GSR V Acquisition Corp. IPO Funding and Initial SPAC Structure Define Early Operational Landscape

GSR V Acquisition Corp. recently closed a significant IPO, establishing capital reserves that set the stage for its initial business combination efforts within typical SPAC timelines.

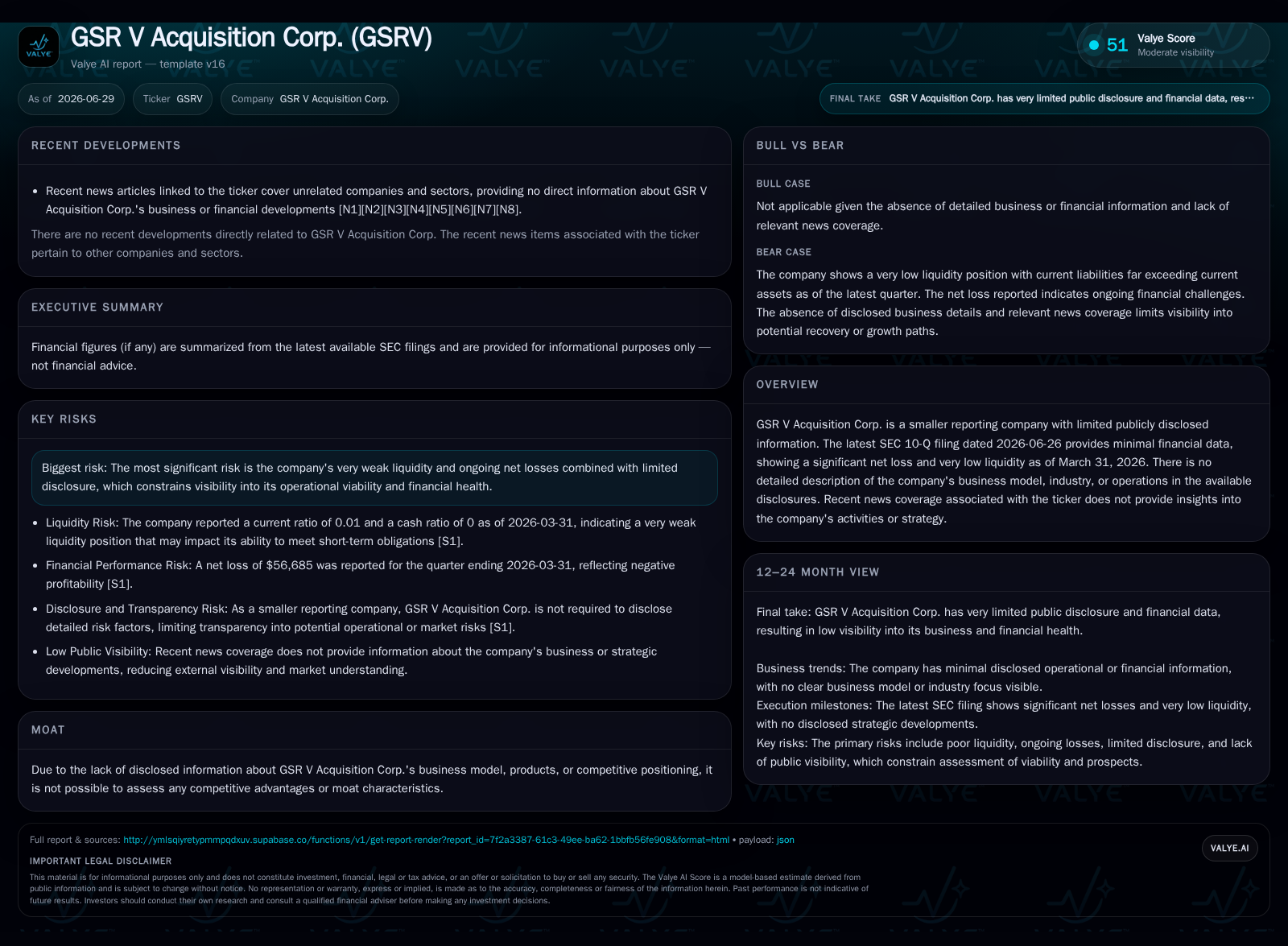

GSR V Acquisition Corp. completed its initial public offering on May 15, 2026, raising gross proceeds of $230 million through units sold at $10 each, including an over-allotment exercise and private placement units. These proceeds have been secured in a segregated trust account, consistent with standard SPAC practices awaiting a de-SPAC transaction. The company currently exhibits minimal operating activity and financial metrics characteristic of an early-stage SPAC without a completed business combination, such as substantial net loss and negligible liquidity outside the trust account. Its operational model aligns with the typical intermediary role SPACs play between public investors and private companies seeking public valuation access. Key risks include constrained liquidity from funds held in trust pending acquisition and the limited timeframe to consummate a business combination before mandatory liquidation.

Recent Operating Update

GSR V Acquisition Corp. successfully completed its initial public offering (IPO) on May 15, 2026, issuing approximately 23 million units at $10 each inclusive of a fully exercised over-allotment option [S3]. Each unit consists of one Class A ordinary share and one-seventh of one right, where rights allow holders to receive additional shares upon de-SPAC transaction completion [S7]. The IPO alongside private placement unit sales raised gross proceeds totaling approximately $236.7 million. Crucially, almost all these funds were placed in a segregated U.S.-based trust account managed by Odyssey Transfer and Trust Company acting as trustee—standard practice to safeguard investor capital until used for an initial business combination [S3].

No material changes were reported in the latest quarterly filing dated June 29, 2026 [S2]; it emphasize that GSR V remains an emerging growth company with minimal operating activity before the completion of any target acquisition.

Business Model Overview

As a Special Purpose Acquisition Company (SPAC), GSR V's business model centers on raising capital via its IPO pipeline—proceeds from units issued are held in trust accounts earning interest—and then using these funds to acquire or merge with a private company that seeks faster access to public markets through a streamlined alternative to traditional IPOs. Until such merger or acquisition occurs (commonly called de-SPAC transaction), the company does not generate operating revenues nor profits but incurs expenses mainly related to administration and compliance.

The issuance structure involving Class A shares bundled with fractional rights followed by exercise mechanisms reflects industry-standard instruments designed to balance investor protections with sponsor economics [S7]. Furthermore, the presence of private placement units purchased by sponsors underscores alignment incentives common among SPAC sponsors who commit 'at-risk' capital upfront with potential upside upon successful transaction closure.

Industry Structure and Competitive Position

Within the broader SPAC ecosystem—which includes peers like Pershing Square Tontine Holdings or Churchill Capital Corp.—GSR V occupies the standard shell intermediary role. It raises funds from institutional and retail investors under regulatory frameworks that require placing IPO proceeds into trust accounts neutralizing day-to-day operational risk exposure for investors.

Competition among SPACs operates primarily on securing quality private targets swiftly within mandated time horizons (usually 18-24 months). Sponsor reputation and prior deal success critically factor into market confidence but are not detailed for GSR V in disclosures [S6]. The absence of disclosed acquisition candidates or strategic sector focus positions GSR V as a blank-check vehicle targeting potentially broad sectors subject to market opportunities identified by its sponsor team.

Capital market factors influencing SPAC performance include prevailing investor appetite for alternative vehicles, cost-of-capital considerations affecting redemption decisions, and regulatory evolutions impacting SPAC structuring nuances.

Growth Drivers

GSR V’s growth trajectory is conditional on successfully sourcing an attractive private company for merger within the allowable timeframe before automatic liquidation demands return of invested funds [S12]. Its $236.7 million pool places it within moderate-sized SPAC offerings capable of acquiring mid-market targets.

Key drivers supporting deal execution include favorable equity market conditions encouraging de-SPAC transactions; availability of experienced sponsors engaged via private placement agreements; structured redemption rights balancing shareholder exit options versus capital retention; and innovations in unit-right instruments enhancing investability [S3], [S7].

Investor interest in faster public listing routes amidst regulatory complexity boosts demand for SPACs as underwriting facilitators. Achieving above-average shareholder redemption containment would indicate market confidence in GSR V's proposed targets when announced.

Risks and Watchpoints

Liquidity constraints outside the trust remain acute per Q1 balance sheet showing only $958 USD in current assets against $128,583 USD current liabilities resulting in an extremely low current ratio (~0.01) [F1]. While cash locked in trust mitigates default risk on capital deployed later for acquisitions, these limited operating liquid assets constrain short-term expense flexibility absent sponsor funding.

SPAC-specific risks center on failure to complete an initial business combination within around 18 months from IPO closing or any extended sponsor discretion period leading to mandatory liquidation — risking capital return but no upside gains for public holders [S12]. Redemption rights can reduce available proceeds if large shareholders exercise them in connection with proposed deals, complicating financing calculations.

The absence of disclosed target companies or strategic sector focuses reduces visibility into potential deal economics and competitive positioning. Sponsor incentives may conflict with shareholder interests if pressure mounts to consummate any deal instead of optimizing target quality or price.

Positive progression along these dimensions would confirm GSR V’s transition from capital raising shell toward an operating public entity.

Financial Profile Discussion

GSR V’s latest reported net loss approximates $56,685 USD as of March 31, 2026 reflecting pre-business combination expenses largely administrative in nature [F1]. Meanwhile, reported short-term liquidity disparities show only nominal current assets ($958 USD) against substantially higher liabilities ($128,583 USD), yielding a current ratio near 0.01 that evidences lack of working capital outside the trust account intended primarily for M&A activity [F1]. This financial profile aligns exactly with early-stage SPAC characteristics where operating results are heavily loss-making until revenue generation commences post-acquisition closure.

The company's segregation of nearly all IPO proceeds totaling over $230 million into an independently managed U.S.-based trust account provides assurance that primary capital earmarked for acquisitions remains intact pending deployment or return at liquidation [S3]. This segregation mechanism is fundamental to preserving investor value but limits operational liquidity necessitating sponsor support for ongoing corporate functions pre-merger.

Overall liquidity outside trust-driven resources constrains purely corporate expense headroom but is typical since monetization events only arise following successful de-SPAC execution across industry peers.

This analysis synthesizes publicly available SEC filings through June 29, 2026 alongside industry-standard context frames applicable to Special Purpose Acquisition Companies (SPACs). All forecasts remain subject to change pending future disclosures about business combinations or operational initiatives by GSR V Acquisition Corp. This document aims solely to contextualize recent developments without providing investment research views or valuations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments