execution risk amid supply chain constraints worsened globally by geopolitical tensions.

Moreover, continued uncertainty around trade policies presents ongoing challenges since any escalation or prolongation could materially affect revenue visibility and market share retention in impacted segments.

Assessment of Future Growth Prospects Amid Uncertain Demand

Growth prospects appear mixed with structural opportunities centered around geographic expansion initiatives like India plus ongoing penetration into fast-growing connectivity solution sectors managed under new leadership mandates [N1][S1]. Yet growth remains capped by external demand cyclicality especially tied to non-core ventures such as e-Mobility technologies where BEL Fuse holds a minority stake that is currently impaired due to market softness in EV sectors [S22][S23].

A notable event was the anticipated impairment charge up to approximately $14 million recorded late in Q4-2025 related to Bel's minority investment in Innolectric AG, a Germany-based e-Mobility technology company now undergoing insolvency proceedings due to delayed high-volume sales and softening government incentives [S22][S23].

Additionally, broader economic conditions including inflationary input cost pressures combined with unpredictable tariff environments temper upside potential while layering execution complexity into realizing synergy benefits from recent acquisitions like Enercon where remaining ownership consolidation is pending completion per shareholder agreements [S16][S18].

Hence future topline expansion depends heavily on navigated industry cycles alongside operational discipline under revised governance.

Capital Allocation Strategy: Dividends, Buybacks, and Investment

BEL Fuse maintained quarterly dividend payments amounting cumulatively to approximately $3.46 million for FY2025 consistent with prior years despite challenging macro contexts demonstrating capital return discipline focused on shareholder yield stability rather than aggressive stock repurchases which paused completely after $16 million buybacks occurred in FY2024 [F1][S9].

Capital expenditures fell slightly by about 15% year-over-year illustrating a measured investment approach oriented towards sustaining core manufacturing capabilities including funding expansions such as the Indian plant rather than excessive capacity build-outs that could strain free cash flow amid uncertain demand.

Free cash flow generated stood near $68.6 million (operating cash flow less capex), underpinning financial flexibility for allocations between debt reduction, strategic M&A or other growth-oriented initiatives balanced cautiously with payout commitments.

Liquidity Position and Balance Sheet Strength

Year-end metrics highlight robust liquidity reflected by a current ratio exceeding three times (3.02), driven by current assets approximating $385 million against current liabilities near $127 million [F1], confirming ample working capital adequacy essential for managing supply cycle fluctuations common in connectivity industries.

Equity grew markedly compared to prior years reaching over $425 million bolstered by retained earnings from profitability turnaround while no significant new debt was reported suggesting conservative leverage usage supportive of creditworthiness even amid external risks related to tariff volatility or restructuring costs associated with acquisitions integration processes like Enercon stakes completion [F1][S10][S16].

What Investors Should Watch Next: Integration, Tariffs, and Market Trends

Ongoing monitoring should focus on three main vectors:

- The successful integration progress regarding the Enercon acquisition—particularly timing and realization of expected synergies—as well as execution effectiveness under renewed leadership ambitions which will shape medium-term operational momentum [S16].

- Developments concerning U.S tariff policies relevant to countries constituting roughly one quarter of BEL Fuse’s sales; any easing could favorably lower COGS risk while escalation pressures may trigger further procurement adjustments or margin squeezes impacting profitability continuity [N1][S2].

- Market signals within connectivity solutions end-markets including defense-related segments served via subsidiaries plus cyclical trends affecting e-Mobility technologies entangled with the minority Innolectric investment whose insolvency restructuring underscores inherent technological sector risks beyond core manufacturing operations [N1][S23].

These factors collectively represent pivotal catalysts or headwinds that will dictate risk-reward calibration for stakeholders over coming reporting cycles.

Disclaimer: This analysis is based solely on publicly available information up through February 2026 filings and disclosures relating to BEL Fuse Inc., including SEC filings and corporate communications provided herein. It does not constitute investment advice or recommendations but intends informational insight reflecting historical data interpretation and contextual understanding within the connectivity solutions sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments