Biohaven Ltd.'s R&D-Heavy Model and Capital Structure Crimp Near-Term Financial Returns

Biohaven remains a clinical-stage biopharma with no product revenue, facing significant development risks and debt covenants tied to its flagship asset's approval.

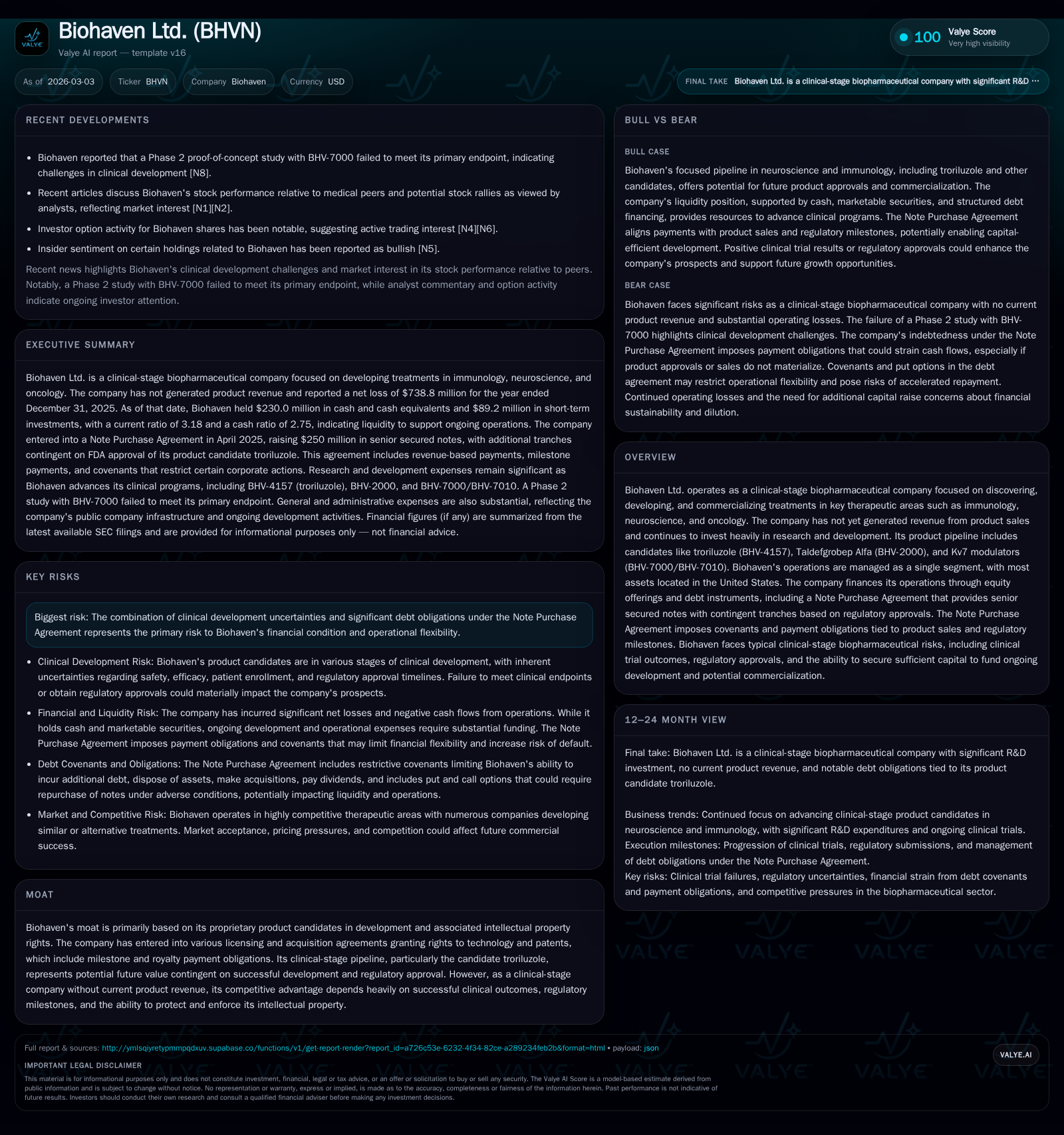

Biohaven Ltd. has sustained operating losses driven by heavy investment in a pipeline focusing on neuroscience, immunology, and oncology treatments. Its financial trajectory is tightly linked to the regulatory approval and commercial success of troriluzole, currently the centerpiece asset under a $600 million Note Purchase Agreement with milestone and royalty payments that impose operational constraints. Despite incremental improvement in losses year-over-year through 2025, Biohaven continues to burn substantial cash with no near-term revenues expected. Monitoring FDA milestones and managing debt covenants will critically influence future liquidity and growth potential.

Historical Performance

Biohaven Ltd. remains a quintessential clinical-stage biopharmaceutical company with operations concentrated primarily in the United States but incorporated in the British Virgin Islands [S1][S24]. The company has yet to generate any revenue from product sales and does not expect near-term revenues until one or more of its product candidates – led by troriluzole (BHV-4157) – achieve regulatory approval and enter the market [S1][S20].

As highlighted in its recent annual filings through December 31, 2025, Biohaven’s operating income has been deeply negative but showed a moderating trend: operating losses reduced from approximately -$885 million in 2024 to around -$745 million in 2025, reflecting a roughly 16% year-over-year improvement [F1]. Net losses followed a similar trajectory, improving about 13% YOY yet still exceeding $730 million in the latest fiscal year [F1]. This level of loss is typical for companies heavily invested in costly clinical trials across multiple therapeutic domains such as immunology, neuroscience, and oncology.

Research & development spending represents the largest portion of operating expenses. These costs encompass payments to contract research organizations (CROs), manufacturing scale-up expenses through contract manufacturers (CMOs), personnel salaries, compliance activities, development milestones tied to licensing arrangements prior to approval, and facilities expenses for labs and offices [S1]. While specific per-program R&D expense allocations exclude internal employee-related expenses (which are spread across programs), external direct costs are assigned program-by-program based on contracts with CROs/CMOs [S1].

Capital expenditures trended downward significantly from roughly $4 million in fiscal 2024 to under $1 million in 2025 as Biohaven emphasized clinical activities over physical infrastructure growth [F1], consistent with a typical late-investment stage biotech strategy.

The following table summarizes key financial metrics from FY 2022 through FY 2025:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -739 | -609 | -745 | 1 | +12.7% |

| 2024 | -846 | -582 | -885 | 4 | -107.4% |

| 2023 | -408 | -332 | -436 | 3 | +28.4% |

| 2022 | -570 | -298 | -568 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -610 | -1418.8 |

| 2024 | -587 | -199.9 |

| 2023 | -335 | -95.4 |

| 2022 | -304 | -105.8 |

Source: SEC companyfacts cache [F1].

Note: Current assets and liabilities data available only for FY2025 allowing calculation of current ratio.

Future Growth Prospects

Biohaven’s growth is contingent on achieving key developmental milestones associated largely with troriluzole’s clinical progress and successful regulatory approvals primarily from the FDA and EMA [S1][S15]. The pipeline also includes Taldefgrobep Alfa (BHV-2000) targeting fibrosis indications and Kv7 modulators (BHV-7000/BHV-7010), with respective research advancing but none having achieved commercial status yet [N1][N2][S24].

Notably, Biohaven's Note Purchase Agreement conditions contingent tranche funding on FDA approval of troriluzole; receipt of that approval would trigger up to $150 million in additional notes issuance before June 30, 2026 [S1][S15]. Beyond this milestone-based funding structure lies an optional third tranche totaling up to $200 million for permitted acquisitions pending mutual consent between parties.

The primary drivers for future revenue generation will revolve around global net sales of troriluzole if approved, which would initiate royalty-like revenue payment obligations under the Notes at an initial rate of around 6.25%, adjustable upward depending on tranche drawdowns post-FDA approval [S1][S15]. Material positive catalysts include: FDA/EMA approvals; successful late-stage trial readouts; establishment of a scalable manufacturing footprint; and potential strategic partnerships or license deals expanding commercialization reach.

Risks constraining growth include typical biopharma uncertainties: enrollment delays; unforeseen safety or efficacy issues; competition from alternative therapeutics; regulatory guideline shifts; intellectual property defense challenges; milestone payment encumbrances embedded within licensing agreements such as those involving Yale University; plus inherent limitations posed by restrictive covenants under existing debt instruments impacting operational flexibility [S8][S10][S20][S22].

Forecasts / Milestones / Expectations

Explicit guidance from Biohaven is limited due to the clinical-stage nature of its operations; however, close monitoring of FDA decisions on troriluzole represents the most immediate inflection point given its linkage to both financing tranches and prospective revenue streams [N4][S1][S15]. Investors should also watch progress on other pipeline assets’ trial advancements as potential secondary revenue drivers or partnership opportunities.

Management expects continued high R&D spending levels reflecting ongoing pivotal studies preparing for regulatory reviews combined with administrative expenses scaling modestly as it builds out a commercialization foundation should approvals materialize [S10][S29]. Internal projections likely factor uncertainties typical for drug development timelines; thus forecasting beyond regulatory milestones remains speculative without concrete disclosures.

Returns / Capital Allocation

Return metrics remain negative given no revenue generation and large operating losses annually since at least FY2022: net income ranged from approximately -$408 million (FY23) worsening beyond -$730 million most recently (FY25), resulting in a deeply negative return on equity upwards of minus fourteen hundred percent (based on last annual net loss divided by equity value) [F1].

Free cash flow stayed negative owing largely to steep cash burn supporting research programs—operating cash flow was nearly -$610 million last year while capex was minimal (~$715k), leaving free cash flow approximately -$610 million as well [F1].

Capital allocation priorities so far have been focused squarely on funding development through equity offerings (including a $188 million common stock issuance closed November 2025) alongside debt financings—no dividends or share repurchases have occurred consistent with the capital-intensive phase prior to any product commercialization generating topline receipts [F1][S16].

The Note Purchase Agreement anchors Biohaven’s capital structure presently: securing an initial principal amount of $250 million in April 2025 with further contingent tranches totaling up to $350 million tied to regulatory events affords vital working capital while imposing strict covenants limiting indebtedness incurrence, mergers/acquisitions outside approved parameters, asset disposals, dividend payments or stock buybacks without lender approval [S5][S15][S26]. The purchasing parties under this agreement also enjoy senior secured rights on cash flows related mainly to troriluzole’s approved products’ sales revenues.

Such arrangements introduce heightened financial risk should expected approvals be delayed or fail—potential defaults could trigger remedy rights including acceleration clauses forcing earlier-than-planned repayment obligations jeopardizing operational continuity absent new funding sources or debt restructuring efforts [S9][S19].

Industry Context (Analysis)

Within biotechnology circles specializing in neurological indications like spinocerebellar ataxia or refractory epilepsy where troriluzole targets lie awaiting validation through registrational studies, companies often require multiyear capital commitments before commercial traction occurs. Licensing pioneering intellectual property platforms—as Biohaven did through agreements including Yale MoDE technology—positions them ahead scientifically but entails complex milestone-backed liabilities that must be carefully managed alongside patent portfolio strategies.

Debt arrangements involving contingent royalties tied directly to specific drug candidates—and adjustable payment percentages depending on performance benchmarks—are increasingly common as biotechs seek non-dilutive financing alternatives responsive to eventual product market success rather than upfront valuation pressures.

This provides both a lifeline for development yet creates structural leverage that magnifies downside volatility relative to broader medical sector peers less reliant on single candidate-dependent financing constructs.

Conclusion

Biohaven Ltd.’s financial profile reflects its identity as an early-stage biopharmaceutical innovator burning significant capital while navigating regulatory milestones critical for commencing revenue generation from novel therapeutics like troriluzole. Its substantial losses juxtaposed against meaningful cash balances shield near-term liquidity but underscore persistent existential business risks inherent in clinical development cycles compounded by senior secured indebtedness containing milestone-contingent funding tranches.

Stakeholders should prioritize tracking FDA decisions related to troriluzole given their dual importance driving both potential future sales receipts triggering debt repayment schedules and unlocking subsequent financing rounds designed for growth acceleration through licensed acquisitions or expanded pipeline investments.

Investors should remain attentive to covenant compliance status amidst evolving trial timelines—and management commentary addressing how Biohaven plans adapting capital structure flexibility given ongoing sizable cash outflows accompanying aggressive R&D investment strategies necessary before sustainable profitability pathways emerge.

This report is prepared solely for informational purposes based on publicly available documents including SEC filings and news reports as referenced herein; it does not constitute investment advice nor an offer or solicitation regarding securities of Biohaven Ltd.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments