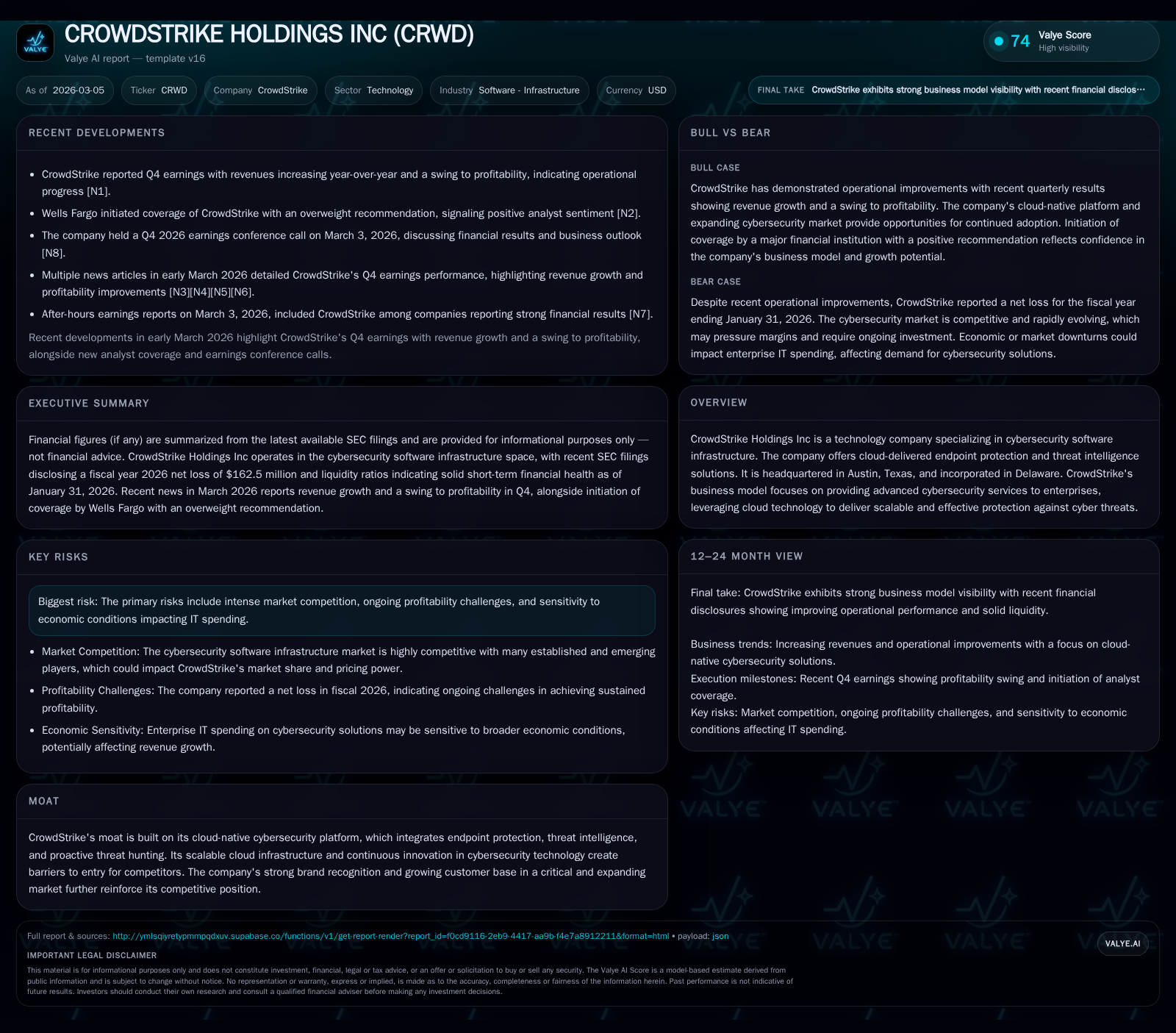

CrowdStrike’s Challenge: Balancing AI-Driven Growth with Profitability Pressures

CrowdStrike continues strong revenue expansion powered by its AI-native cloud platform but faces persistent operating losses amid heavy investments.

CrowdStrike Holdings Inc has established itself as a leading cloud-native cybersecurity provider with an innovative AI Security Cloud platform underpinning robust revenue growth. Despite accelerating top-line performance, the company struggles with sustained operating losses exacerbated by expanding costs in R&D and sales. Strong operating cash flows provide a counterbalance, reflecting efficient capital deployment and customer monetization. Going forward, market competition, economic sensitivity of IT spending, and evolving technology demands constitute key hurdles in CrowdStrike’s quest to translate growth momentum into consistent profitability.

Growth Trajectory Powered by AI Security Cloud

CrowdStrike has distinguished itself in the cybersecurity industry through its AI-native Falcon platform, a cloud-native solution that integrates endpoint protection, threat intelligence, and real-time prevention across enterprise environments [S1]. The company’s approach centers on a single lightweight sensor deployed across endpoints and workloads that collects extensive telemetry only once. This data is then reused for multifaceted security functions — from detection to automated response — empowered by machine learning fueled by cyber Reinforced Learning from Human Feedback (RLHF). This creates a network effect where increasing data volumes enhance model intelligence, raising barrier to entry against competitors.

Historically, this technological foundation supported strong revenue expansions evidenced by beating Wall Street expectations for Q4 and fiscal year 2026 revenues [N1][N4]. Though exact revenue figures are not disclosed in the evidence cache [F1], the persistent double-digit growth narrative is consistent with CrowdStrike’s position as an innovator defining the AI Security Cloud category [S1].

Operating income trends show an intensifying loss profile as CrowdStrike scales: operating income deteriorated from -$190 million in FY2022 to -$293 million in FY2026 [F1]. Despite this expanding loss, net income dynamics reveal significant swings including a positive net income spike in FY2023 followed by a plunge back into negative territory (-$163 million) in FY2026 — underscoring the cost pressures inherent in rapid scaling.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | -163 | 1612 | -293 | 302 | |

| 2024 | -19 | 1382 | -120 | 255 | -121.6% |

| 2023 | 89 | 1166 | -2 | 177 | +148.7% |

| 2022 | -183 | 941 | -190 | 235 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2026 | 1310 | -3.7 |

| 2024 | 1127 | -0.6 |

| 2023 | 990 | 3.9 |

| 2022 | 706 | -12.5 |

Source: SEC companyfacts cache [F1].

Note: Operating and net income deltas reflect deepening losses coinciding with accelerated investment phases; CFO growth indicates improving operational cash generation [F1].

Q4 and Fiscal Year 2026: Surpassing Revenue Estimates Amid Operating Losses

The Q4 fiscal 2026 earnings announcement highlighted continued strength on revenue growth that exceeded analyst consensus [N1][N4]. Management commentary on the earnings call elaborated on accelerating customer acquisition especially among large enterprises adopting Falcon’s integrated platform capabilities [N2]. However, these gains come at a cost to profitability as operating expenses surged.

Operating income declined by over 140% year-over-year in FY26 compared to FY25 [F1], driven largely by increased R&D investments aimed at expanding AI capabilities and broadening platform integration. Enterprise sales costs also rose materially reflecting intensified competition for larger deals.

Despite these losses at the profit line, CrowdStrike reported a swing toward positive quarterly profits on certain adjusted metrics during Q4 itself — exemplifying how subscription-based SaaS models can produce lumpy earnings results amid front-loaded customer acquisition spending [N5]. The juxtaposition of robust top-line beats with continuing operating deficits captures the tension between growth scaling and margin expansion.

Strategic Drivers Behind Falcon Platform Adoption

At the heart of CrowdStrike's competitive edge lies its Falcon platform architecture described in detail within its SEC filings [S1]. Contrasting legacy cybersecurity solutions built as collections of point products blended post hoc, Falcon operates as a purpose-built unified system.

Its core component is a single lightweight sensor designed for minimal system impact while delivering comprehensive telemetry across endpoints, identities, cloud workloads, and third-party integrations. This consolidated data ingestion eliminates redundant data collection cycles and fuels diverse AI-driven detection engines.

Moreover, Falcon leverages deep neural networks trained on trillions of weekly security events combined with realtime human insights via RLHF. This enables automatic prevention actions executed at machine speed against evolving adversaries increasingly leveraging automation themselves. CrowdStrike’s continuous enhancement of sensor intelligence and platform breadth supports greater customer retention through reduced breach incidents and simplified security operations.

This architecture fosters economies of scale uncommon in traditional cybersecurity firms where legacy update cycles often lag threat morphologies. It also simplifies IT overhead by consolidating fragmented security tools into one scalable SaaS platform.

Profitability Dynamics: Operating Losses vs. Robust Operating Cash Flow

Although accounting profits remain negative — with an operating loss of approximately $293 million for FY2026 — CrowdStrike generates strong operating cash flow ($1.61 billion), reflecting underlying business efficiency [F1]. The notable divergence between net losses and positive cash generation can be attributed to non-cash charges including stock-based compensation, amortization of intangible assets associated with acquisitions, and deferred revenue recognition patterns typical for subscription businesses.

Capital expenditures increased moderately to roughly $302 million in FY26 (+18.5% YoY), directed largely toward cloud infrastructure enhancement supporting its global network backbone [F1]. After deducting capex from CFO, free cash flow remains strongly positive at approximately $1.31 billion annually.

This robust free cash flow profile underlines CrowdStrike’s ability to fund aggressive R&D spending without reliance on external financing currently despite near-term accounting losses.

Capital Allocation: Investment for Expansion Vs. Shareholder Returns

Cash and equivalents reached above $5.2 billion entering FY27 [F1]. This liquidity buffer empowers continued reinvestment prioritizing innovation rather than returning capital through dividends or repurchases; no buybacks have been recorded recently [F1].

The strategy reflects management's focus on maximizing long-term value creation by funding advanced AI research initiatives, expanding product offerings beyond endpoint protection into identity and workload coverage areas, and growing global go-to-market channels.

Given the scale of recurrent free cash flow positive operations, future capital allocation flexibility appears strong although shareholders should monitor any shifts toward distribution policies if profitability recovers sustainably.

Competitive Landscape and Market Risks Influencing Growth Prospects

CrowdStrike faces vigorous competition from established incumbents such as Palo Alto Networks and Microsoft Defender alongside nimble startups innovating around zero trust architectures or specialized threat intelligence services [S1][S4]. The market’s rapid evolution requires constant innovation investment which pressures margins further.

Economic headwinds impacting IT budgets represent a meaningful risk; enterprises may delay or compress cybersecurity projects during downturns affecting new logo acquisition rates or renewal pricing power [S4][S5]. Increased regulatory scrutiny around data privacy and incident reporting could raise compliance costs or legal risks; ongoing litigation matters inject additional uncertainty drawing executive focus away from operational execution [S4].

Investors should weigh these factors within broader industry tailwinds driven by escalating cyber threats globally necessitating modernized defense platforms.

Looking Ahead: Key Milestones and Factors to Monitor

Explicit forward guidance remains cautiously framed given historic margin volatility [N2]. However, sell-side analyst endorsements such as Wells Fargo’s Overweight initiation highlight confidence in CrowdStrike’s secular growth prospects sustained by pipeline strength and innovation cadence [N8]. Piper Sandler's recent upgrade echoes similar sentiment emphasizing cross-selling potential within existing large accounts alongside new client wins [N14].

Key milestones include successful launch cycles extending Falcon into adjacent security domains (identity protection, DevOps security), progression toward positive GAAP profitability measures sustained beyond quarter perturbations, scaling managed detection & response offerings that deepen recurring revenue quality, plus continued expansion into international markets where penetration remains lower.

Monitoring improvements in gross margin percentages alongside stable or improving customer churn will provide tangible signals on Marketplace acceptance balancing scale economies against competition-induced pricing pressures.

This analysis synthesizes known quantitative results with detailed qualitative disclosures assembled from regulatory filings and recent market reports aiming to offer a nuanced view on CrowdStrike Holdings’ strategic progress. While exhibiting leadership fueled by AI innovation powering notable top-line growth trajectories coupled with strong operating cash generation capability, CrowdStrike must navigate persistent profitability challenges amidst intensifying competitive pressures across an economically sensitive cybersecurity domain.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments