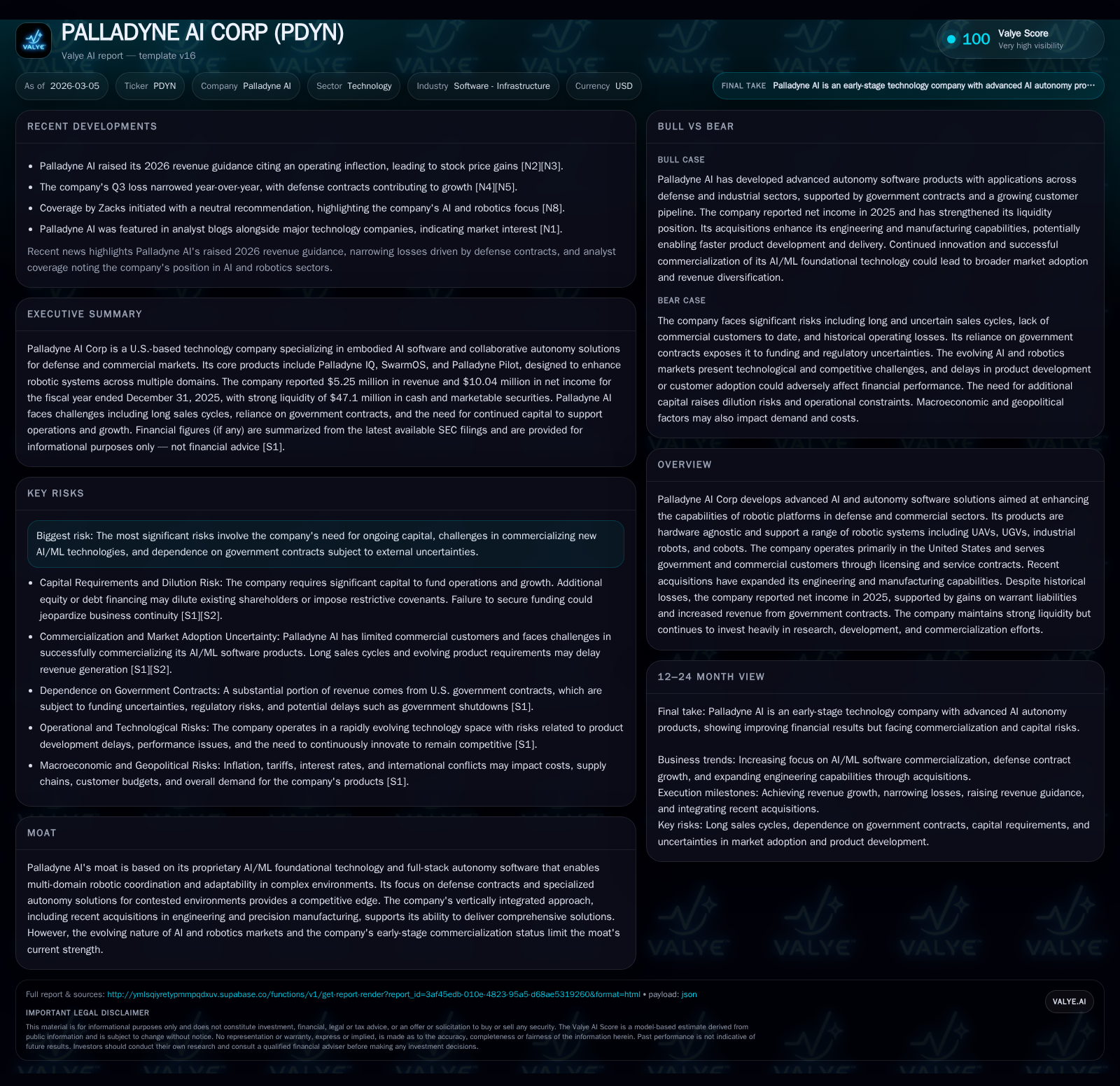

Palladyne AI Corp Achieves First Net Income Despite Revenue Decline and Heavy Investment

The U.S.-based AI autonomy software company reported improvement to net profitability in 2025 amidst ongoing commercialization challenges and substantial R&D expenditures.

Palladyne AI Corp, focused on advanced embodied AI and autonomy solutions for defense and industrial robotics, reported a notable milestone with positive net income in 2025 despite revenue declining by over 30% year-over-year. The company’s strategy includes leveraging proprietary AI foundational technology and expanding through strategic acquisitions to build vertical integration, particularly targeting government contracts. Heavy investment in research, development, and commercialization continues to pressure operating margins and cash flow, with operating losses of $32.4 million and negative free cash flow of approximately $28.3 million in 2025. Liquidity remains strong with over $47 million in cash and marketable securities supporting near-term operations. Moving forward, Palladyne faces risks around lengthy sales cycles, dependence on government contracts, and the evolving competitive dynamics in AI-driven robotics autonomy.

Overview

Palladyne AI Corp operates at the intersection of AI-driven robotics autonomy with a portfolio encompassing full-stack embodied AI software for UAVs (unmanned aerial vehicles), UGVs (unmanned ground vehicles), cobots, industrial robots, and maritime autonomous platforms. Its offerings—including Palladyne IQ, SwarmOS, and Pilot—are designed to be hardware agnostic enabling broad applicability across defense and commercial sectors [S1].

The company positions itself as a mid-tier U.S. prime defense contractor leveraging its proprietary autonomy software stack combined with recent acquisitions in engineering design, manufacturing, and precision machining to create an integrated solution capability [S1][S4]. Its focus centers on contested environments requiring resilient multi-vehicle coordination via adaptive AI models suitable for degraded communication scenarios.

Historical Performance

Fiscal years 2022 through 2025 reflect a trajectory of declining revenues but improving net income driven primarily by non-operating financial items:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5 | 10 | -28 | -32 | -32.6% | +113.8% |

| 2024 | 8 | -73 | -23 | -27 | +26.7% | +37.2% |

| 2023 | 6 | -116 | -77 | -121 | -57.8% | +26.4% |

| 2022 | 15 | -157 | -65 | -177 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -28 | 13.4 |

| 2024 | -23 | 761.7 |

| 2023 | -77 | -282.6 |

| 2022 | -67 |

Source: SEC companyfacts cache [F1].

Table sourced from SEC company facts data [F1].

Revenue peaked in FY2022 driven by government contracts but declined subsequently as Palladyne shifted focus away from legacy hardware toward scalable AI/ML software autonomy products [S1][S8]. Operating losses narrowed compared to prior years but remain significant due to ongoing heavy investments in R&D and commercialization efforts [F1][S12].

The positive net income recorded in FY2025 was influenced substantially by gains related to warrant liabilities rather than core operational profitability [F1], highlighting ongoing challenges turning top-line into sustainable profits.

Growth Outlook

Key growth drivers include:

- Commercialization Progress: Advancement of Palladyne IQ, SwarmOS, and Pilot through customer trials toward broader market adoption is vital for revenue growth; sales cycles are protracted up to or beyond 12-18 months given the nascent technology nature [S1][S4].

- Government Engagement: Defense contracts provide a foundation but entail exposure to budgetary fluctuations and procurement timing uncertainties [S1][S9].

- Vertical Integration: Late-2025 acquisitions of GuideTech, MKR Fabricators, and Warnke Precision Machining enhance production capabilities potentially improving cost efficiency and time-to-market while enabling proprietary UAV platform development [S4][S10].

- Market Acceptance Risks: Adoption hurdles remain due to customer caution around new AI/ML technologies in mission-critical settings requiring resilience and trustworthiness under contested environments [S1][S9].

These factors present both opportunities and risks as Palladyne navigates early commercialization stages amid competitive pressures.

Milestones and Expectations

While explicit guidance is not provided publicly, investors should monitor:

- Revenue ramp during continued commercialization efforts.

- Progress integrating acquired engineering/manufacturing capabilities.

- Backlog development: estimated remaining performance obligations were approximately $13.9 million at end-2025 expected mainly within one year [S17].

- Cash burn trends relative to equity financing activities which raised nearly $70 million gross between late-2024 and end-2025 [S19][S24].

Capital Allocation & Returns

Despite attaining positive net income ($10 million) in FY2025, Palladyne operated at a substantial operating loss (-$32 million) alongside negative free cash flow approximated at -$28.3 million (operating cash flow minus capex), reflecting continued investment intensity [F1]. No dividends or share repurchases were disclosed.

Equity strengthened significantly from negative territory (~–$9 million) at end-2024 to $74.7 million at end-2025 following large equity raises during the period providing liquidity for operations extending beyond the next twelve months barring unforeseen events [F1][S23][S4][S13].

The approximate return on equity for FY2025 is about 13%, though this should be interpreted cautiously given non-operating items contributed materially to net income rather than sustainable operational earnings [F1].

Industry Context & Competitive Positioning

Palladyne operates within a complex ecosystem where autonomous robotics software solutions face lengthy sales cycles due to rigorous validation requirements inherent to defense applications.

Hardware agnosticism of Palladyne’s AI stack aligns with industry demand for flexible integration across various robotic platforms avoiding vendor lock-in.

The company’s focus on edge-native orchestration supports decentralized decision-making critical for contested domains where connectivity may be compromised.

Competitive pressures arise from established defense primes investing heavily alongside innovative startups rapidly advancing autonomous capabilities.

Risks Summary

Key risks include:

- Dependence on volatile government spending affecting contract timing and revenue recognition.

- Potential need for additional external capital that could dilute shareholders or impose operational constraints if financing terms are unfavorable [S14][S7].

- Uncertainty around customer adoption given novel technology requiring extended sales cycle maturation.

- Customer concentration risk as two clients represented approximately 73% of revenue in FY2025 amplifying sensitivity to contract changes [S10].

- Legal proceedings currently immaterial but could pose costs if circumstances shift unexpectedly [S16].

Conclusion

Palladyne AI Corp reached an important milestone achieving positive net income in FY2025 amidst ongoing operating losses characteristic of early-stage technology companies pursuing innovation in defense autonomy software.

Its strategic acquisitions demonstrate commitment to vertical integration aimed at scalability but also increase near-term resource demands.

Maintaining execution discipline on commercialization while managing liquidity will be pivotal for translating technological advances into sustainable financial performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments