Bridgeline Digital Strengthens AI-Powered Marketing Suite Amid Mixed Financial Signals

Latest quarterly results underscore ongoing AI product innovation while highlighting liquidity pressures and renewal risks facing Bridgeline Digital in a competitive Martech environment.

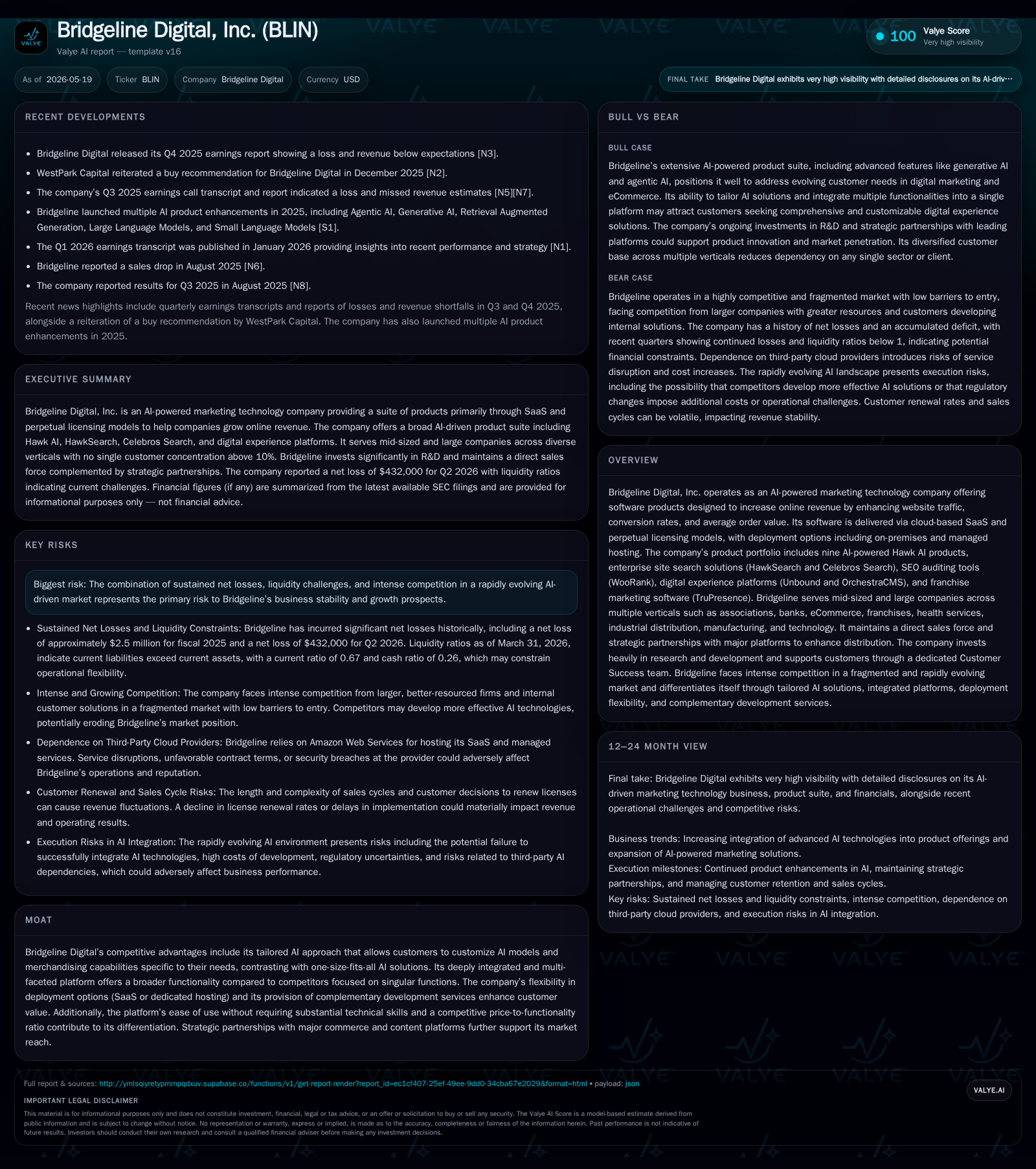

Bridgeline Digital’s May 2026 quarterly 10-Q reveals sustained investments in tailored AI-powered marketing products alongside continued operating losses. The company’s unique Hawk AI suite offers differentiated configurability and multi-functionality attractive to mid-sized and large enterprises. However, a current ratio below 1 reflects tight liquidity, and license renewal rates remain a crucial revenue vulnerability given customer concentration dynamics. Competitive fragmentation and pricing pressure endure industry-wide challenges. Monitoring upcoming renewal data and operating cash flow generation will be pivotal to assessing Bridgeline’s path toward financial stability and growth.

Latest Quarterly Operating Update: Innovation Balanced with Financial Constraints

In Bridgeline Digital’s latest quarterly filing dated May 15, 2026 [S2], there are no material revisions to previously disclosed risk factors [S9], maintaining continuity in the company's risk outlook from its December 19, 2025 annual report [S1]. Despite the absence of new financing or restructuring announcements in recent filings including an April 28 event report [S3], the company continues its cadence of AI-driven product launches central to its growth narrative.

However, financial metrics reveal a cautiously constrained operational environment. As of March 31, 2026, Bridgeline reported cash and equivalents of approximately $1.37 million against current liabilities totalling about $5.21 million — reflecting a current ratio of approximately 0.67 — underscoring near-term liquidity tightness [F1]. No new significant debt financing has been disclosed recently to offset this gap.

Operating losses persist as a feature of Bridgeline’s cost structure growth model; the firm posted net losses historically (e.g., fiscal year ended September 30, 2025) amounting to $2.5 million [F1]. This highlights the challenge of balancing heavy technology investments with revenue realization in a competitive market. The interplay between advancing product innovation and managing cash burn is thus crucial.

Bridgeline’s Business Model: AI-Driven Digital Revenue Enhancement

Bridgeline Digital generates revenue primarily through software licensing fees offered via multiple deployment models: cloud-based SaaS subscriptions hosted either by the company or third parties such as AWS; perpetual licenses installed on-premises at client sites; and managed hosting services that provide additional infrastructure management [S1, S12]. This mix creates diversified revenue streams but also complicates forecasting due to differing contract structures.

Revenue drivers include initial license sales often accompanied by complex implementation projects requiring significant integration effort and professional services support [S13]. Post-implementation, recurring subscription fees from renewals maintain revenue resilience but fluctuate based on customer satisfaction and competitive alternatives.

Strategically important is Bridgeline's suite of nine AI-powered Hawk AI products designed to increase online revenue through improving website traffic quality, conversion rates, and average order values by optimizing search relevance and personalization [S23]. Products such as Smart Search leverage cutting-edge large language models (LLMs) with retrieval-augmented generation (RAG), supported by complementary modules like Concept Search (NLP-based goal recognition), Visual Search (camera-based queries), and an array of Smart Agents assisting merchandising teams through agentic AI automation [S23].

This tailored approach allows customers considerable autonomy to fine-tune AI behavior per site segment or function—offering distinct configurability compared to one-size-fits-all marketplace offerings that lack merchandising controls (e.g., synonym tuning or trending product boosts). Services such as web design, SEO audits via WooRank integration, digital experience management platforms (OrchestraCMS), and franchise marketing software (TruPresence) supplement this core portfolio [S13], illustrating a broad addressable market beyond pure eCommerce into industrial distribution and associations.

Competitive Positioning: Tailored AI Suite vs. Modular Industry Peers

Bridgeline operates in a fragmented Martech sector marked by specialized vendors delivering either narrowly scoped tools or commoditized solutions lacking customization potential [S11]. Its competitive moat derives from platform depth—integrating multiple functions such as content management, commerce optimization, search personalization—packaged with customer-specific merchandising rules enhancing AI output precision.

Ease of use is emphasized across user interfaces designed to reduce dependence on highly technical staff within client organizations—a non-trivial barrier for many enterprise deployments that demand agility despite technical complexity beneath the surface [S11].

Moreover, Bridgeline’s dual delivery methods—SaaS versus dedicated hosting—afford deployment flexibility sought among both traditional enterprises preferring control over sensitive data environments and newer cloud-first adopters aiming for operational simplicity [S11]. Complementing software sales with development services further cushions customer adoption by minimizing reliance on third-party integrators.

Strategic partnerships spanning major commerce/content platforms such as Adobe Experience Manager and Shopify extend Bridgeline’s reach via embedded integrations enhancing channel distribution efficacy beyond direct sales efforts alone [S12]

This multi-dimensional differentiation contrasts sharply with competitors focused on singular capabilities like site search only (e.g., Algolia), SEO analytics (e.g., SEMrush), or personalization modules lacking endpoint manageability features—all while competing against customers who might build internal tools [S16]. The breadth of modules plus ability to customize foundational AI models aligns with emerging preferences for tailored digital consumer experiences enabled through generative AI technologies.

Industry Dynamics: Customer Adoption, Competitive Fragmentation, and Pricing Dynamics

Bridgeline addresses mid-market to large enterprise segments in verticals including health services, finance institutions like banks/credit unions, franchises with complex multi-location branding needs, eCommerce retailers competing on digital UX innovation as well as associations seeking membership engagement improvements [S12, S27]. This diversity serves as a partial hedge against sector-specific downturns but also complicates sales cycles due to divergent buying criteria.

Sales cycles exhibit two notable traits:

- Lengthiness driven by requisite cross-functional implementation planning across marketing operations,

- Fluctuations impact license revenue recognition quarter-to-quarter given project complexity which cannot easily be accelerated or compressed without affecting margins negatively.

Renewal rates—a critical recurring revenue lever—are vulnerable since customers possess full discretion not to renew subscriptions/licenses at term end [S1]. Factors contributing to potential churn include perceived stagnation in product innovation relative to competitors’ offerings; dissatisfaction with service levels; or shifting budgetary constraints where marketing spend reprioritization occurs under economic pressures

While no single client accounts for over 10% revenue currently—per recent disclosures—a handful contribute significantly enough that renewal failure could materially depress revenues short term [S16]. This customer concentration combined with low switching costs inherent in software-as-a-service platforms elevates pricing competitiveness within each vertical sufficiently high to pressure margins landscape-wide. Further complicating matters are the relatively low industry barriers permitting rapid entry of startups riding newer generative AI breakthroughs disrupting legacy Martech solutions

Growth Catalysts: AI Innovations, Product Expansion, and Strategic Partnerships

Key elements driving future growth rest squarely on advancing proprietary artificial intelligence capabilities against competitive benchmarks:

- Agentic AI empowers clients’ merchandising teams with autonomous machine learning agents that collaboratively optimize product displays and search ranking dynamically without constant manual intervention,

- Integration of generative AI components including smart response engines elevates interactive shopping experiences beyond static keyword matching frameworks,

- Leveraging both large language models (LLMs) alongside smaller foundation models enables flexible cost-performance tradeoffs accommodating different customer scale needs,

- Expansion into adjacent functional areas like SEO auditing using WooRank's platform aims at increasing wallet share within existing accounts by deepening value delivered around organic search optimization,

- Extension into franchise marketing management via TruPresence caters directly to complex parent/child site structures yielding cross-sell opportunities within established relationships.

Furthermore, alliances with cloud infrastructure providers such as Amazon Web Services ensure scalable managed hosting options underpinning SaaS delivery reliability—a critical prerequisite for enterprise adoption—and collaborations with ecosystem partners like Adobe or Shopify open expanded marketplace distribution channels beyond the direct sales force reach limitations typical for SMB-focused vendors [S12]

Risks and Constraints: Liquidity Challenges Renewal Rates And Market Competition

Despite promising technology stacks enriching Bridgeline's client value proposition, underlying structural risks cast shadows on medium-term stability:

- Chronic operating losses evidenced through fiscal 2025 net losses hovering around $2.5 million annually carry forward substantial accumulated deficit saddling balance sheet strength from roughly $94 million cumulative losses historically recorded [F1][S1], signaling persistent profitability hurdles.

- A current ratio well below unity at approximately 0.67 per latest quarter-end metrics signals tight working capital availability threatening operational flexibility absent external funding injections or materially improved cash flow conversion from license renewals predominating subscription revenues at risk if churn accelerates unexpectedly [F1][S2].

- Customer concentration effects intensify revenue volatility should several key clients choose contract non-renewal simultaneously given observed dependence patterns highlighted in risk disclosures where major account decisions drive disproportionate top-line swings [S27].

- Market fragmentation invites aggressive price competition particularly from larger well-capitalized peers able to deploy cutting-edge generative AI features quickly forcing continuous investment just to stay parity potentially compressing margins amid scale disadvantages faced relative to dominant players described broadly among peers such as Bloomreach or Coveo [S16].

- Reliance on third-party cloud providers (notably AWS) for SaaS/managed hosting adds operational entrainment risk should service terms deteriorate or interruptions occur prioritizing swift migration capability which remains non-trivial operationally due to bespoke platform complexity documented internally [S22].

Collectively these constraints impose a watchful stance around financial sustainability coupled with disciplined execution needed around expanding renewal retention programs highlighted across customer success initiatives designed specifically for churn mitigation plus continuous R&D budgeting maintaining feature relevancy in fast-evolving market conditions.

Key Milestones and Upcoming Developments to Monitor

To gauge trajectory clarity over coming quarters stakeholders should track:

- Quarterly filings reporting renewal rates explicitly indicating whether key contracts renew on favorable terms impacting backlog predictability,

- Announcements concerning incremental strategic partnerships or deeper integrations pushing adoption within partner ecosystems,

- Product launch timelines aligned with planned rollouts of advanced generative/agentic AI features promising roadmap fulfillment credibility,

- Potential capital raising activities or debt refinancing events mitigating working capital pressures highlighted absent so far but implicit given reported liquidity ratios,

- Indicators from customer success metrics shooting early signals about net retention improvement or deterioration capturing practical effectiveness of retention programs described in corporate disclosures.

Such markers will elucidate execution competency addressing intertwined innovation-led growth ambitions balanced against near-term financial stewardship demands outlining sustainable scaling pathways ahead.

Financial Snapshot: Liquidity Status Profitability Challenges And Capital Needs

At the close of Q1 FY26 Bridgeline Digital held cash & equivalents totaling $1.37 million juxtaposed against current liabilities amounting roughly $5.21 million leaving a suboptimal current ratio near 0.67 indicative of working capital strain limiting operational headroom[F1][S2]. Historical fiscal year net loss figures approximated $2.5 million reinforce ongoing profitability challenges constraining equity buildup from prior cumulative deficit approximating $94 million documented through FY25 year-end[F1][S1].

No subsequent financing actions have been revealed post-latest quarter filings implying reliance on existing liquid resources plus improvement through operational efficiencies or elevated recurring revenues derived mainly from license renewals[S2][F1]. Should renewal attrition accelerate amidst competitive pressures or capex-intensive R&D ramp-ups further burden fixed cost allocations bridging the cash flow gap could become increasingly difficult absent equity/debt infusions necessitating close credit line covenant monitoring although no material covenant waivers have been disclosed yet[S2].

This fragile liquidity backdrop accentuates the importance of tightly managed cost controls alongside successful top-line expansion driven primarily through sustained subscription renewals representing critical earning visibility components inherent in subscription SaaS economics documented across disclosure kits [S1][S23]

Disclaimer: This analysis is based solely on available public SEC filings up to May 2026 and does not constitute investment advice nor an endorsement of any outcomes related to Bridgeline Digital Inc.

Financial position in context

As of 2026-03-31, companyfacts shows $1373000 in cash and equivalents [F1]. Current assets of $3mm and current liabilities of $5mm imply a current ratio near 0.67x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments