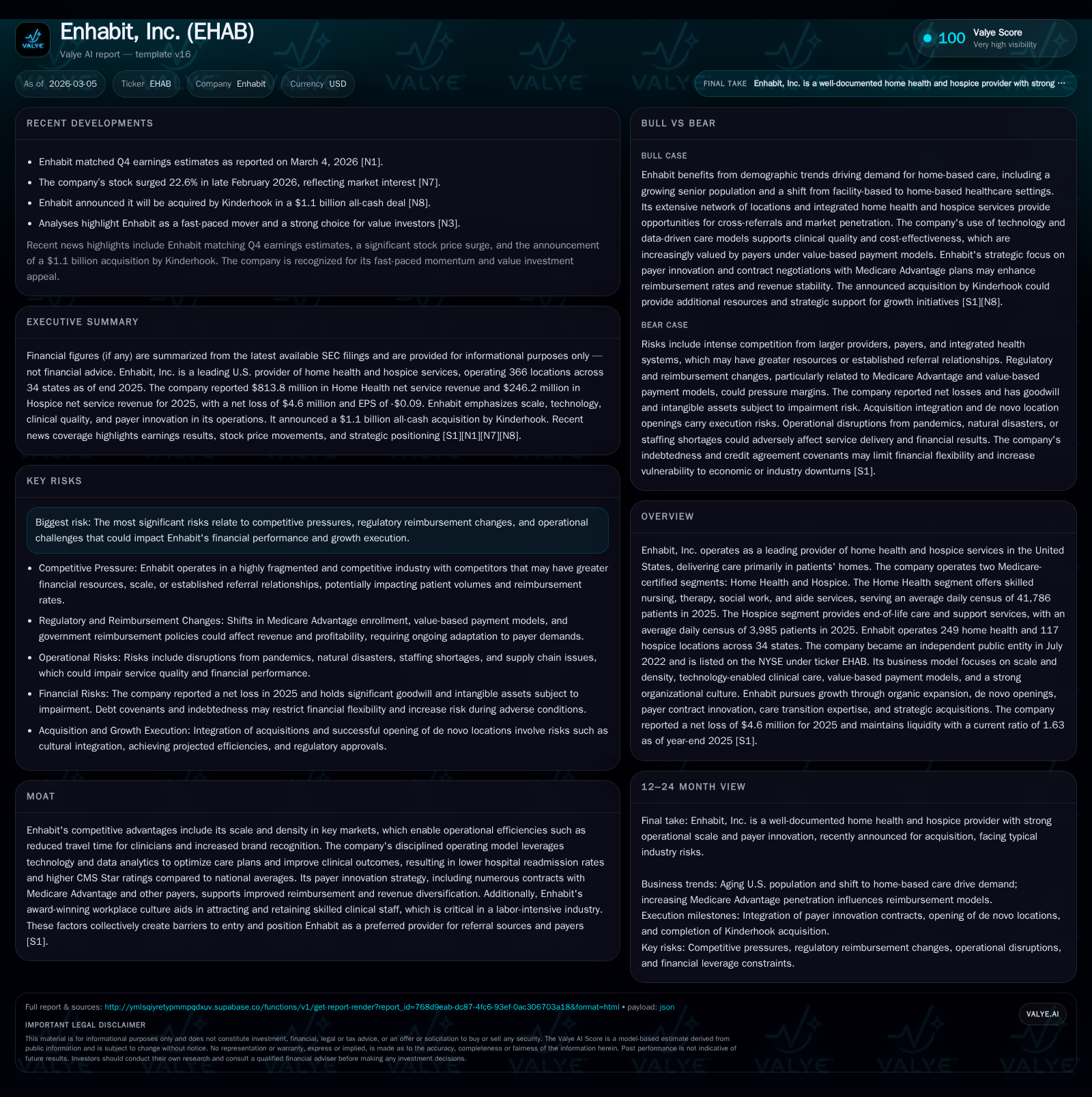

Enhabit’s Financial Turnaround Highlights Value Amid Pending $1.1 Billion Acquisition

Enhabit, Inc. demonstrates marked operational recovery and solid cash flow generation despite continued net losses as it awaits completion of its Kinderhook acquisition.

Enhabit, a prominent home health and hospice services provider, has rebounded from sizable losses in prior years to report positive operating income and strong cash flows in 2025, reflecting effective operational adjustments and strategic growth. The company’s growth is supported by scale, technology-enabled care, payer diversification, and a disciplined operating model. However, regulatory risks, intense competition, and the uncertainties surrounding the pending $1.1 billion all-cash acquisition by private equity firm Kinderhook present notable challenges ahead. Capital structure enhancements with new credit facilities position Enhabit to pursue selective acquisitions in 2026, while maintaining financial flexibility.

Company Overview and Business Model

Enhabit, Inc. is a leading provider of home health and hospice services across the United States. With origins dating back over 25 years and headquartered in Dallas, Texas, Enhabit transitioned to an independent public company in July 2022 after separating from Encompass Health Corporation. As of December 31, 2025, Enhabit operated an extensive network comprising 249 home health agencies and 117 hospice locations spanning 34 states [S1], [S11].

The company’s operations are organized into two Medicare-certified segments:

- Home Health: Skilled nursing, therapy (physical, occupational, speech), medical social work, and aide services delivered primarily post-acute or for chronic condition management within patients’ homes.

- Hospice: End-of-life care offering pain management, palliative counseling, spiritual support, and bereavement services.

In total, these segments served an average daily census of approximately 41,786 patients in home health and 3,985 patients in hospice during 2025 [S1], generating net service revenues tallying approximately $813.8 million (76.8%) from Home Health and $246.2 million (23.2%) from Hospice [S1], [S11]. This portfolio reflects the company's targeted focus on high-growth demographics requiring cost-effective care solutions outside traditional facility settings.

Historical Performance Trends

Enhabit's financial trajectory until recently was marked by substantial net losses despite stable or growing topline volumes. According to SEC filings from FY2022 through FY2024, the company suffered persistent net deficits (e.g., -$40.4 million in FY2022; -$156.2 million in FY2024) during negative operating income that peaked at -$115.1 million in FY2024 [F1]. However, these losses narrowed sharply in fiscal year 2025 with operating income turning positive at $16.1 million—an impressive turnaround representing a year-over-year improvement exceeding 114%. Net loss also shrank dramatically to -$4.6 million while operating cash flow expanded robustly to $70.7 million (+38% YoY) [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -5 | 71 | 16 | 5 | +97.1% |

| 2024 | -156 | 51 | -115 | 4 | -94.0% |

| 2023 | -80 | 48 | -48 | -99.3% | |

| 2022 | -40 | 80 | -11 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 66 | -0.9 |

| 2024 | 47 | -29.8 |

| 2023 | -12.0 | |

| 2022 | 73 | -5.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue explicitly for FY2025 is detailed only as net service revenue split between segments totaling approximately $1 billion; prior years' revenue data are unavailable.

This financial improvement reflects operational efficiency gains enabled by scale and density advantages—including reduced clinician travel times—and disciplined integration of technology-driven care pathways that enhance outcomes while managing costs [S1]. The timing aligns with strategic shifts toward value-based payment models leveraging expanded contracts with Medicare Advantage plans [S25].

Growth Drivers and Operational Strengths

Scale & Density

Enhabit’s competitive moat fundamentally relies on its geographic footprint concentration in key markets permitting operational efficiencies that are difficult for smaller competitors to replicate [S1], [S25]. Concentration reduces travel time for clinicians allowing greater patient capacity per clinician-hour.

Technology & Clinical Excellence

Utilization of data analytics enables optimized personalized care plans improving clinical outcomes such as reduced hospital readmissions—a critical quality metric influencing CMS Star ratings—and supporting payer willingness to contract under value-based arrangements [S1].

Payer Innovation & Contracting

The company has cultivated a diversified reimbursement profile including numerous contracts with Medicare Advantage plans alongside traditional Medicare fee-for-service business mitigating reimbursement risk concentration [S1], [S25]. Value-based purchasing programs incentivize quality outcomes aligning with Enhabit’s operational model.

Workforce & Culture

An award-winning workplace culture not only supports retention amid industry-wide labor shortages but also underpins clinical quality—an essential determinant of patient satisfaction and referral source confidence [S1].

Challenges & Risk Profile

Regulatory & Compliance Risks

Healthcare regulation complexity exposes Enhabit to ongoing risks from government audits and investigations under CMS guidelines affecting Medicare/Medicaid reimbursement claims [S7], [S16], including risks associated with False Claims Act liabilities due to coding or billing errors [S4], [S19].

Legislative changes such as those introduced by recent healthcare reform laws impose increased scrutiny on providers’ compliance with anti-kickback statutes and physician referral laws (“Stark Law”), heightening legal risk exposure [S12], [S13]. Furthermore, policy shifts regarding Medicaid eligibility could impact revenue though Medicaid comprises less than one percent of their revenue mix currently [S14].

Competitive Landscape

The home health/hospice sector is fragmented but increasingly consolidating with large national providers attaining scale advantages [S14]. Enhabit competes against both publicly traded peers integrated with payers and private operators but holds distinction as the largest standalone publicly traded entity focused exclusively on home-based post-acute care presently [S14]. Maintaining this position requires continued investment in clinical quality measures and technology.

Acquisition Uncertainty & Transaction Effects

On February 22, 2026, Enhabit entered into an agreement to be acquired by Kinderhook Industries for approximately $1.1 billion in an all-cash transaction subject to customary closing conditions including regulatory approvals and shareholder consent [N1], [S18]. Completion timing remains uncertain; failure or delay poses potential disruptions including management distraction from operations, employee retention risks during transition periods, deferments by customers/payers on business decisions involving Enhabit’s services as well as transaction-related costs borne regardless of outcome [S18], [S22].

Capital Structure & Liquidity Positioning

Recent refinancing activity included an amended Credit Agreement dated February 26, 2026 featuring a Term Loan A facility ($315 million) amortizing quarterly over five years alongside a revolving credit facility ($160 million) maturing concurrently—all secured by first-lien liens on material assets—demonstrating enhanced liquidity readiness for growth investments or transaction support needs [S21], [S6]. Interest margins correlate with leverage ratios embedding some flexibility subject to covenants.

Cash & equivalents stood at approximately $43.6 million at year-end 2025 against current liabilities around $126 million yielding a current ratio near 1.63x reflecting prudent working capital management although net debt levels remain significant given sizeable credit facilities drawn partially due to acquisitions historically [F1], [S9].

Capital Deployment & Strategic Outlook for Growth

Management has articulated plans for deploying between $25–50 million toward targeted acquisitions during calendar year 2026 aimed at accelerating top-line expansion particularly where synergies can improve profit margins through integration — primarily focusing on home health given its dominance within their revenues—but opportunities also exist within hospice additions consistent with demographic tailwinds favoring aging populations requiring palliative care services [S26].

Organic volume growth prospects hinge on sustained success integrating new sites effectively while navigating evolving payment models designed increasingly around value rather than volume alone requiring nimble adjustment capabilities amid policy shifts such as CMS’s discontinuation of some bundled payment initiatives like BPCI Advanced effective end-2025 combined with rollout of mandatory payment models like TEAM covering post-operative episode accountability starting January 2026 which could alter referral patterns or reimbursement calculations unexpectedly [S15], [S17]. Monitoring reimbursement trajectories post-policy changes will be crucial.

What To Watch Going Forward (Analysis)

- Completion status and timing of Kinderhook acquisition including related regulatory reviews and shareholder vote outcomes.

- Integration progress of past acquisitions plus any announced accretive deals aligning with stated capital deployment intentions.

- Impact of new mandatory payment models (e.g., TEAM) on referral volume patterns especially from acute care hospitals.

- Developments around CMS audit programs or enforcement actions affecting revenue certainty or compliance costs.

- Metrics reflecting patient outcomes such as hospital readmission rates tied closely to reimbursement under VBP arrangements.

- Changes in workforce dynamics possibly influenced by pending merger uncertainty or competitive labor market pressures.

- Evolution of payer mix particularly enrollment trends within Medicare Advantage versus traditional FFS segments impacting margins.

Conclusion: Balancing Positive Operational Momentum Against Transactional Uncertainty and Regulatory Complexity

Enhabit’s operational turnaround culminating in positive EBITDA-level results coupled with strong cash flows marks meaningful progress relative to prior years’ heavy losses evidencing effective strategy execution centered around leveraging scale/density advantages supported by clinical excellence and technological enablement tailored for an evolving value-based care market milieu. Nonetheless, challenges persist primarily revolving around regulatory scrutiny inherent to healthcare reimbursement environments plus sizable outstanding debt obligations necessitating vigilant capital management complemented by growth-focused yet disciplined M&A efforts poised for accelerated deployment now that acquisition restrictions have eased. Meanwhile the pending acquisition by Kinderhook adds layers of near-term uncertainty influencing stakeholder behavior potentially constraining corporate agility until deal closure — an event whose timing remains indeterminate yet will materially pivot Enhabit's future strategic landscape either through ownership transition or status quo continuation if terminated. Ultimately investors should contextualize recent financial improvements within these broader thematic risks while appreciating Enhabit's well-established competitive strengths underpinning its positioning within the fragmented yet consolidating US home health/hospice market sector.

This analysis is based solely on publicly available information sourced from SEC filings ([F1],[S1]-[S29]) and relevant news articles ([N1]-[N12]). It does not constitute investment advice or solicitation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments