POPULAR, Inc.’s Return to Profit Leadership: Growth Trends and Strategic Positioning in 2025

POPULAR, Inc. leveraged geographic concentration and diversified loan strategies to achieve notable profit growth amid local economic challenges in 2025.

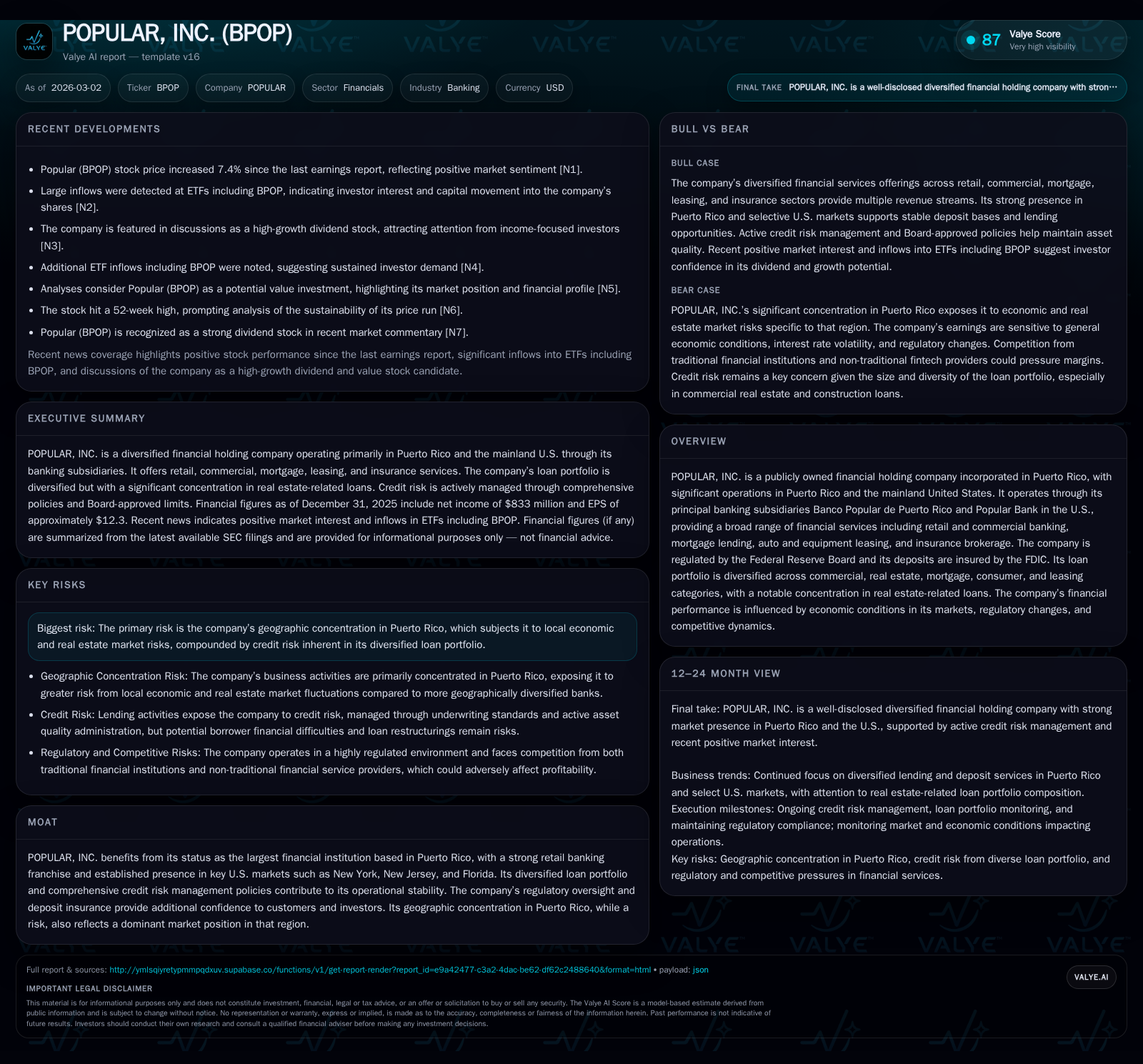

POPULAR, Inc., the largest financial institution headquartered in Puerto Rico, posted a 35.6% increase in net income for 2025 driven by stabilization in its core Puerto Rican market and growth in mainland U.S. operations. Its loan portfolio remains heavily weighted toward real estate but with increasing diversification across commercial and consumer sectors. Strong operating cash flow growth and disciplined capital allocation underpin its improved return on equity of approximately 13.3%. Regulatory scrutiny and credit risks tied to Puerto Rico’s economic environment present ongoing challenges requiring vigilant risk management and strategic expansion into U.S. metropolitan markets.

A Storied Growth Track Record Amid Regional Complexities

POPULAR, Inc., anchored in Puerto Rico with significant U.S. operations, delivered robust earnings momentum in fiscal year 2025. The company posted net income of $833 million, marking a remarkable 35.6% increase from $614 million reported in 2024 [F1]. This upswing belies mixed revenue signals arising from economic volatility concentrated chiefly in its dominant Puerto Rican market, which accounted for approximately 80% of total revenues in 2025 [S1]. The protracted economic headwinds on the island have historically pressured results through higher delinquencies and charge-offs; however, gradual recovery phases alongside federal stimulus inflows have created pockets of stability propelling profit growth.

Despite this top-line variability, POPULAR’s standing as the largest Puerto Rico-based financial institution enabled it to capitalize on both retail loyalty and commercial banking expansion domestically and on the U.S. mainland [S1],[S2]. Detailed segment disclosure highlights intense dependency on regional dynamics but also illustrates broadening revenue streams from rising loan origination activity within highly competitive metropolitan areas such as New York City and Miami [S9],[S15].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 833 | 878 | 197 | +35.6% |

| 2024 | 614 | 675 | 213 | +13.5% |

| 2023 | 541 | 687 | 208 | -50.9% |

| 2022 | 1103 | 1015 | 104 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 198 | 681 | 13.3 |

| 2024 | 180 | 461 | 10.9 |

| 2023 | 160 | 479 | 10.5 |

| 2022 | 162 | 911 | 26.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures unavailable; net income reflects fiscal year-end values.

Loan Portfolio Diversification: Balancing Real Estate Concentrations and Commercial Credit

The company’s loan portfolio composition underscores a critical balancing act between concentration risk and diversification efforts. At year-end 2025, real estate-related loans constituted roughly half (52%) of loans outstanding — encompassing residential mortgages, construction loans focused on multifamily and condominium projects, as well as commercial real estate lending secured by owner-occupied and non-owner-occupied properties [S8],[S10]. Concurrently, POPULAR has expanded commercial multi-family exposures notably within its mainland U.S. banking units.

Commercial and industrial loans form the next prominence slice at about 22%, complemented by leasing services predominantly auto-related loans at approximately 10% exposure, reflecting activities through automotive dealerships [S10]. Consumer lines such as personal loans and credit cards add further diversification though remain smaller within the total mix.

This multifaceted lending profile is overseen via proactive credit risk management policies enforced by internal limits aligned with regulatory guidance [S22]. The bank employs rigorous underwriting standards calibrated against risk appetite thresholds to maintain allowance adequacy for credit losses amid economically sensitive segments like commercial real estate construction — sectors vulnerable to cyclical downturns or sector-specific shocks.

Economic Landscape Impacting Performance: Puerto Rico’s Recovery and Mainland Market Dynamics

Puerto Rico’s economic backdrop continues to dictate much of POPULAR’s operational fortunes. The island’s prolonged recession since the late-2000s compounded by a fiscal crisis culminating in government bankruptcy protection filing in 2017 cast long shadows over borrower creditworthiness [S1],[S13]. Though incremental progress is evident post-government restructuring with the exit from bankruptcy in 2022, substantial fiscal constraints prevail alongside local unemployment concerns.

Federal stimulus funds related to disaster relief have buoyed activity surges but reliance on such support renders sustainability uncertain amid political shifts or reductions in aid allocations [S1]. Meanwhile, mainland market demands in New York/New Jersey/Florida carry different economic sensitivities including greater competition intensity but offer avenues for organic loan growth that partially offset Puerto Rico-specific headwinds [N1],[S6].

Interest rate volatility shaped net interest margins as rising rates increased funding costs yet simultaneously enhanced yields on new lending—though tight pricing environments pressured deposit costs amid competitive rivalry within key metro geographies [S6],[N4].

Capital Allocation Priorities: Robust ROE and Cash Flow Evolution

In an asset-heavy sector where capital efficiency governs competitiveness, POPULAR exhibited improves returns reinforced by prudent capital management. Return on equity approximated a solid 13.3% for fiscal year-end December 2025 calculated from reported net income and stockholders’ equity tallied at approximately $6.25 billion [F1].

Operating cash flow escalated notably by over thirty percent year-over-year to nearly $878 million while capital expenditures moderated slightly after prior period increases — underpinning free cash flow availability exceeding $680 million [F1]. This cash flow prioritization fuels strategic flexibility for organic investments or shareholder returns.

Leverage indicators reflect regulatory compliant capital buffers consistent with Federal Reserve oversight ensuring resilience under stress scenarios [S5],[S17]. Dividend sustainability coincides with strong earnings coverage supporting incremental distributions.

Dividend Yield and Share Repurchases: Shareholder Value Enhancements

A progressive dividend strategy marks POPULAR’s commitment to shareholder remuneration post-recovery phase with payout increases totaling approximately one-third over the past three years [F1],[N3]. In parallel, buyback programs accelerated considerably during calendar year 2024 signaling confidence in underlying cash generation capacity and capital surplus deployment aims [F1],[N8].

Analysis of payout ratios affirms that dividend payments remain comfortably covered by earnings without jeopardizing reinvestment plans or regulatory capital thresholds — key parameters valued by income-focused investors drawn to growing yield profiles balanced with prudent capital stewardship.

Regulatory Compliance Challenges and Their Financial Implications

Heightened regulatory scrutiny has emerged as a material consideration for POPULAR — particularly given historical inquiries into consumer lending practices including add-ons on products and mortgage appraisal protocols within its primary Puerto Rican operations [S4]. Self-identified compliance issues related to sanctions programs amplify operational risk dimensions with attendant reputational implications.

The cost burden linked with ongoing monitoring systems upgrades, process enhancements, and legal settlements translates into tangible expense line pressures while enforcement outcomes carry potential constraints on product offerings or business activities [S4],[S16],[S29]. Navigating these terrains involves elevated governance diligence coupled with adaptive risk frameworks designed to preempt future noncompliance episodes.

Strategic Outlook: Market Expansion and Risk Mitigation Paths Ahead

Looking forward, POPULAR’s strategic thrust blends deepening core market penetration within Puerto Rico alongside measured expansion across affluent U.S. corridors encompassing New York City metropolitan areas, Northern New Jersey suburbs, and select Florida markets known for demographic growth trajectories [N1],[S6]. This dual-market approach leverages entrenched brand equity locally while hedging concentration risks inherent to its home territory.

Operational initiatives focus on enhancing digital banking capabilities to meet evolving customer preferences against rising fintech competition alongside cross-selling bundled financial products via specialized subsidiaries enhancing fee income diversity [S7]. The company must also sustain credit quality vigilance amidst loan origination growth ambitions given sector cyclicality.

What Investors Should Monitor in Upcoming Quarters

Several key performance indicators warrant close observation:

- Trends in charge-offs or delinquency rates especially within residential mortgage and construction segments that historically react acutely to economic shifts.

- Regulatory engagement developments including any new enforcement actions or mandated compliance investments impacting operating costs.

- Deposit inflow stability reflecting customer confidence levels amid competitive pricing pressures.

- Dividend announcements combined with buyback activity signaling management’s assessment of capital adequacy vs shareholder return priorities. Market sentiment indicators suggest positive momentum post recent earnings release supported by ETF inflows; maintaining this trajectory requires continued execution against outlined risks [N1],[N2],[N4].

This report synthesizes publicly available financial disclosures and market intelligence up to March 2, 2026 regarding POPULAR, Inc., providing analysis grounded strictly on documented evidence without speculative extrapolation or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments