Barnwell Industries Confronts Operational and Governance Headwinds

Latest quarterly disclosures reveal Barnwell's intensified operational challenges and governance struggles impacting liquidity and strategic direction.

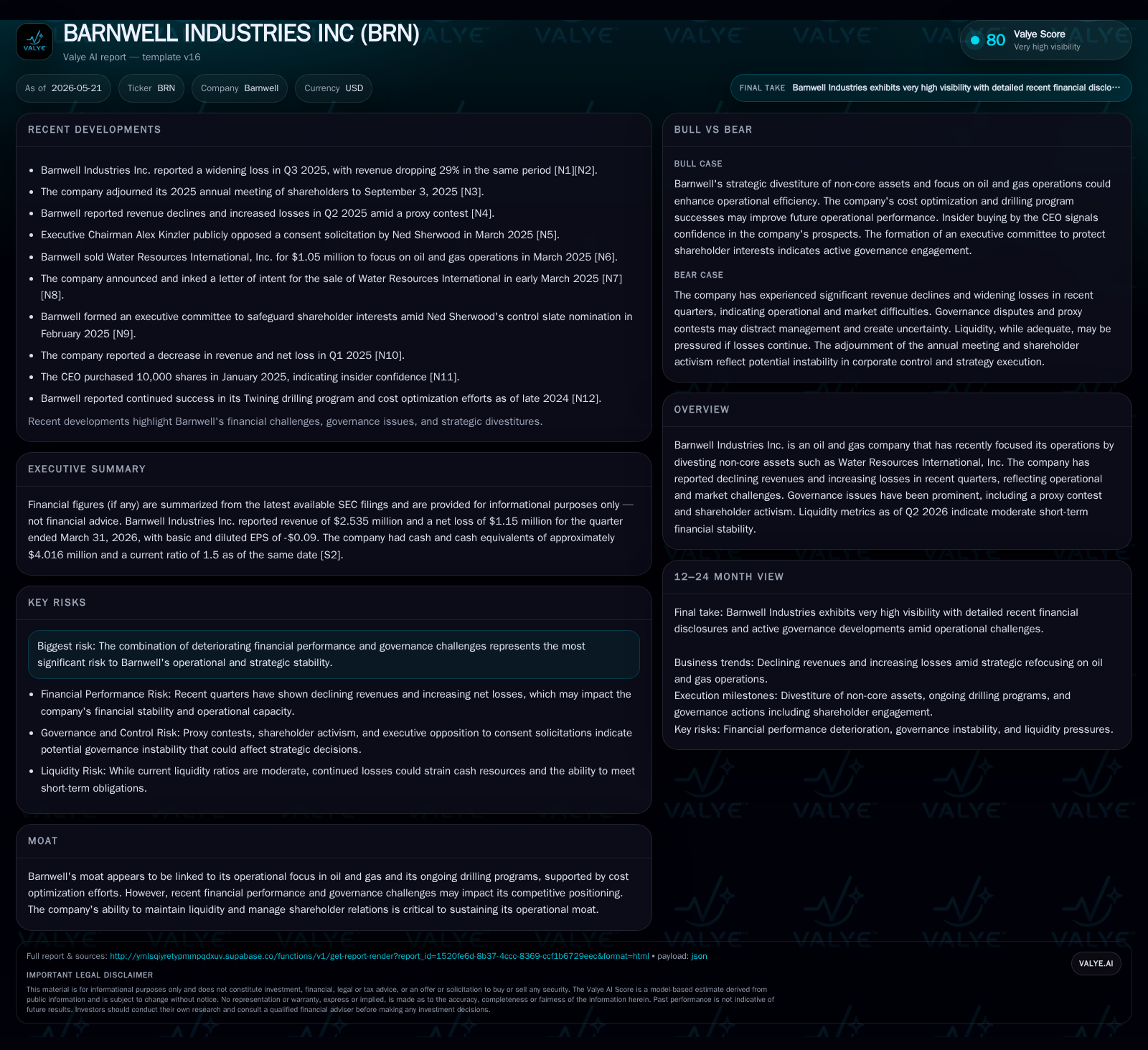

Barnwell Industries reported declining revenues and widening losses in its latest quarter, underscoring ongoing difficulties in its upstream oil and gas operations. The company is sharpening its focus through divestitures of non-core assets but faces significant governance tensions including shareholder activism. Liquidity remains moderate with a current ratio of 1.5, though financial pressures persist. Operational growth hinges on drilling program efficiency and cost controls, while governance stability is crucial to navigating upcoming milestones.

Recent Quarterly Operating Update Highlights

Barnwell Industries’ Q2 2026 (ending March 31) filings illuminate a challenging operating environment marked by declining revenues along with increasing net losses [S2]. The company continues to execute divestitures, notably having exited Water Resources International, signaling a tighter operational focus on upstream oil and gas activities [S1], [S3]. Notably, Barnwell received a cash distribution from minority partnership interests earlier in March 2026 which supports near-term liquidity [S3]. The balance sheet as of quarter-end retains roughly $4 million in cash with current assets exceeding current liabilities by a healthy margin—translating into a current ratio around 1.5 [F1], [S2]. While short-term liquidity appears adequate, the combined effect of revenue pressure and wider losses underscores operational execution risks as Barnwell navigates this pivotal period.

Barnwell’s Business Model: Oil & Gas Focus and Asset Divestitures

Barnwell’s core revenue generation post-divestiture centers on upstream oil and natural gas exploration and production operations. Historically diversified with land investment and other segments, the company’s strategic shedding of non-core assets such as Water Resources International refines its exposure to commodity markets primarily through production volumes from proven reserves [S1], [S3]. Buyers in this model are typically end-market consumers or intermediaries purchasing hydrocarbon outputs. Revenue fluctuates with commodity prices while volume depends on drilling activity and field productivity. Prices are subject to global market forces making earnings volatile. Cost structures heavily influence margins given fixed expenses related to drilling leases, asset retirement obligations, and regulatory compliance. By concentrating on upstream drilling projects, Barnwell seeks to optimize capital deployment but trades off diversification benefits it once enjoyed [S1].

Industry Environment and Competitive Positioning

Within the broader upstream oil & gas industry landscape, Barnwell qualifies as a smaller/mid-tier operator emphasizing operational efficiency. Unlike large integrated majors with sprawling reserves portfolios or downstream integration, Barnwell is focused on exploiting developed Canadian reserves alongside select U.S. properties [S1], [S2]. The industry environment mandates management of cost flexibilities amid capital intensity and regulation governing environmental remediation including asset retirement obligations [S13]. Supply chain constraints for drilling equipment or skilled labor can further challenge timely project execution. Peer firms benefit from scale advantages absent here; thus Barnwell’s competitive positioning relies on tight cost control measures plus securing stable customer contracts within fluctuating price regimes. Regulatory exposures related to land use permits, environmental liability budgeting, and tax regimes require ongoing vigilance common in the sector [S14].

Governance Dynamics Impacting Strategic Execution

Governance tensions have surfaced prominently for Barnwell during recent quarters despite no new material risk changes disclosed as of Q2 2026 [S2]. Proxy contests and shareholder activism weigh heavily on management’s bandwidth to drive forward strategic initiatives including asset sales or capital raises. These disputes likely amplify uncertainty among potential investors or partners while clouding consensus needed for operational continuity. Board-level decisions triggered by activist influences could shift strategic priorities abruptly or disrupt existing contractual relationships if unresolved. Thus governance dynamics constitute a critical watchpoint for assessing both near- and medium-term company trajectory [S2].

Growth Drivers Anchored in Core Operations and Cost Management

Growth prospects hinge fundamentally on operational enhancements within Barnwell’s upstream portfolio. Increasing drilling productivity through better well design or technology application can drive volume gains essential for revenue recovery amidst volatile pricing [S2]. Cost optimization efforts noted in recent filings including tighter overhead control improve margin resilience even as top-line remains pressured. Additionally, cash inflows from minority partnership interests provide non-operating liquidity support aiding capital allocation flexibility [S3]. Prudent reinvestment prioritizes proven high-return projects while managing asset retirement liabilities conservatively. These growth drivers remain circumscribed by prevailing market conditions but offer realistic avenues for incremental improvement if effectively executed.

Risks Stemming from Financial Performance and Shareholder Activism

Primary risks emerge from continued financial deterioration characterized by declining revenues coupled with increasing net losses observed recently [S2], [S1]. Commodity price volatility poses inherent threat exacerbating revenue unpredictability over short cycles. Governance instability fueled by shareholder activism introduces potential strategic distractions or shifts undermining execution consistency [S2]. Liquidity concerns persist given moderate cash balances relative to operating cost demands notwithstanding positive current ratios [F1]. Furthermore, regulatory compliance costs tied to environmental obligations remain a continuing expense pressure point for an upstream-focused company of Barnwell's scale [S14]. Collectively these risk factors pose credible constraints upon operational sustainability absent measured corrective actions.

Key Milestones to Monitor in Upcoming Quarters

Stakeholders should closely watch several milestones signaling either stabilization or exacerbation of challenges: production volume trends indicating drilling program effectiveness; progress toward reducing net losses; resolution or escalation of proxy contest and activist pressures; successful completion of additional asset monetizations enhancing cash flow; refinancing moves or equity offerings influencing capital structure; regulatory developments impacting operating costs; along with any unexpected write-downs tied to reserves evaluations. These markers will provide tangible evidence of execution trajectory critical for assessing Barnwell's evolving value proposition [S2], [S3].

Financial Snapshot: Liquidity, Profitability, and Capital Structure

As of March 31, 2026, Barnwell held approximately $4 million in cash equivalents supporting liquidity cushions against $4.3 million in current liabilities yielding a current ratio near 1.5—a moderate safety buffer for short-term obligations [F1]. Total debt metrics dated back prior years indicated relatively low leverage; no recent debt increase disclosures were evident indicating manageable financial gearing [F1]. Nonetheless, operating income remains marginal with reported widening net losses reflecting ongoing cost pressures coupled with revenue declines primarily linked to commodity exposure disruptions seen in the latest quarter’s bottom line results [S2], [F1].

Disclaimer: This analysis is based exclusively on disclosed SEC filings and company-provided data as of May 2026. No investment advice or research views are offered herein; readers should consult appropriate professional counsel before making any investment decisions.

Financial position in context

As of 2026-03-31, companyfacts shows $4mm in cash and equivalents [F1]. Current assets of $6mm and current liabilities of $4mm imply a current ratio near 1.5x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments