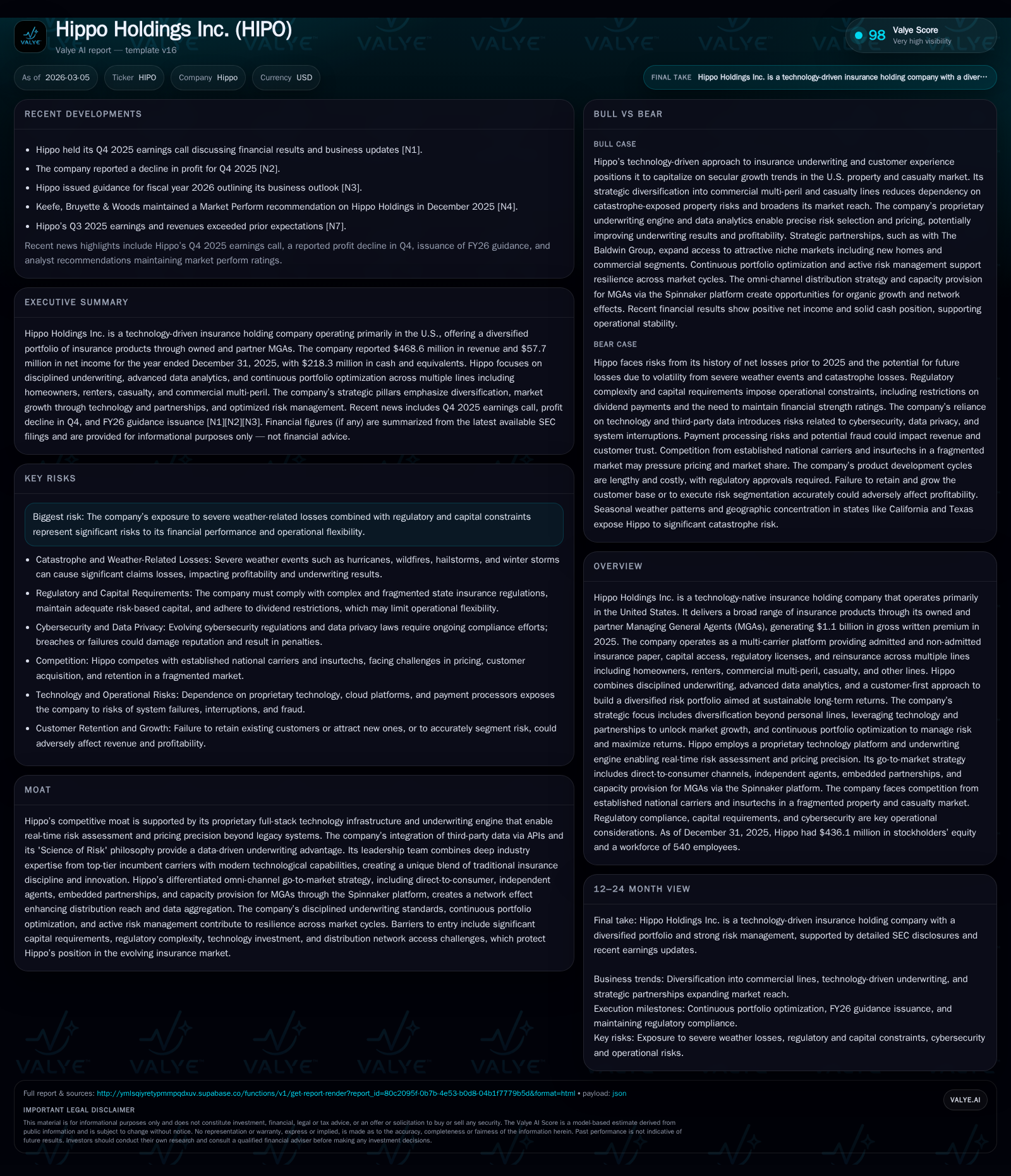

Hippo Holdings Inc. Drives Growth Through Proprietary Tech and Portfolio Diversification

The company’s profitable turnaround in 2025 is anchored in advanced underwriting technology, multi-carrier platform expansion, and strategic portfolio management amid ongoing regulatory and catastrophe risks.

Hippo Holdings transformed from multi-year net losses into profitability in 2025 by scaling its premium base to $468.6 million while improving underwriting precision through proprietary technology. Its multi-carrier platform, including owned and partner MGAs supported by the Spinnaker capacity initiative, diversified product offerings beyond homeowners insurance. However, risks remain from severe weather volatility and a fragmented regulatory landscape that constrain growth and capital deployment. Future progress depends on navigating these headwinds while leveraging technology and expanding market reach.

From Losses to Profits: Tracking Hippo’s Historical Growth Trajectory

Hippo Holdings’ journey from substantial net losses to profitability by the close of fiscal year 2025 marks a significant operational transition. Revenue surged over threefold from $119.7 million in 2022 to $468.6 million in 2025, representing approximately a 259% increase over this period [F1]. This growth was partly suppressed historically due to a conservative underwriting pause on HO3 homeowners policies instituted after severe weather events caused notable catastrophe losses in Q2 2023 [S1]. Such pauses reduced immediate premium inflows but stabilized loss ratios over time.

Net income transitioned from a steep negative of -$333.4 million in 2022 to a positive $57.7 million in 2025 [F1]. Early-stage losses also reflected the timing mismatch inherent in insurance marketing expenses—incurred upfront while premiums are recognized ratably over 12-month policy terms—and increased fixed costs as the company expanded its employee base and complied with public company standards [S1]. The underlying improvement was driven by disciplined risk selection and portfolio optimization that improved underwriting margins along with scaling top-line premiums.

Operating cash flows demonstrated volatility consistent with premium growth cadence but turned positive at $9.2 million in 2025 after negative outflows exceeding $161 million in 2022 [F1], indicating advancing operational cash generation.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 469 | 58 | 9 | 0 | +25.9% | +242.5% |

| 2024 | 372 | -40 | 48 | 0 | +77.4% | +85.2% |

| 2023 | 210 | -273 | -92 | 30 | +75.2% | +18.1% |

| 2022 | 120 | -333 | -161 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 15 | 9 | 13.2 |

| 2024 | 16 | 47 | -11.2 |

| 2023 | 2 | -122 | -72.3 |

| 2022 | -166 | -56.5 |

Source: SEC companyfacts cache [F1].

Note: Year-over-year percentages calculated using reported numbers [F1].

Technology-Led Underwriting: The Engine Behind Hippo's Competitive Edge

At the core of Hippo’s competitive position lies its proprietary full-stack technology infrastructure enabling sophisticated automated underwriting decisions powered by advanced data analytics [S4][S6]. Unlike many incumbent insurers relying on siloed legacy platforms, Hippo integrates multiple third-party data sources via customized APIs supporting its 'Science of Risk' philosophy — combining actuarial rigor with real-time risk assessment.

This system facilitates precision pricing across both admitted (regulated) and non-admitted (E&S) insurance paper lines—critical for navigating complex state regulations where coverage flexibility varies [S12]. It also enables active modulation of risk exposure by dynamically adjusting retention thresholds based on catastrophe modeling simulations.

By embedding AI systems under governance aligned with evolving regulatory guidance such as NAIC’s Model AI Bulletin, Hippo balances compliance with machine learning benefits for rating accuracy without sacrificing fairness or transparency [S21][S22]. This supports proactive loss prevention initiatives beyond reactive claims settlement—a key shift fostering long-term policyholder engagement.

Platform Strategy and Market Reach: Diversifying Lines and Partnership Levers

Hippo operates a multi-carrier platform comprising both owned Managing General Agents (MGAs) and partner MGAs alongside its Spinnaker platform which provides capacity provisions—functioning as insurer-of-record for third-party programs [S12][S26]. This structure supports portfolio diversification across homeowners, renters, commercial multi-peril (CMP), casualty, and specialty lines enabling balanced risk retention.

An omni-channel distribution approach complements the model: direct-to-consumer sales integrate with independent agents and embedded partnerships woven into real estate workflows [S4]. A strategic alliance with The Baldwin Group notably triples Hippo's footprint in the New Homes market segment—a high-growth niche tied to home construction cycles [N2][S6].

This layered go-to-market strategy enhances customer acquisition efficiency while creating network effects where aggregated data streams refine underwriting algorithms—strengthening their moat against competitors challenged by entrenched agent networks [S15][S27].

Navigating Regulatory Complexity and Catastrophe Risks

Hippo faces extensive regulation across U.S states governing premium rates, underwriting practices, licensing, data privacy, and new AI-related compliance frameworks impacting its underwriting models [S9][S10][S16][S20]. Regulatory scrutiny intensifies around data use given evolving privacy laws such as CCPA/CPRA alongside NAIC guidance on AI system governance [S16][S21][S22].

Severe weather remains a principal risk driver; past Q2-2023 catastrophe losses prompted a nationwide HO3 new business pause illustrating sensitivity to natural disaster spikes [S1][S4]. Hippo mitigates this via layered reinsurance treaties complemented by catastrophe bond placements adjusting retention within defined risk appetite parameters ensuring resilience across cycles [S7][S8][S10].

Portfolio diversification into renters and commercial lines smooths geographic concentration exposure previously focused on homeowners risks; continuous stress testing against modeled hurricane or wildfire scenarios informs capital adequacy assessments regularly [S16][S17].

Capital Allocation Discipline: Returns, Buybacks, and Cash Flow Trends

Hippo’s balance sheet strengthened with shareholders’ equity at approximately $436 million as of FY-end 2025 after prior declines reflecting historic losses but now stabilizing alongside profitability gains [F1]. The company repurchased about $14.5 million worth of shares in FY25—a modest reduction from prior years—signaling prudent capital deployment amidst improving fundamentals [F1].

Operating cash flow improvements lifted it into positive territory at $9.2 million following large negative swings due to upfront claim settlements relative to premium collections during earlier growth phases [F1]. Low capital expenditure levels ($0.1 million in FY25) indicate a lean reinvestment profile focused primarily on software development rather than physical assets.

Approximate return on equity based on latest annual net income stands near 13%, demonstrating emerging effectiveness translating earned premiums into shareholder value after several years of structural losses [F1]. Ongoing reinvestment decisions will balance sustaining technology advantages versus opportunistic buybacks or dividends—which have not been disclosed currently.

Key Milestones to Watch Going Forward

Critical upcoming indicators include renewal rates following the HO3 new business pause which will reveal customer retention dynamics post-underwriting constraints [N2][N3]. Reinsurance treaty renewals later this year will affect available capacity pricing influencing cost of capital deployment.

New product launches extending beyond core personal lines into adjacent home-related insurtech or niche commercial sub-segments will test execution capabilities outside existing strongholds.

Regulatory developments around AI usage require close monitoring as new compliance frameworks could impact model deployments or pricing sophistication.

Geographic expansion plans hinge on effective navigation of fragmented state licensing regimes without diluting the underwriting discipline established thus far.

This analysis integrates public financial statements and disclosures without prescribing investment action or forecasts beyond documented guidance evidence. It highlights operational drivers shaping Hippo Holdings Inc.’s recent profitability turnaround alongside recognized risks inherent across the P&C insurance ecosystem it competes within.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments