Iron Dome Acquisition I Corp.: IPO Capital Structure and Initial Business Combination Prospects

Iron Dome Acquisition I Corp. holds over $150 million in trust post-IPO, focusing on securing a suitable business combination within an 18-month deadline.

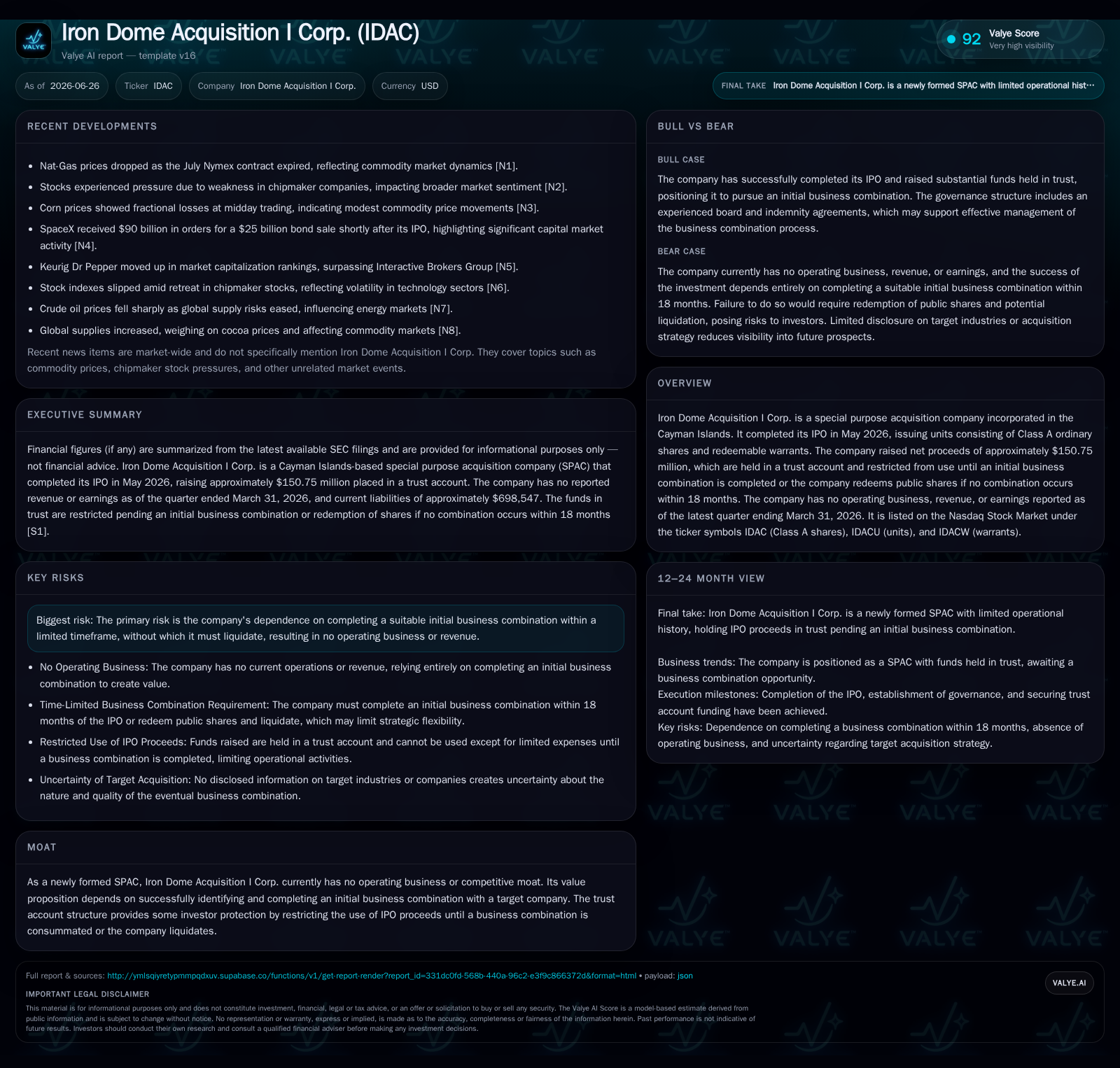

As of its latest 10-Q filing dated June 26, 2026, Iron Dome Acquisition I Corp. remains a pure special purpose acquisition company (SPAC) with no operating business and approximately $150.75 million net IPO proceeds secured in a trust account. The company's capital structure includes Class A ordinary shares bundled with redeemable warrants and private placement warrants held by its sponsor, balancing investor protections with potential dilution risks. With roughly eight months remaining to consummate an initial business combination or face liquidation, shareholder redemption rights and timing constraints loom as critical factors for deal execution. Iron Dome operates amid a competitive SPAC environment where sponsor reputation, deal pipeline quality, and market conditions will largely influence success.

Latest Quarterly Filing Update: IPO Proceeds Held Secure in Trust Account

Iron Dome Acquisition I Corp.'s most recent quarterly report filed on June 26, 2026 ([S2]) confirms its status as a special purpose acquisition company (SPAC) with no operating revenues or earnings. The company raised net proceeds of approximately $150.75 million from its May 2026 initial public offering (IPO) combined with a private placement of warrants. These funds are held in a trust account administered by Odyssey Transfer and Trust Company for the benefit of public shareholders and underwriters ([S3]). Withdrawals from this trust are tightly controlled—allowed only for tax payments funded by interest earned or for redemptions aligned with amended governance provisions.

At quarter-end March 31, 2026, Iron Dome reported minimal liabilities under $700,000 and total debt around $136,585 ([F1]), reflecting a clean balance sheet optimized for deploying capital toward an initial business combination without legacy leverage burdens.

Capital Structure: Units, Warrants, and Sponsor Alignment

Iron Dome’s IPO followed conventional SPAC structuring: it issued units each consisting of one Class A ordinary share plus one-half of one redeemable warrant exercisable at $11.50 ([S3],[S7]). This design balances equity participation with long-term upside via warrants while introducing typical dilution risk upon exercise post-business combination.

The sponsor acquired 2.75 million private placement warrants at $1 per warrant before IPO closing ([S15]). These warrants mirror public warrants but include transfer restrictions until after the business combination closes. This aligns sponsor incentives closely with successful deal completion while granting registration rights supportive of liquidity.

Such structures are common among SPACs but carry strategic implications: warrant dilution can pressure post-merger equity value if exercised broadly; however, they serve as important incentives for sponsors and early investors seeking enhanced returns.

Redemption Rights: Investor Protections vs Deal Execution Complexity

Shareholders hold redemption rights embedded in Iron Dome’s amended memorandum and articles effective May 14, 2026 ([S6],[S9]). Public shareholders may redeem their Class A shares before or concurrent with the initial business combination at a per-share price based on trust account value less expenses.

While these rights protect investors against unsatisfactory deals or delays, they introduce execution risks for sponsors. High redemption levels reduce merger proceeds available for financing acquisitions or providing growth capital to targets.

Additionally, amendments affecting redemption terms require shareholder votes with quorum thresholds—a procedural complexity affecting deal structuring under varying market or regulatory conditions.

Competitive Context: Mid-Sized SPAC Within Broader Market Landscape

Within the active mid-2026 SPAC market, Iron Dome’s approximately $150 million raise situates it in a mid-tier range compared to mega-SPACs like Pershing Square Tontine Holdings (PSTH), which raised multiple billions.

It benefits from standard industry safeguards including an underwriting agreement led by Santander US Capital Markets LLC and comprehensive governance agreements ensuring management accountability ([S11],[S16]).

While lacking scale advantages of serial multi-SPAC operators such as Social Capital Hedosophia Holdings, Iron Dome’s success depends on leveraging sponsor expertise and credible deal sourcing amid competition for high-quality private targets seeking faster public access than traditional IPOs.

Traditional IPO peers face longer timelines and more regulatory hurdles relative to SPACs promising expedited listing contingent on swift deal closures.

Growth Drivers: Market Demand and Sponsor Execution

Growth prospects depend on favorable market conditions fueling demand for SPAC-led business combinations: strong investor appetite for alternative vehicles; regulatory frameworks supporting streamlined de-SPAC transactions; and a growing pool of private companies seeking liquidity without traditional IPO complexities.

Sponsor reputation is critical; experienced sponsors can attract better targets and secure supportive PIPE financing enhancing transaction viability.

The fixed 18-month timeframe from IPO closing imposes urgency on due diligence and negotiations to close deals efficiently.

Risks and Watchpoints: Deadlines, Redemptions, Dilution

Key risks include failure to consummate an initial business combination within the mandated 18 months post-IPO (expiring November 2027), triggering mandatory liquidation returning remaining trust funds net expenses to shareholders ([S9]).

High shareholder redemptions could substantially reduce proceeds available for acquisitions, complicating deal financing.

Warrant dilution from exercises at below-market prices ($11.50) may pressure equity values post-merger. Combined effects of redemptions and dilution could weigh on initial public market performance after business combination.

Additional risks involve regulatory scrutiny over disclosures and potential conflicts between sponsor incentives versus public shareholder interests.

What To Watch Next: Deal Progress Milestones

Investors should monitor announcements identifying target companies selected for combination discussions along with filings signaling progress such as governance amendments or proxy solicitations for shareholder votes.

PIPE financing arrangements would indicate institutional investor confidence vital for transaction funding stability.

As the IPO anniversary approaches, timing pressures will intensify; any extension requests require shareholder approval adding negotiation complexity.

Transparency regarding deal pipeline quality through disclosures will be key to setting realistic expectations among investors.

This analysis is based solely on filings through June 26, 2026 ([S2],[S3],[F1]) without speculation beyond disclosed facts. It aims to clarify structural aspects influencing Iron Dome Acquisition I Corp.'s strategic outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments