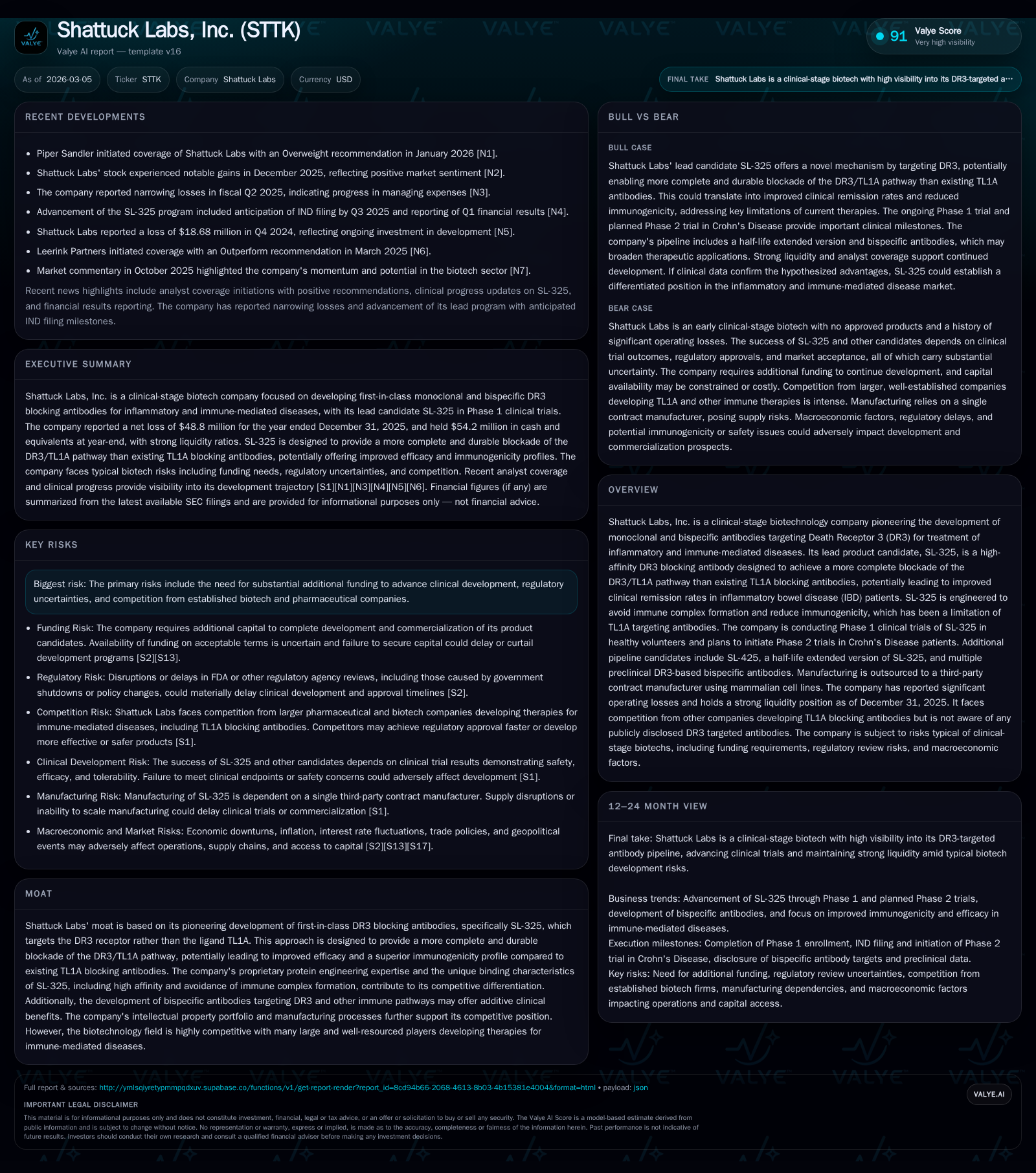

Shattuck Labs’ Strategic Leap in DR3 Antibody Innovation Spurs Clinical Promise

Shattuck Labs leverages pioneering DR3-blocking antibodies with promising clinical and financial trajectories amid intensive R&D investment.

Shattuck Labs is developing first-in-class monoclonal antibodies targeting the DR3 receptor for inflammatory diseases, notably SL-325 for inflammatory bowel disease (IBD). The company’s proprietary approach aims to offer superior pathway blockade and immunogenicity profile compared to existing TL1A blockers. Financially, Shattuck Labs shows steady reduction in losses driven by clinical progress, supported by a solid cash runway extending into 2029. Phase 1 trials of SL-325 are underway with Phase 2 initiation planned in Crohn’s Disease patients by Q3 2026. Key risks include regulatory uncertainties, capital needs, and competitive pressures typical of early-stage biotech.

Accelerating Innovation: The Science Behind SL-325’s Differentiation

Shattuck Labs has carved a distinct niche within the immunology space by targeting Death Receptor 3 (DR3) — the exclusive receptor for Tumor Necrosis Factor-Like Ligand 1A (TL1A) — with its lead monoclonal antibody candidate, SL-325. Unlike prior approaches focusing on neutralizing the ligand TL1A itself, Shattuck's strategy involves blocking the receptor side of the pathway to achieve a more comprehensive receptor occupancy (RO). In preclinical head-to-head studies against TL1A blockers (sequence equivalents to leading competitors), SL-325 demonstrated superior blockade of TL1A binding to DR3 [S1]. This mode of action promises not only more durable pathway inhibition but may circumvent a significant limitation among TL1A-targeting antibodies: immune complex formation.

By binding DR3 directly, SL-325 is engineered to avoid immune complex formation that typically arises from TL1A antibody engagement with soluble ligand—known to trigger high rates of anti-drug antibody (ADA) production. Elevated ADAs undermine treatment efficacy particularly in inflammatory bowel disease (IBD) patients, challenging current therapeutics targeting the TL1A ligand [S1]. Furthermore, Shattuck optimized SL-325 as an Fc gamma receptor-silenced monoclonal antibody, minimizing risk of antibody-dependent cellular cytotoxicity (ADCC) or phagocytosis events which might complicate safety profiles. The epitope targeted on DR3 also avoids inducing receptor-mediated endocytosis, contributing to durable RO observed lasting at least two months in non-human primate (NHP) studies [S1]. This constellation of protein engineering advances underscores Shattuck's emphasis on improving both efficacy and immunogenicity within a notoriously challenging therapeutic class.

Historical Financial Trends: Improving Losses Amid Heavy R&D Investment

Since inception, consistent with many clinical-stage biotechs focused on novel immunotherapies, Shattuck Labs has operated at a loss given its absence of commercial products and revenues. However, financials reveal measured progress; over the four-year period ending FY2025, the company has reduced its operating loss annually by roughly 36% year-over-year (YoY), signaling tighter expense management aligned with clinical milestones [F1]. Net loss followed a similar path—dropping from -$101.9 million in FY2022 to -$48.8 million in FY2025—a reflection of focused resource deployment primarily in R&D rather than SG&A expansion.

Operating cash flow also improved from a negative $94.5 million in FY2022 to negative $39.9 million in FY2025. Capital expenditure remains minimal relative to operational spend, indicating limited fixed asset purchases typical for early-stage biotech development [F1]. Equity capital stood at $82.4 million at year-end 2025 despite accruing losses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -49 | -40 | -52 | 0 | +35.3% |

| 2024 | -75 | -61 | -81 | 0 | +13.6% |

| 2023 | -87 | -81 | -92 | 0 | +14.4% |

| 2022 | -102 | -94 | -103 | 12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -40 | -59.2 |

| 2024 | -61 | -94.7 |

| 2023 | -82 | -60.3 |

| 2022 | -106 | -57.9 |

Source: SEC companyfacts cache [F1].

Losses reflect intensive R&D investment characteristic of novel biologics development without current revenue streams [F1].

Clinical Milestones on the Horizon: Phase 1 Progress and Phase 2 Plans

Currently enrolled in Phase 1 single ascending dose (SAD) and multiple ascending dose (MAD) clinical trials evaluating safety and pharmacokinetics of SL-325 in healthy volunteers, completion is anticipated by Q2 2026 [S1]. These early-stage studies are critical for defining safe dosing ranges ahead of indication-specific efficacy trials.

Capitalizing on encouraging non-human primate toxicology outcomes—which highlighted no evidence of immunotoxicity or Fc-mediated cytotoxic effects—and leveraging patient safety data from analogous TL1A blockade programs conducted by others providing a derisked safety backdrop, Shattuck expects to launch randomized placebo-controlled Phase 2 trials in Crohn’s Disease patients around Q3 2026 [S1][N2]. Targeting DR3 as opposed to TL1A offers potential for more durable efficacy via robust receptor occupancy while mitigating ADA-driven reduced effectiveness tied to TL1A ligand blockers.

The differentiation is rooted in biological rationale: TL1A is solely responsible for signaling through DR3 without alternative receptors; thus attenuating DR3 blocks complete signal transduction versus partial ligand neutralization approaches [S1]. This mechanistic insight forms the backbone of Shattuck’s strategy heading into pivotal IBD study stages.

Capital Structure and Cash Management: Extending Runway to 2029

With $54.2 million in cash and equivalents reported at fiscal year-end December 31, 2025 [F1], Shattuck Labs maintains liquidity sufficient to fund continuing operations until approximately 2029 assuming no material shifts in burn rate [S2]. This runway benefits from historically declining cash outflows attributable mainly to more streamlined clinical operations.

However, capital adequacy hinges partly upon holders exercising common stock warrants whose outcomes remain uncertain due to market price variability relative to exercise prices as well as regulatory limits tied to Form S-3 offerings restricting sales volume until surpassing public float thresholds near $75 million [S2]. Warrant exercises could occur via cash or cashless mechanisms—the latter reducing incoming proceeds though limiting dilution effects.

Management signals openness toward further capital raises driven by favorable market conditions or strategic imperatives but acknowledges dilution risks inherent with such financings [S2][S29]. Regular assessment of capital sources vis-à-vis pipeline development timelines remains critical given absence of product revenues.

Market Risks and Regulatory Considerations Impacting Development Timelines

Extensive regulatory environments shape every facet of Shattuck's drug development—from preclinical research through eventual commercialization—with FDA approval pathways for biologics demanding substantial evidence of safety and efficacy under stringent cGMP conditions [S10][S16]. Any delays in patient enrollment or adverse findings could postpone milestone achievements.

Additionally, compliance with healthcare laws such as the Anti-Kickback Statute (AKS), False Claims Act (FCA), HIPAA privacy rules, and newer transparency mandates like the Physician Payments Sunshine Act imposes operational overheads and reputational considerations [S4][S5][S6][S7][S8]. Changing drug pricing reforms—e.g., Medicare negotiation provisions under recent legislation—introduce additional uncertainties affecting future reimbursement strategies [S11][S24].

Global regulatory complexities include EU Clinical Trials Regulation requirements post-Brexit alongside varied national laws regulating promotion practices potentially restricting marketing activities [S17][S21][S25].

Competition adds another challenge given established players developing diverse biologics targeting inflammatory pathways; Shattuck emphasizes proprietary engineering advantages but acknowledges inherent sector risks linked to patent enforcement costs and competing candidates entering similar indications [S12][S23][S27].

Future Growth Levers: Expanding the Pipeline Beyond SL-325

Beyond its lead asset SL-325, Shattuck develops next-generation molecules including SL-425—a half-life extended variant designed for longer systemic exposure potentially allowing less frequent dosing—and several bispecific antibodies simultaneously targeting DR3 alongside alternate immune checkpoints or TNF receptors [S1]. Such pipeline breadth aims to reduce reliance on a single clinical program while enabling additive or synergistic therapeutic modalities in complex immune-mediated diseases such as IBD.

This diversified pipeline approach aligns with common risk mitigation strategies observed among startups developing new molecular entities where incremental innovations can unlock improved patient outcomes or expanded indications post initial proof-of-concept achievements.

What Investors Should Watch: Catalysts and Potential Setbacks

Key near-term catalysts include top-line Phase 1 results expected mid-2026 providing insights into pharmacokinetics, safety profile, and initial receptor occupancy metrics critical for dose selection ahead of Phase 2 starts planned shortly after [N2][S1]. Trial enrollment rates will serve as operational health indicators given patient recruitment challenges prevalent in autoimmune trial landscapes.

Capital raise announcements or partnerships could act as liquidity inflection points but also pose dilution concerns depending on terms amidst prevailing market conditions [S29]. Competitive advancements from other biologics players or unexpected regulatory feedback altering trial designs represent downside risks that may delay timelines or increase costs.

Common stock warrant exercises remain an unpredictable source affecting near-term cash flows—monitoring trends here may offer clues regarding shareholder sentiment or financing pathways impacting overall capitalization structure.

This analysis is based solely on information publicly disclosed through SEC filings and reputable news outlets as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments