VIDA Global’s Early-Stage AI Agent Platform Faces Commercialization and Regulatory Challenges

VIDA Global’s Q1 2026 results underline early-stage commercialization risks amid evolving AI agent SaaS market dynamics and partner dependency.

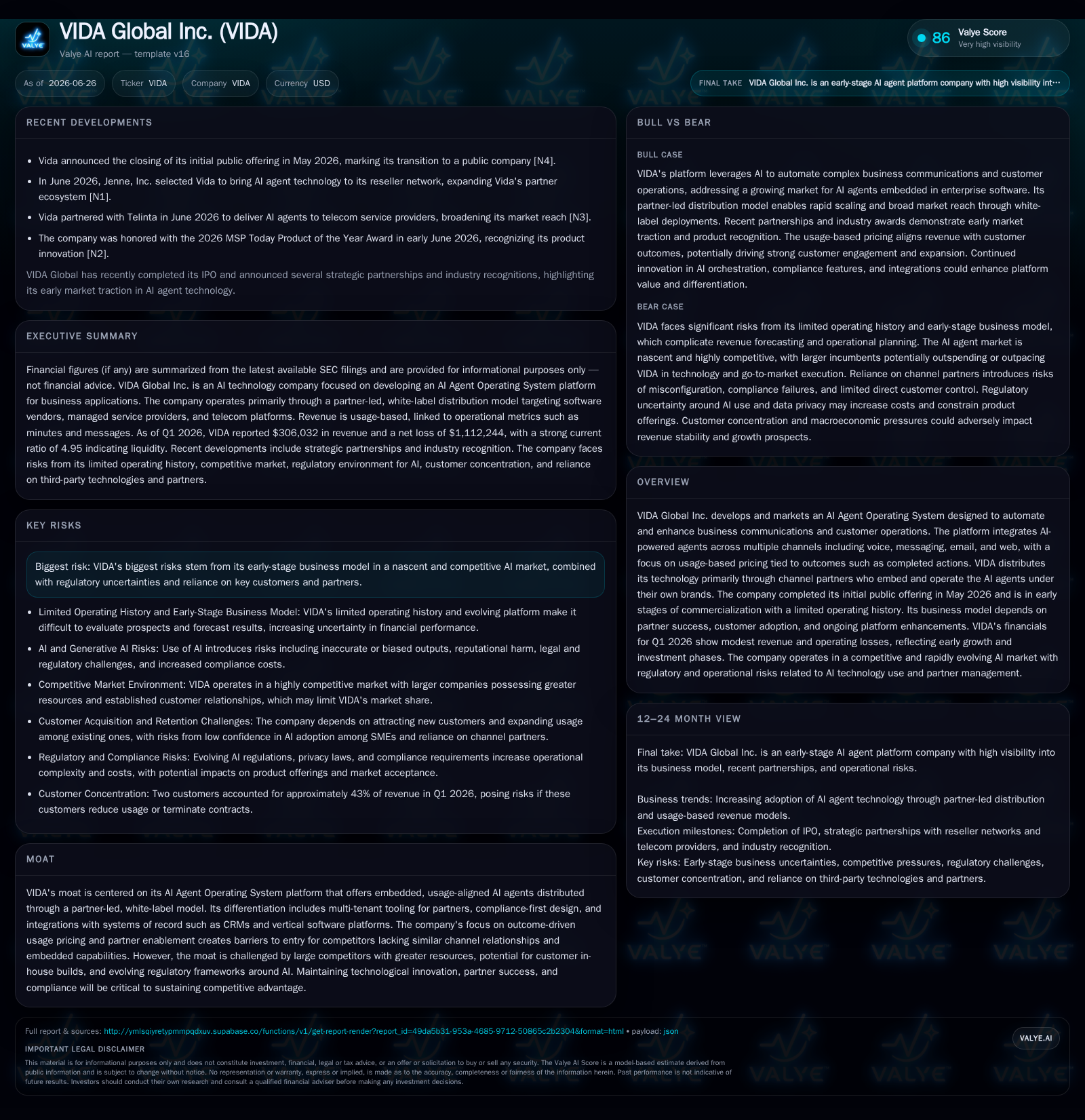

VIDA Global Inc., having recently completed its IPO in May 2026, operates an AI Agent Operating System designed for partner-led, usage-based deployments across multiple communication channels. The company’s latest quarterly filing reveals modest revenue generation alongside significant operating losses, reflecting typical early commercialization challenges and uncertainties in demand forecasting. VIDA's business model strongly hinges on channel partners embedding its AI technology under their brands, creating a differentiated usage-driven pricing structure but also concentrating execution risk. The competitive landscape is intense with large tech incumbents active in adjacent spaces, while regulatory complexities around AI usage elevate compliance costs and risk exposure. The path to growth requires accelerating partner adoption, ramping up customer usage volumes, and maintaining innovation amidst rapidly shifting legal frameworks.

Recent Operating Update: Early Commercial Traction with Modest Revenues Reflecting Growth Phase

VIDA Global reported Q1 2026 revenue of $306K alongside an operating loss of approximately $887K as it navigates from development into commercialization following its May 2026 IPO [F1], [S2]. This financial snapshot typifies nascent SaaS players building partner networks and customer usage in a complex enterprise arena. Modest top-line results underscore the still limited scope and scale of deployments despite initial product-market fit signals through embedded launches with channel partners. Revenue recognition is closely tied to outcome-driven metrics such as voice minutes used or completed actions like payments processed, tightly aligning income to platform utility rather than traditional seat-license procurement models [S11]. This approach introduces volatility related to end-user engagement variability and seasonality in industries served.

Business Model: Usage-Based AI Agents via Partner-Centric White-Label Distribution

VIDA’s core offering is a cloud-hosted AI Agent Operating System that integrates generative AI across multiple communication channels—voice calls, SMS/MMS messaging, emails, and web interactions—to automate business processes like scheduling appointments or customer payments. The platform is designed for multi-tenant use by channel partners who embed VIDA’s agents under their own branding into their software or service stacks. This white-label approach focuses VIDA as an enabler rather than direct service provider to end customers, controlling technical infrastructure while relying on partners for sales execution and customer relationship management.

Revenue is generated predominantly via usage-based pricing tied directly to successful outcomes (actions completed by AI agents) rather than fixed seats or subscription tiers common in legacy SaaS models. This outcome-driven billing reflects a deeper alignment with client ROI but demands high-quality agent performance and sustained user engagement to drive healthy margins. VIDA also offers integrations with upstream systems of record such as CRMs or vertical industry platforms to enable seamless data flow and orchestration.

Strategically, the model leverages partner enablement through multi-tenant tools facilitating administration, compliance enforcement (e.g., adherence to telemarketing laws), and billing configuration across heterogeneous client bases. While this provides scalability benefits and partner stickiness potential, it inherently concentrates risk around partner success and timely commercialization of embedded features.

Industry Structure and Competitive Context

VIDA operates within the emergent Software as a Service (SaaS) segment focused on AI-powered agent platforms aimed at automating customer-facing operations—a niche characterized by ongoing rapid innovation but immature demand patterns. Key industry players include established cloud vendors expanding into generative AI-enhanced workflows, specialty CRM providers embedding similar automation capabilities, telecom service platforms offering unified communications-as-a-service (UCaaS), and an array of emerging startups targeting vertical-specific use cases.

The competitive landscape pressures VIDA due to large incumbents’ scale advantages in R&D spending, distribution breadth, bundled offerings combining AI with broader suite products, and entrenched sales relationships. Many competitors prioritize seat-based or feature-bundled pricing models contrasting VIDA’s pure usage-outcome billing strategy which can complicate direct price benchmarking but offers differentiation on alignment with customer value delivered.

Rapidly evolving regulatory regimes around artificial intelligence—including the EU’s comprehensive Artificial Intelligence Act—alongside telemarketing statutes like TCPA impose an increasingly complex compliance environment unique to this SaaS niche. Compliance-first design in VIDA’s platform aims to mitigate these risks but demands ongoing investment in security controls, audit capabilities (e.g., call recording redaction), consent management workflows, and domain-specific configurations for regulated sectors such as healthcare or finance.

Growth Drivers: Expanding Adoption Through Usage Expansion and Partner Ecosystem Scale

VIDA’s growth trajectory depends critically on accelerating partner adoption rates—both onboarding new channel partners and deepening integration within existing ones—to expand footprint across various industry verticals including home services, healthcare enrollment windows, retail marketing campaigns, and logistics coordination where multi-channel agent automation yields measurable productivity gains.

Usage volume growth — measurable through completed agent actions or interaction minutes consumed — underpins recurring revenue expansion given the outcome-driven price model [S11]. Increased feature adoption such as new workflow automations or additional communication channels can also drive upsell within installed bases benefiting net revenue retention metrics.

Another growth vector lies in improving agent capabilities leveraging advancements in generative AI models allowing higher accuracy automation tasks; this fosters better ROI narratives necessary for convincing risk-averse enterprises to replace legacy seat-license systems or internal builds. Regulatory clarity emanating from frameworks like the US Executive Order on AI policy may reduce barriers for broader deployments across geographies [S14].

Finally, strategic partnerships announced post-IPO (e.g., collaborations with Telinta targeting telecom providers and reseller networks like Jenne Inc.) hint at increasing traction in channel ecosystems that can multiply go-to-market coverage without proportional increases in direct sales staffing costs [N1],[N2],[N3].

Risks and Constraints: Commercialization Uncertainty Amid Regulation and Partner Dependence

VIDA faces well-documented risks from its early-stage status: limited historical data constraining reliable growth forecasts; lengthy integration cycles typical for embedded agent rollouts; sensitivity of usage volumes to campaign timings or macroeconomic fluctuations; plus concentrated revenue exposure accounting for two customers representing over 40% of recent quarterly revenues [S7],[S22]. Loss or reduced usage from any major client could materially impact financial results.

Operational complexity inherent in managing distributed partner ecosystems adds unpredictability around timing of launches as partners juggle competing product roadmaps and technical priorities [S29]. Further complexity arises from evolving telecommunications regulations governing automated outreach which influence both product design decisions and go-to-market strategies.

Legal risks particular to IP infringement claims loom especially as VIDA leverages third-party generative AI models whose licensing terms continue dynamic change; material weaknesses identified in internal controls over financial reporting suggest further operational refinement is needed as public listing imposes greater scrutiny [S8],[S21].

The company’s treasury also holds bitcoin exposure positing volatility risk uncommon amongst traditional SaaS peers yet reflecting management’s alternative asset views [S25]. Lastly, reliance on a small number of major partners increases counterparty risks including credit issues or strategic realignments away from VIDA products.

What to Watch Next: Partner Rollouts, Usage Growth Metrics, Compliance Milestones

Key upcoming milestones include successful embedded launches with existing channel partners demonstrating scalability of usage adoption beyond initial pilots; monitoring ARR growth anchored to increased volume consumption metrics will be essential indicators of stickiness within end-customer operations.

Regulatory developments around artificial intelligence governance present ongoing watchpoints—particularly regarding cross-jurisdictional compliance with evolving EU AI Act provisions or US telecommunication regulations—which may trigger additional platform modifications or cost structures.

Operational execution around remedying identified internal control weaknesses will also impact investor confidence during this critical growth phase. Investor attention will focus on quarterly updates reflecting improvements in sales cycle durations coupled with efficiency gains in partner enablement processes.

Monitoring competitive reactions from larger SaaS incumbents incorporating similar agent functionalities into broader unified suites will provide clues on margin pressures or feature parity battles going forward.

Financial Profile Highlights: Early Revenue Generation Backed by Strong Liquidity Cushion

From a financial perspective based on the latest Q1 2026 data filed June 26th [F1], VIDA generated just over $300K in revenue but reported an operating loss near $887K indicative of continued investments in R&D infrastructure befitting early commercial-stage SaaS firms.

Liquidity appears sufficient near term given current assets of approximately $2.1 million against current liabilities of $424K, implying a current ratio near 4.95x as of March 31, 2026 [F1]. Operating cash burn is contextualized alongside planned capex for compliance programs (e.g., SOC 2 certifications) plus engineering headcount additions detailed in filings [S21], requiring close monitoring amid variable revenue conversion timing tied to unpredictable partner launches.

Gross margin volatility is expected given outcome-based usage pricing varies with end-customer activity levels influenced by economic cyclicality within verticals such as retail marketing campaigns or healthcare enrollments noted by management commentary. Future margin improvement potential hinges on scaling fixed-cost leverage while stabilizing consumption patterns.

This analysis emphasizes VIDA Global's positioning as an emergent player leveraging channel-centric usage-priced AI agents during early commercialization stages fraught with adoption uncertainties alongside regulatory flux inherent to the evolving generative AI SaaS landscape. Continued success will rely heavily on execution against lengthening sales cycles through durable partner relationships while navigating multifaceted legal-compliance environments specific to automated customer engagement technologies. Investors should watch traction manifested through growing usage volumes commanded by increasingly sophisticated agents delivered via trusted partners coupled with visible mitigation of operational control gaps revealed through recent public disclosures.

This report is intended solely for informative purposes based on disclosed filings and industry context; it does not constitute investment advice.

Financial position in context

Current assets of $2.1 million and current liabilities of $424,264 imply a current ratio near 4.95x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments