Beneficient Faces Financial Strains and Strategic Reset Amid Leadership and Litigation Developments

Beneficient's latest quarterly filings reveal operational challenges, leadership shifts, and strategic moves aimed at stabilizing its collateral management business.

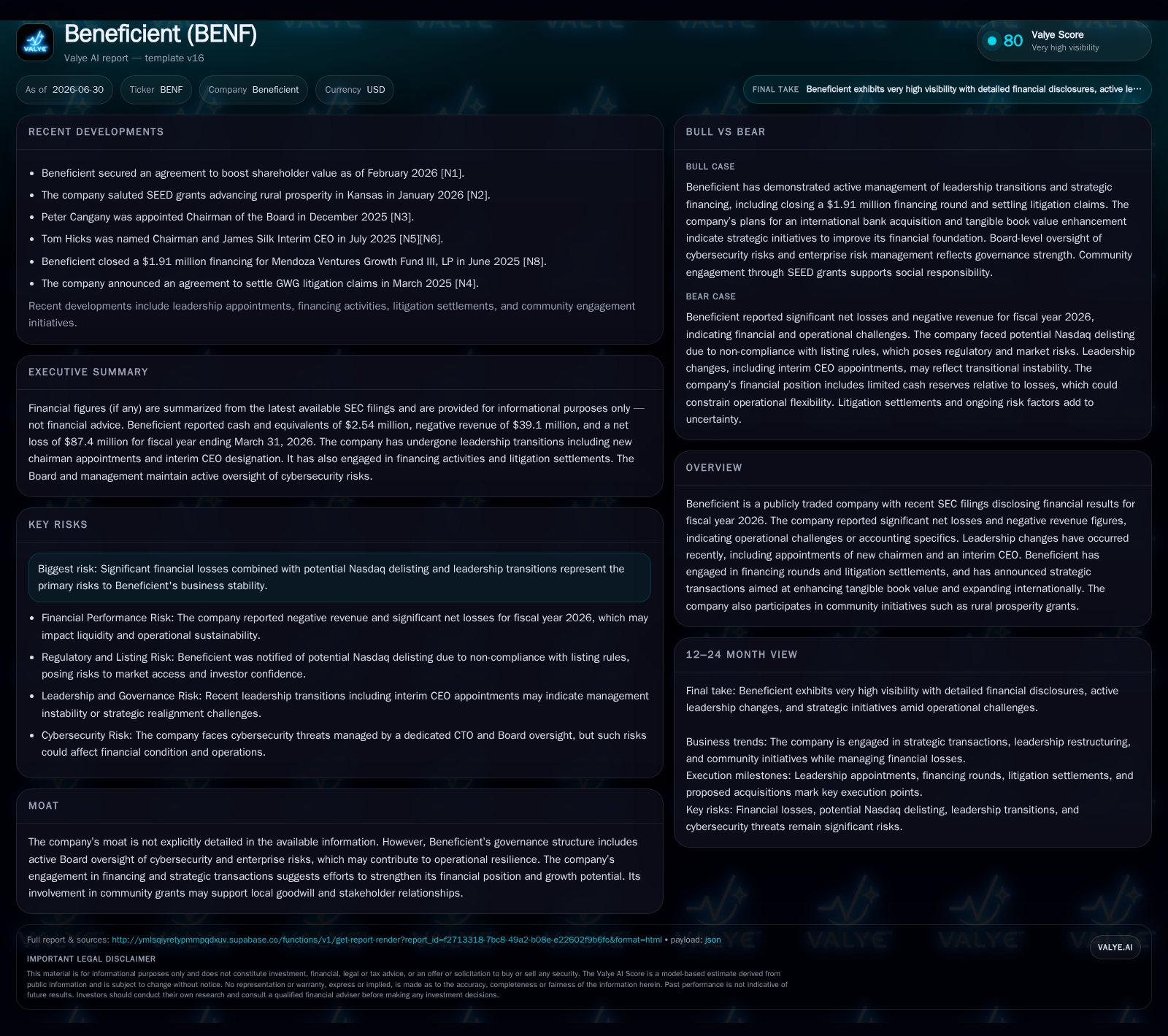

Beneficient reported substantial net losses and negative revenues in its latest quarterly results, reflecting ongoing operational difficulties within its specialty finance and collateral management segment. The company has undergone leadership changes, including elevating its interim CEO to full CEO, while resolving significant litigation matters linked to prior disputes. Efforts to enhance tangible book value and expand internationally signal strategic intent amidst risks of delisting and financial instability. Governance with a cybersecurity focus underpins risk management as Beneficient navigates a high-leverage environment with constrained liquidity.

Recent Operating Update

Beneficient's Q3 2026 results reflected acute operational stress characterized by a net loss of $87.4 million and negative reported revenue of $39.1 million [F1], underscoring the severity of its financial challenges. This negative top line suggests not just weak demand but potentially accounting adjustments or reversals associated with collateral valuation or loan servicing metrics typical in specialty finance where revenue recognition can be volatile [S2]. Despite this, the company actively repaid $27.5 million of principal on a significant loan prior to maturity in January 2026 and continues to manage deferred interest obligations under that facility, showing prioritization of debt servicing even under tight liquidity conditions [S18]. These moves suggest an effort to stabilize liabilities amidst high leverage.

Leadership changes mark another critical development: James G. Silk moved from interim to permanent CEO by late June 2026 [S7], signaling a strategic leadership reset possibly aimed at pivoting the company's operational approach or financial strategy. Concurrently, litigation tied to GWG Holdings concluded with court-approved settlements eliminating significant legal overhang from prior years but leaving residual exposures related to indemnification commitments toward former executives [S17]. This settlement removes one layer of uncertainty, yet ongoing litigation risk remains intrinsic given the nature of specialty finance disputes around secured assets.

Additionally, Beneficient's recent engagement to provide collateral management services for a Texas state-chartered bank on secured lending transactions underscores continuing market traction despite overall financial headwinds [S19]. This contract is notable as such agreements often underpin fee income streams critical for improving operating leverage in collateral-related financing sectors.

Business Model Overview

Beneficient operates within the specialty finance realm focused on collateral management services — an intermediary role managing asset quality and security for secured lending transactions. Typically, such firms generate most revenue through fees charged for managing collateral portfolios, interest spreads on lending facilitation, and advisory fees related to securing transactions [S1]. The company’s business success hinges on precise credit risk assessment, operational efficiency in collateral tracking, regulatory compliance, and robust enterprise risk management frameworks.

However, Beneficient's visible financial frailty - notably recurring net losses and severely negative revenue figures - indicates challenges either from impaired collateral values or suboptimal service volumes/mixing impacting fee generation. In capital-intensive specialty finance firms, profitability correlates heavily with origination volume growth and default management efficiency; absence here can pressure margins and cash flows.

Governance embedding cybersecurity oversight led by an experienced CTO reflects awareness of operational risks tied to protecting sensitive borrower and lender data inherent in secured lending workflows. Regular board-committee scrutiny further reinforces adherence to enterprise risk standards crucial for maintaining regulatory compliance and reputational capital in finance sectors [S1].

Industry Structure and Competitive Position

Beneficient situates among specialty finance companies handling complex secured lending operations—peer sets include asset managers like Ares Capital who combine lending exposure with collateral oversight. While peers may benefit from diversified portfolios or stronger capital bases, Beneficient’s smaller scale and pronounced leverage place it at heightened vulnerability during credit cycles or market shifts affecting underlying collateral values.

Its mix of traditional collateral management services coupled with attempts at international expansion could position it uniquely if execution succeeds; however, competition intensifies from larger firms offering integrated fintech-enabled solutions that optimize loan origination-to-collateral monitoring pathways.

Continued litigation settlements reduce some existential risks compared to peers still embroiled deeply in legal disputes; nonetheless, the threat of Nasdaq delisting looming over persistent losses signals competitive survival concerns not typically faced by more established specialty lenders.

Growth Drivers

Key growth drivers include the rising demand for secured lending supported by asset-backed financing trends nationally. Expansion into new geographies aims to tap underserved markets where security-focused financing is underpenetrated [S1]. Strategic partnerships with regulated banks offer access points into underwriting channels and fee-based engagements.

Furthermore, enhancements to collateral management technology—automation for monitoring loan covenants or alerting credit events—could improve margins by lowering operational costs per unit managed. Successful capital raises and financing rounds are vital for scaling capacity aligned with growth plans.

Community engagement efforts around rural prosperity grants may bolster brand goodwill regionally aiding local partnership formations essential for expansion.

Risks and Watchpoints

The foremost risk is continued financial strain exacerbated by heavy leverage—net debt stands roughly at $94 million compared to scant cash reserves at quarter-end—amplifying liquidity pressures limiting agile responses to market disruptions [F1]. This leverage challenge dovetails with exposure to borrower defaults that could impair collateral values further dragging profitability downward.

Regulatory compliance mandates heighten complexity especially concerning cybersecurity governance and reporting requirements; failure here risks sanctions damaging reputation directly affecting business continuity [S4]. Despite settled GWG litigation claims removing some uncertainties, ongoing legal actions regarding indemnifications implicate reputational damage potential.

The possibility of Nasdaq delisting due to sustained losses threatens investors' confidence undermining secondary financing opportunities crucial for turnaround execution. Market volatility influencing asset valuations compounds this uncertainty as does fluctuating interest rates impacting debt servicing costs.

What to Watch Next

Upcoming milestones include monitoring quarterly revenue stabilization or improvement signaling recovery in fee income from core collateral services. Progress reports on tangible book value enhancement strategies announced in the annual filing will indicate effectiveness in rebuilding shareholder equity buffers.

Successful execution of international expansion plans will be pivotal; announcements detailing client additions or geographic rollouts should serve as positive demand markers.

Leadership communications under CEO Silk will be critical for understanding strategic refinement addressing operating inefficiencies alongside cost control measures. Litigation-related disclosures concerning remaining indemnification exposures warrant observer attention given their possible financial impact.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments