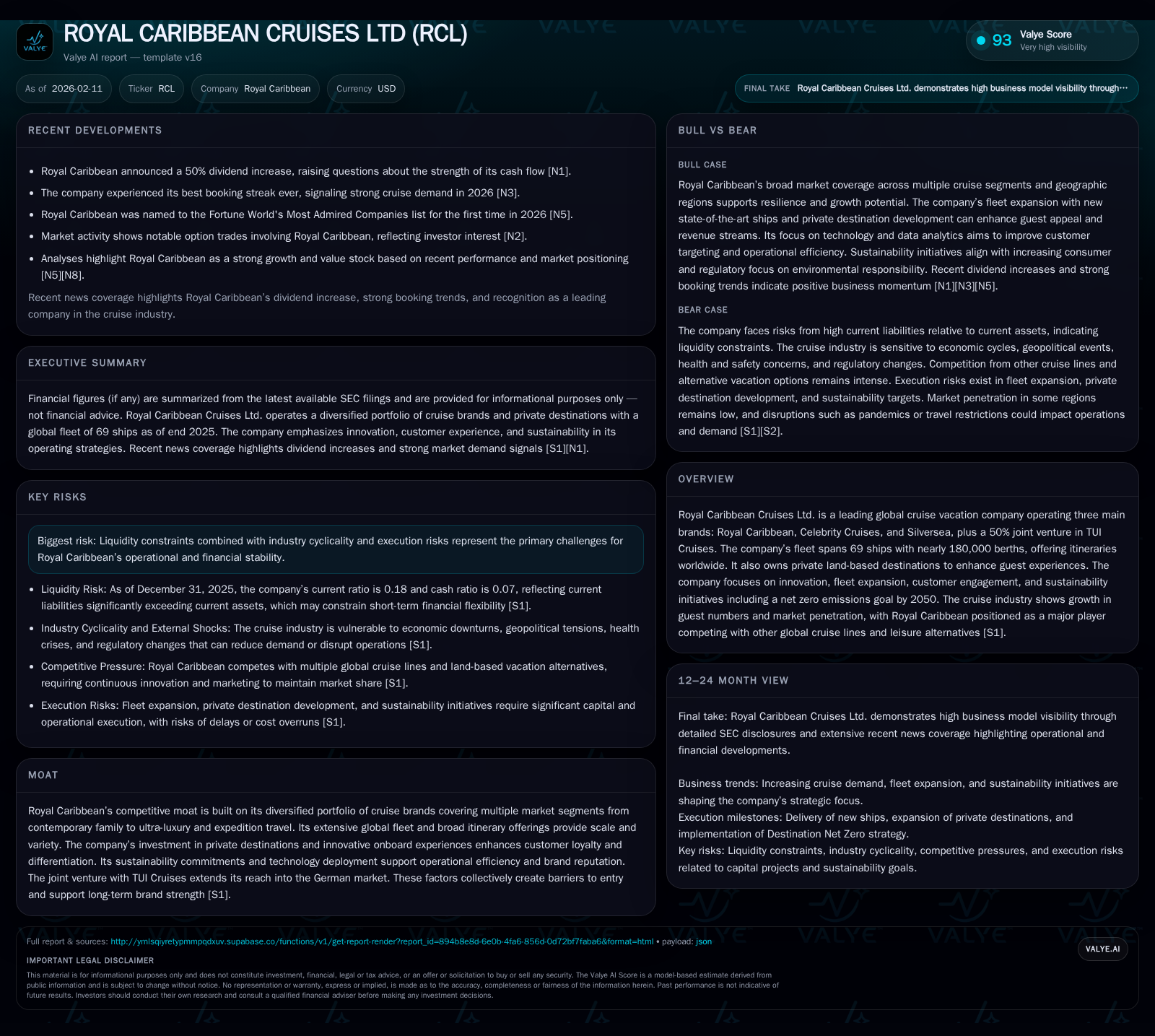

Royal Caribbean Cruises Ltd: Navigating Growth Amid High Leverage and Innovation in the Global Cruise Industry

Royal Caribbean’s bold dividend hike underscores a complex balance between robust earnings and constrained liquidity amid aggressive fleet expansion.

Royal Caribbean Cruises Ltd. occupies a commanding position in the global cruise industry through its diversified brand portfolio and expansive fleet. The company’s recent 50% dividend increase signals confidence backed by $4.27 billion net income in 2025, yet liquidity remains stretched, with a current ratio hovering around 0.18. Strategic investments in innovative vessels, private destination offerings, and sustainability initiatives underscore its competitive moat, but challenges from high leverage, cyclical demand, and cybersecurity require vigilant navigation.

Charting the Course: Royal Caribbean’s Market Position and Brand Portfolio

At the helm of the global cruise landscape stands Royal Caribbean Cruises Ltd., a powerhouse boasting three principal brands—Royal Caribbean, Celebrity Cruises, and Silversea—supplemented by a crucial 50% stake in TUI Cruises. With an aggregated fleet of 69 vessels housing nearly 180,000 berths, the company's scale offers unprecedented global reach across more than 1,000 destinations spanning all seven continents [S1]. This diverse brand architecture strategically covers vacation segments ranging from family-friendly casual cruising under Royal Caribbean to ultra-luxury experiences via Silversea.

This segmentation enables Royal Caribbean not only to capture a wide swath of consumer preferences but also to optimize itinerary diversity with cruise lengths varying from quick getaways to extended exploration lasting up to two weeks. The integration of the German market through the joint venture with TUI Cruises diversifies geographic exposure while expanding market share within Europe [S1]. The breadth of options positions Royal Caribbean not simply as a cruise operator but as an orchestrator of comprehensive vacation experiences.

Dividend Surge: What Royal Caribbean’s 50% Raise Signals About Cash Flow

In early February 2026, Royal Caribbean stunned observers by announcing an aggressive 50% dividend increase—a bold move that reverberated through investor sentiment and media coverage alike [N1]. Anchored by an impressive net income tally of approximately $4.27 billion for fiscal year ending 2025 [F1], this payout hike ostensibly reflects management’s bullish view on ongoing cash generation capabilities.

Yet beneath this buoyant headline lurks an important tension; current financial ratios reveal considerable liquidity pressure. The company reported a current ratio near a razor-thin 0.18 as of December 2025—a level that underscores disproportionate current liabilities totaling roughly $12 billion against current assets just over $2.2 billion [F1]. This suggests that while profitability shines through the income statement, short-term operational cash flow may be constrained by heavy working capital or debt servicing demands.

Such divergence between earnings strength and liquidity tightness invites scrutiny over whether forthcoming operational cash inflows can sustainably underpin both growth investments and shareholder returns without stretching the balance sheet further.

Fleet and Innovation: Building Competitive Moats Through Ships and Experiences

Central to Royal Caribbean’s moat is its deliberate investment in fleet renewal and technological advancement. The company meticulously accounts for its most significant assets—ships—through detailed capitalization and depreciation strategies that factor residual values between 10%-15%, allocating depreciation over estimated useful lives spanning 30-35 years [S1].

Beyond mere accounting finesse, these estimates consider evolving environmental regulations, technological obsolescence risks, and long-term market demand projections for cruising vacations. Planned drydocking at intervals ranging from thirty to sixty months underpins maintenance programs essential to sustaining class certifications required for operation [S1].

The strategic deferral of drydocking expenses spreads cost recognition steadily rather than incurring erratic spikes associated with periodic overhaul cycles. This disciplined approach smooths earnings volatility while preserving ship operating capabilities.

Innovation encompasses onboard experience enhancements alongside engineering advances—creating unique attractions ranging from novel dining concepts to immersive entertainment that differentiate Royal Caribbean ships from peers.

Private Destinations & Guest Engagement: Crafting Unique Value Propositions

Extending beyond oceanic voyages, Royal Caribbean leverages private land-based resorts such as Perfect Day and Royal Beach Club venues to augment guest engagement [S1]. These exclusive destinations integrate seamlessly with ship itineraries offering curated shore excursions imbued with brand-centric quality assurance.

Such proprietary land holdings serve dual strategic purposes: enhancing customer loyalty through differentiated experiences unavailable on competitor vessels; while creating additional revenue streams outside traditional cruise ticket sales. This land-sea synergy elevates the overall brand proposition by crafting comprehensive vacation ecosystems—a potent defense against commoditization pressures prevalent in leisure travel.

Financial Health Deep Dive: Liquidity Shorts Amidst Robust Earnings

Delving deeper into balance sheet dynamics reveals the paradox at Royal Caribbean’s financial core: despite healthy profitability demonstrated by $4.27 billion net income, liquidity measures paint a cautionary portrait [F1][S1]. Cash reserves totaling approximately $8.25 billion are substantial nominally but overshadowed by staggering current liabilities nearing $12 billion—translating into a current ratio at an exceptionally low threshold (0.18) that typically signals difficulty covering short-term obligations without asset liquidation or refinancing.

This imbalance likely stems from working capital strain alongside scheduled debt maturities borne out of recent fleet expansions financed largely through borrowed funds [S1]. Disparities between operational cash generation timing versus financial commitments create periodic funding gaps requiring vigilant treasury management.

While longer-term solvency remains intact owing to substantial asset backing and ongoing earnings power, this structural liquidity pinch imposes limits on managerial flexibility concerning capital expenditures or opportunistic acquisitions without increasing leverage risk.

Sustainability Ambitions and Regulatory Navigation in Cruise Operations

Royal Caribbean has publicly committed to achieving net zero emissions for its entire footprint by mid-century—an ambitious target set within a tightening regulatory environment governing maritime operations [S1].

This pledge necessitates continuous upgrades in vessel propulsion technologies including alternative fuels adoption, energy efficiency enhancements throughout ship systems, and investment into carbon offset measures. Regulator-mandated compliance drives accounting considerations influencing ship useful life assumptions along with capitalization policies for improvement projects aimed at environmental performance enhancements [S1].

Aligning sustainability actions with financial stewardship will be critical as regulatory frameworks mature internationally—potentially affecting operating licenses or imposing costly retrofits if standards shift abruptly.

Risk of Rough Seas: Cyclicality, Cybersecurity, and Execution Challenges

Underlying operational fragilities include cyclical demand sensitivity inherent to leisure travel industries susceptible to economic downturns or macro shocks [S1]. The high fixed-cost nature of cruise operations magnifies earnings volatility during these troughs.

A growing frontier of risk comprises cybersecurity threats impacting network integrity and passenger data protection. Royal Caribbean has constructed a rigorous cybersecurity governance framework led by seasoned CIO and CISO executives possessing decades of domain expertise—the latter maintaining close ties with leading cyber organizations like NIST [S1]. Frequent board-level reviews via an engaged Audit Committee ensure sustained attention towards risk mitigation strategies.

Execution risks also pertain to delivering promised innovation without cost overruns or delays which could erode competitive advantages or customer satisfaction - a perennial challenge given the complexity of modern mega-ships.

Navigating Competition: Market Trends and Position Versus Peers

Royal Caribbean sails within turbulent competitive waters marked notably by capacity surges from Carnival Corporation pushing increased supply particularly in key regions such as the Caribbean [N12]. While rising consumer discretionary spending supports cruise demand broadly [N2], margin pressures surface where pricing power faces dilution due to overcapacity.

Royal Caribean's distinct positioning via premium product innovation partially offsets these pressures enabling it to rally stock price gains exceeding double-digit returns early in 2026 after positive earnings surprises [N4][N6]. Yet balancing growth aspirations amid intensifying peer moves requires continued fleet differentiation plus agile market responsiveness.

Investment Outlook: Weighing Growth Against Financial Constraints

Weaving together strands illuminated throughout this analysis presents an image of Royal Caribbean as a voyage fraught with both opportunity and constraint [N6][N8][F1][S1]. Its impressive scale combined with innovative experiential offerings form resilient competitive moats supporting long-term relevance amidst evolving market tastes.

Conversely, stretched liquidity ratios coupled with cyclicality inherent in luxury leisure markets impart notable near-term risk flags demanding cautious stewardship around capital allocation including the recently enhanced dividend program [N1]. The question remains whether future cash flows will consistently underpin ambitious expansion plans without further tightening credit profiles or compromising operational flexibility.

As Royal Caribbean charts its path forward amidst competing imperatives — growth acceleration versus stabilizing financial footing — rigorous execution alongside adaptive governance will define its ability to navigate safely toward sustainable horizons.

This analysis is intended solely for informational purposes based on publicly available data as of February 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments