Broadstone Net Lease’s 2025 Revenue Growth and Dividend Resilience Under Rate Pressure

Broadstone Net Lease posted solid revenue growth in 2025 but faced net income contraction amid rising capital expenditures and maintained dividend payments exceeding a 6% yield.

Broadstone Net Lease, Inc. (BNL) reported 5.2% revenue growth to $454.1 million in fiscal 2025, continuing its trajectory supported by its triple-net lease portfolio that provides stable cash flows. However, net income declined sharply by 40.6% to $96.5 million due to significantly higher capital expenditures which weighed on profitability despite an 8.4% increase in operating cash flow. The company sustained dividend payouts above $200 million, supporting a dividend yield surpassing 6%, though absence of share buybacks signals a capital allocation shift influenced by market conditions. Liquidity with $30 million in cash and careful debt management alongside tenant credit risk remain key factors as BNL balances income stability with growth investment under current real estate cyclicality and tightening interest rates.

2025 Financial Performance: Revenue Gains vs. Net Income Contraction

Broadstone Net Lease reported fiscal year 2025 revenues of $454.1 million, marking a solid 5.2% increase over the prior year’s $431.8 million [F1]. This revenue growth underscores the effectiveness of Broadstone's portfolio strategy built around triple-net lease agreements that generally provide steady rental income streams insulated from most property-related operating costs.

However, net income declined significantly during the same period, falling by 40.6% year-over-year from $162.4 million in 2024 down to $96.5 million in 2025 [F1]. This contraction is mainly attributable to a sharp increase in capital expenditures — which rose by 76.9%, reaching nearly $29.7 million — reflecting investments likely related to property acquisitions or renovations aimed at maintaining or enhancing portfolio value [F1]. Despite this impact on profitability, operating cash flow (CFO) improved by 8.4% to approximately $299.5 million, signaling stable underlying cash generation supported by triple-net lease structures transferring many expenses to tenants [F1][N2].

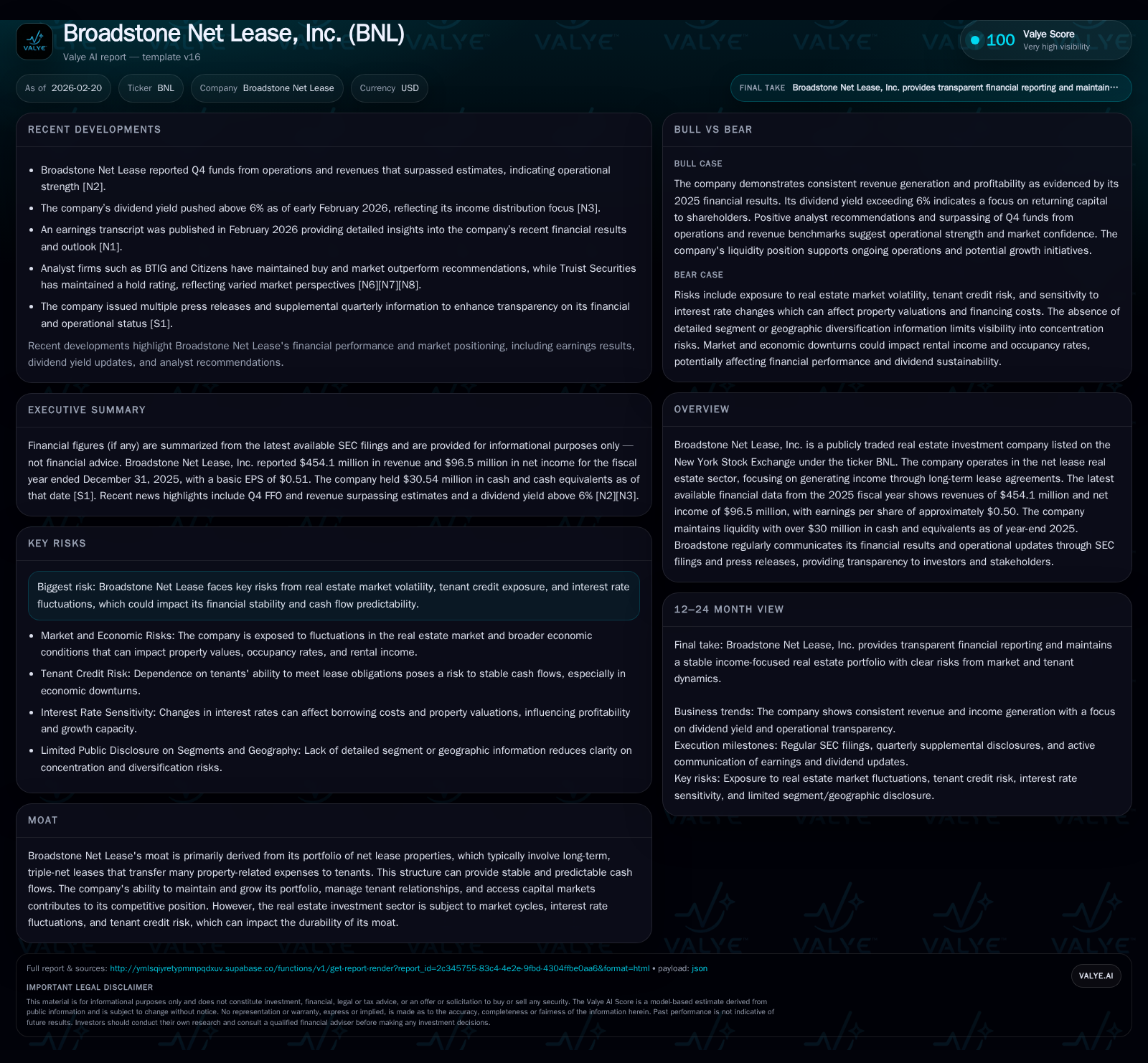

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 454 | 96 | 299 | 30 | +5.2% | -40.6% |

| 2024 | 432 | 162 | 276 | 17 | -2.5% | +4.5% |

| 2023 | 443 | 155 | 271 | 46 | +8.7% | +27.3% |

| 2022 | 408 | 122 | 256 | 31 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 219 | 270 | 3.3 |

| 2024 | 217 | 259 | 5.4 |

| 2023 | 208 | 225 | 5.1 |

| 2022 | 181 | 225 | 3.9 |

Source: SEC companyfacts cache [F1].

Note: Operating income data is not available for recent years in provided tags.

Triple-Net Lease Model: Stable Cash Flows Amid Tenant Credit Risks

Broadstone’s competitive advantage stems from its triple-net lease model where tenants bear responsibility for property taxes, insurance, and maintenance costs alongside rent payments [S1][S4]. This structure provides predictable rent streams insulating Broadstone from many operating cost fluctuations.

However, this model exposes the company to tenant credit risk—financial distress or default by tenants could disrupt income flows [S6][S7]. With macroeconomic pressures such as rising interest rates and inflation affecting various sectors, tenant credit quality remains a key risk highlighted in recent disclosures and investor commentary [N3]. Additionally, cyclical real estate market downturns may affect asset values and leasing activity upon expiration.

Investor confidence is reflected in Broadstone’s dividend yield exceeding six percent despite these risks [N3], underscoring the market’s view of stable income balanced against credit exposure.

Capital Allocation: Dividends Sustained While Buybacks Absent Amid Rising Capex

The company maintained strong shareholder returns with approximately $218.8 million paid in dividends during fiscal year 2025 compared to about $216.8 million in the prior year—despite lower net income—demonstrating commitment to dividend continuity [F1][N3]. This supports a dividend yield above six percent.

In contrast, no common stock repurchases have been recorded since before fiscal year 2020; historical buybacks last occurred around FY2019 at roughly $34.6 million annually [F1]. The absence of buybacks signals a strategic shift toward preserving capital for dividends and funding elevated capital expenditure needs.

Capital spending surged by nearly three-quarters year-over-year, likely driven by build-to-suit projects or facility upgrades intended to sustain asset quality and attract creditworthy tenants [F1][S19]. This aligns with broader REIT trends where maintaining portfolio competitiveness requires increased reinvestment even amid interest rate pressures.

Liquidity and Debt Management: Preparing for Interest Rate Environment Challenges

Liquidity remains solid with about $30.5 million in cash and equivalents as of December 31, 2025 [F1], providing cushion for near-term obligations including dividends and capital investments.

The company has actively managed its debt profile through refinancing activities documented across multiple recent Form 8-K filings spanning late 2025 into early 2026 [S8][S9][S11][S16]. These efforts appear focused on mitigating exposure to rising interest rates while maintaining access to capital markets for ongoing financing needs.

While explicit debt ratios are not disclosed within provided tags, typical REIT leverage targets suggest Broadstone aims for balanced leverage consistent with industry norms.

Such financial discipline is important given potential volatility from tenant credit risk or tightening capital markets.

Outlook and Milestones: Operational Execution Evident but Future Growth Dependent on Pipeline Progress

Recent quarterly earnings reports surpassed consensus estimates on revenues and funds from operations (FFO), underscoring execution strength heading into fiscal year-end [N2][N1]. These results support confidence in the quality of Broadstone’s revenue base despite margin pressures.

Key milestones include progress on build-to-suit development projects previously disclosed [S19], lease renewal activity timing, new tenant acquisitions within the triple-net framework, and ongoing monitoring of tenant financial health—all critical indicators for sustaining future FFO and dividends.

Explicit forward-looking guidance or detailed milestone timelines are not available from provided sources; thus, investors should monitor subsequent quarterly disclosures closely.

Investor Implications: Yield Appeal Balanced Against Profitability Headwinds and Credit Risk Exposure

Broadstone offers investors attractive yield potential via its stable rental income derived from triple-net leases; however, net income volatility driven by rising capex requirements tempers near-term profitability.

The approximate return on equity of about 3.3% reflects moderate efficiency converting equity into earnings given consistent dividend payouts [F1]. Free cash flow after capex remains positive near $270 million annually supporting distribution capacity [F1].

Investors should continue assessing funds from operations coverage metrics, tenant credit trends reported going forward, and shifts in capital expenditure priorities that may influence future yield sustainability.

In summary, Broadstone navigates a balance between maintaining its traditional net lease model stability against external challenges posed by interest rate increases and commercial real estate cycles through measured reinvestment strategies aimed at preserving long-term asset quality.

This report synthesizes information solely from public SEC filings and news disclosures available as of February 20, 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments