Brown & Brown Inc: Navigating Organic Challenges Amid Acquisition-Driven Growth in Insurance Brokerage

Brown & Brown Inc reported strong revenue growth fueled by acquisitions but faced organic revenue contraction and integration complexities in Q4 2025.

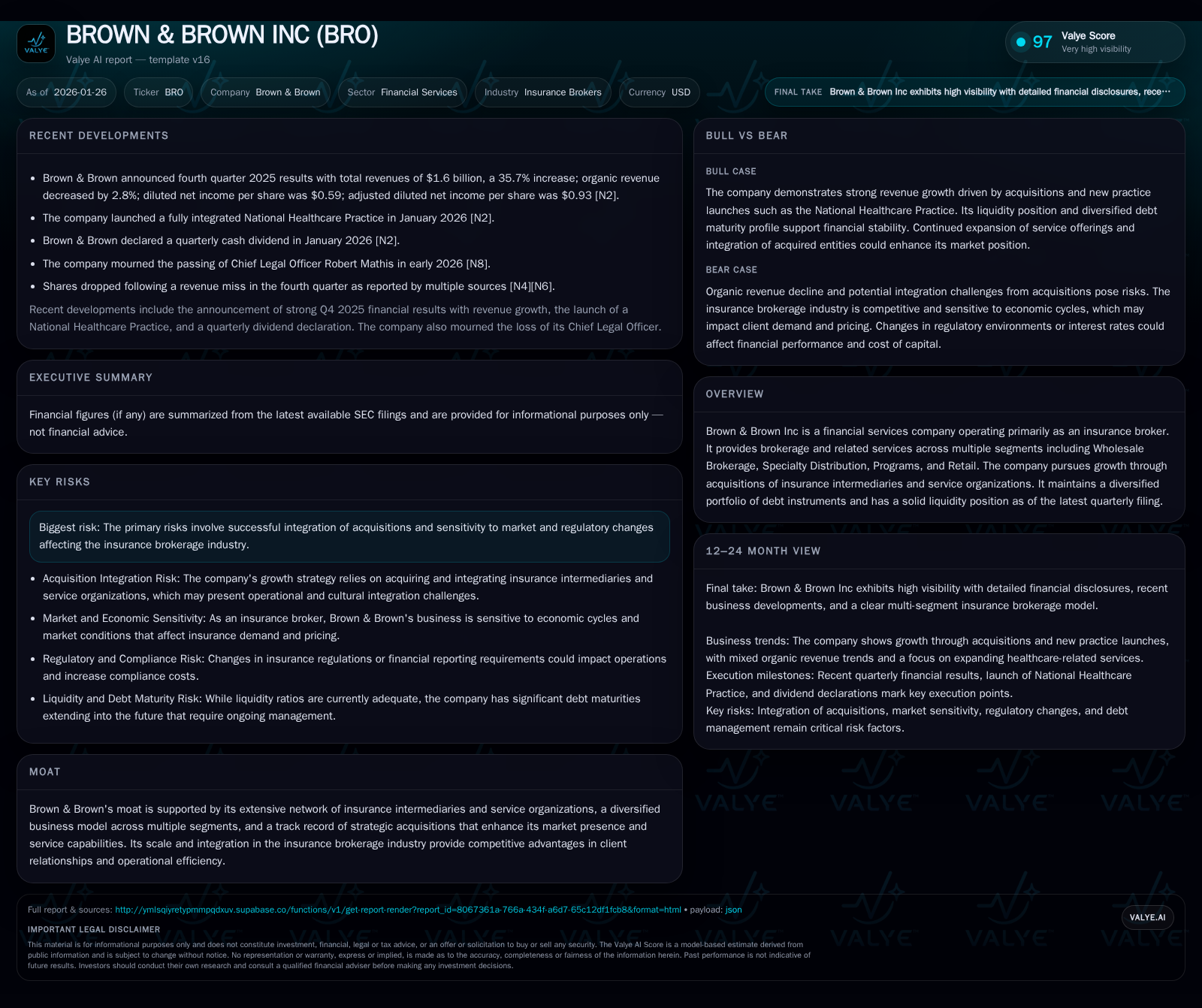

Brown & Brown Inc's fourth quarter 2025 results highlight the dual-edged nature of its acquisition-centric growth strategy, with total revenues rising 35.7% year-over-year yet organic revenues declining 2.8%. The company’s diversified insurance brokerage segments and scale offer competitive advantages, though recent earnings missed revenue expectations, triggering a share price dip. Brown & Brown’s solid liquidity and disciplined capital structure support continued acquisition activity, but integration execution and organic growth remain key operational challenges.

What changed recently

Brown & Brown Inc reported its fourth quarter 2025 earnings on January 26, showing total revenues of approximately $1.6 billion, marking a 35.7% increase year-over-year. However, this headline growth masks a 2.8% organic revenue decline, signaling underlying challenges in core operations absent acquisitions [N1]. Diluted net income per share stood at $0.59, while adjusted EPS was $0.93, figures that fell short of some market expectations and resulted in a share price decline following the announcement [N3][N4].

Key operational updates include the launch of a fully integrated National Healthcare Practice, indicating strategic expansion into specialized insurance distribution channels [N10]. The company also announced a quarterly cash dividend, underscoring confidence in its cash flow profile despite recent organic softness [N7]. On the leadership front, Brown & Brown mourned the passing of its Chief Legal Officer Robert Mathis, a notable event for corporate governance and continuity [N9].

Business model as a system

Brown & Brown operates primarily as an insurance brokerage and services platform, generating revenue through commissions and fees by intermediating between insurance carriers and end customers. Its business is segmented into Wholesale Brokerage, Specialty Distribution, Programs, and Retail, each targeting different customer niches and product lines [S1][S3].

The company’s growth engine is heavily reliant on acquisitions, having built a vast network of insurance intermediaries and service organizations since 1993. This strategy aims to expand geographic reach, diversify specialty offerings, and aggregate scale benefits. The firm typically structures deals with earn-outs, as evidenced by the $25 million maximum potential earn-out payable disclosed, highlighting ongoing acquisition-related expenses and risks [S2][S5].

Financially, Brown & Brown maintains a solid liquidity profile with over $1.19 billion in cash and equivalents and a current ratio above 1.1, which supports its acquisition pipeline and operational needs [S13]. The company carries $400 million in senior notes due in 2026 with a 4.6% coupon, suggesting manageable near-term refinancing or repayment obligations [S11]. Operating margins, as measured by EBITDAC, hover around 33%, indicating efficient cost management across its segments, though margin expansion is challenged by organic growth headwinds and integration costs [S7][S15].

Industry map & competitive battlefield

The insurance brokerage industry is characterized by fragmentation, with numerous regional and specialty brokers competing alongside national platform players like Brown & Brown, Marsh McLennan, Aon, and Willis Towers Watson. Brown & Brown’s competitive advantage stems from its acquisition scale, diversified segment coverage, and a strong intermediary network that drives client relationships and retention.

Wholesale Brokerage focuses on complex or hard-to-place risks, often requiring specialized underwriting expertise. Specialty Distribution and Programs serve niche markets with tailored insurance products, while Retail targets more traditional, direct client-facing brokerage services. The integration of these segments enables Brown & Brown to cross-sell and deepen client penetration.

Competitive dynamics include pricing pressures from carriers, regulatory uncertainties, and evolving client demand for integrated risk management solutions. The industry also faces digitization trends, with technology-enabled platforms altering traditional brokerage value propositions. Brown & Brown’s strategy to launch a National Healthcare Practice reflects an attempt to capture rising healthcare insurance complexity and regulatory-driven demand [N10].

Where the economics become real

Unit economics in insurance brokerage revolve around commission rates, client retention, and operational leverage. Brown & Brown earns commissions typically as a percentage of premiums placed, with variability by segment and product complexity. Organic revenue growth is critical to sustaining margin expansion, but the recent 2.8% organic decline points to pricing or volume pressures in certain lines [N1].

Acquisitions offer bolt-on revenue and cost synergies but come with integration expenses and earn-out liabilities, which can weigh on near-term profitability. The disclosed $25 million in potential earn-outs underscores this dynamic [S5]. Brown & Brown’s operating leverage is evident in EBITDAC margins near 33%, but sustaining these margins requires balancing growth investments with cost discipline [S7][S15].

Capital structure supports the model, with manageable debt levels and ample liquidity—$1.19 billion cash on hand and a current ratio of 1.18 enable opportunistic acquisitions without straining the balance sheet [S13]. However, the $400 million senior notes maturing in 2026 necessitate attention to refinancing strategies or cash allocation [S11].

Diligence questions / disconfirming signals

- What are the drivers behind the organic revenue decline? Is this due to market conditions, loss of client mandates, pricing pressure, or operational execution issues?

- How successful has the company been historically in integrating acquired intermediaries and realizing expected synergies? What is the track record on earn-out payments and related contingencies?

- To what extent does Brown & Brown face regulatory risks, especially related to tort reform or changes in liability insurance demand as noted in risk disclosures?

- How resilient is the company’s diversified segment mix in an economic downturn or insurance cycle shift?

- What are the potential impacts of digitization and insurtech competitors on Brown & Brown’s traditional brokerage model?

- How will the company manage the upcoming $400 million senior notes maturity in 2026 amid its acquisition and dividend policies?

- What is the potential effect of leadership changes, such as the passing of the Chief Legal Officer, on governance and strategic execution?

This analysis is based on publicly available company disclosures and recent news reports and does not constitute financial advice or a recommendation. It aims to provide a detailed operational and strategic overview of Brown & Brown Inc within the insurance brokerage industry context.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments