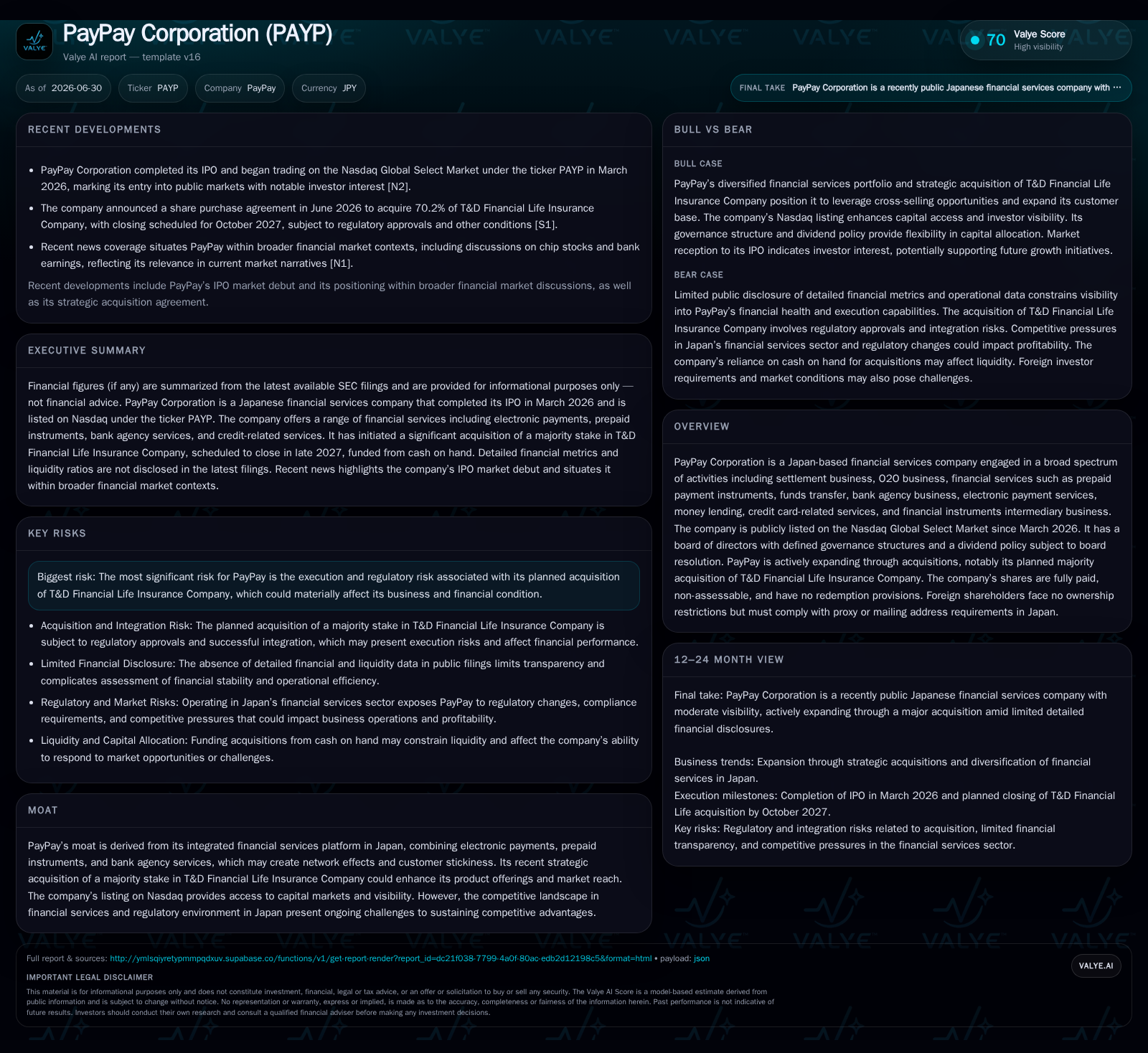

PayPay Corp’s Strategic Pivot: Acquisition Plans and Platform Expansion in Japan’s Financial Services Sector

PayPay's recent quarterly disclosures highlight acquisition ambitions and platform growth amid evolving regulatory demands in Japan's financial services.

The June 2026 interim filings from PayPay Corporation reveal a strategic inflection marked by a planned majority acquisition of T&D Financial Life Insurance Company, broadening its footprint beyond payments and lending into insurance intermediation. This move complements PayPay’s integrated financial services platform, which leverages transaction fees, lending interest, and brokerage commissions to drive revenue. However, these expansions expose the company to regulatory complexity and execution risk, particularly around capital adequacy and AML/CFT compliance enforcement. PayPay's competitive challenge is to deepen network effects and cross-service retention while managing multi-jurisdictional oversight in a highly regulated market.

June 2026 Interim Update Anchors Strategic Expansion Narrative

PayPay Corporation’s latest quarterly disclosures as of June 30, 2026, foreground a critical pivot in the company’s growth trajectory with its announced plan to acquire a controlling 70.2% stake in T&D Financial Life Insurance Company [S3]. This acquisition signals PayPay's deliberate push beyond its established core in electronic payment services and consumer finance into the insurance intermediation space. The deal positions the company not merely as a payments facilitator but as an integrated financial services platform competitor in Japan’s fragmented yet heavily regulated market.

The June filings also emphasize governance continuity as the results of voting rights exercise at the 8th Annual General Meeting reflected stable shareholder support for current management strategy [S2]. This backdrop bolsters confidence that the company's expansion initiatives have board-level endorsement amidst ongoing operational challenges.

Integrated Financial Services Platform: Revenue Model and Service Synergies

PayPay operates across multiple segments within financial services: electronic payment processing including prepaid payment instruments; bank agency business enabling funds transfer and settlement; money lending including small loans; credit card-related products; online brokerage via PayPay Securities; and now with insurance brokerage following the T&D Financial Life acquisition [S1]. This complex product mix generates revenues through distinct mechanisms:

- Transaction fees on digital payments underpin consistent service-related income streams.

- Interest income from the loan book drives net interest margins intrinsic to lending activities.

- Brokerage commissions yield fee-based revenues from intermediary securities business.

- Insurance distribution introduces additional commission revenues tied to policy sales.

By consolidating these services under one umbrella platform, PayPay aims to harness network effects that improve customer retention and reduce churn. Cross-selling insurance alongside finance products may raise customer lifetime value while enhancing switching costs toward competing platforms.

Regulatory Compliance Environment Shapes Operations and Risk Management

Operating as a registered financial instruments business operator subjects PayPay to rigorous regulatory oversight by Japan's Financial Services Agency (FSA). PayPay Securities’ regulatory capital adequacy ratio stood at a robust 301.7% as of March 31, 2025—well above the minimum requirement of 120%—reflecting prudent capitalization standards required under the Financial Instruments and Exchange Act (FIEA) [S1]

AML/CFT compliance forms another cornerstone of operational risk management. The company endured an FSA inspection in 2021 identifying necessary improvements in anti-money laundering systems at its banking subsidiary [S1]. Remediation efforts concluded successfully with confirmation from the FSA by June 2024; however, AML/CFT remains an evolving compliance frontier with potential future risks including administrative inquiries or penalties should lapses occur

Moreover, PayPay faces heightened scrutiny related to its major shareholder status in banking/subsidiary entities: Should authorizations be revoked due to regulatory infractions or shifts in policy interpretation, the company must reduce holdings below defined thresholds within set periods or face enforcement actions ranging from forced divestiture to suspension of operations [S1]. This creates material execution risk especially during rapid business model expansions.

Acquisition-Driven Product Expansion: Implications of T&D Financial Life Integration

The announcement on June 4, 2026 clarified PayPay's intent to integrate T&D Financial Life Insurance as a majority-owned subsidiary with an acquisition price near ¥132 billion excluding related expenses [S3], [S25]. Strategically this move diversifies revenue base by embedding insurance brokerage alongside existing financial products, enhancing cross-selling possibilities within its digital ecosystem.

This expansion elevates PayPay's status closer to a fully integrated financial group paralleling traditional financial conglomerates. However, it also intensifies regulatory complexities relating to insurance sector controls governed separately under Japanese law. The company is likely confronting increased compliance costs alongside operational challenges integrating underwriting practices with digital finance capabilities.

Competitive Positioning Amid Fintech Innovators and Traditional Banks

Within Japan’s rapidly digitizing payment landscape, PayPay competes with fintech innovators such as PayPal internationally and domestic digital wallets like LINE Pay whose focus is predominantly on user-friendly electronic payments. The multi-product strategy employed by PayPay potentially offers deeper engagement through bundled offerings compared with single-service providers.

Against established banking groups like Mizuho Financial Group that combine retail banking scale with comprehensive regulatory expertise, PayPay differentiates itself through agility driven by Nasdaq-listed capital market access enabling expansion investments including acquisitions [S1]. Nonetheless, balancing innovation with regulatory adherence remains essential for competing effectively.

Pricing power derives from diversified fee structures — transaction fees remain sensitive to volume growth trends; lending operations contribute steady net interest margins; brokerage commissions supplement fee income—varied revenue sources provide some buffer against unit cost pressures inherent in high-compliance environments.

Growth Opportunities through Network Effects and Cross-Service Customer Retention

Increasing digital payment adoption combined with O2O (online-to-offline) commerce growth creates fertile ground for scaling transaction volumes—a primary metric influencing fee revenue expansion. By extending offerings through insurance intermediation post-T&D acquisition, PayPay locks customers into wider product suites promoting stickiness.

Customer retention metrics are critical here: binding users across payments, lending, brokerage, and now insurance functions leverages network effects reducing churn rates while improving cross-sell ratios, thereby increasing average revenue per user (ARPU). This integrated approach parallels successful models among global fintech leaders who monetize embedded finance strategies effectively.

Operational Watchpoints: Execution Risks and Regulatory Uncertainties Ahead

Notwithstanding strategic promise, significant risks prevail. Integration execution challenges loom large with T&D Financial Life bringing legacy insurance operations requiring cultural alignment and IT system harmonization.

Regulatory environment volatility presents continuous uncertainty—Japan’s evolving AML/CFT regulations demand sustained investment in compliance infrastructure. Any lapses risk enforcement actions impairing operations or reputation damage.

Moreover, cybersecurity threats form a high priority given extensive use of online platforms handling sensitive financial data across multiple service lines. Robust governance involving designated Chief Information Security Officer responsibilities reflects management awareness yet requires vigilant ongoing effort.

Finally, macroeconomic variables impacting consumer credit quality influence delinquency rates in loan books affecting net interest income stability. Monitoring these KPIs will be essential to proactively mitigate credit risk exposures.

This analysis synthesizes publicly filed disclosures without recommending any investment action. It aims to elucidate key operational developments shaping PayPay’s shifting competitive landscape within Japan's integrated financial services sector based on verified SEC sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments