Blackstone Real Estate Income Trust’s Earnings Volatility and Capital Deployment Dynamics

Analyzing BREIT’s contrasting strong property-level income against steep net losses and its nuanced capital allocation within a private REIT structure.

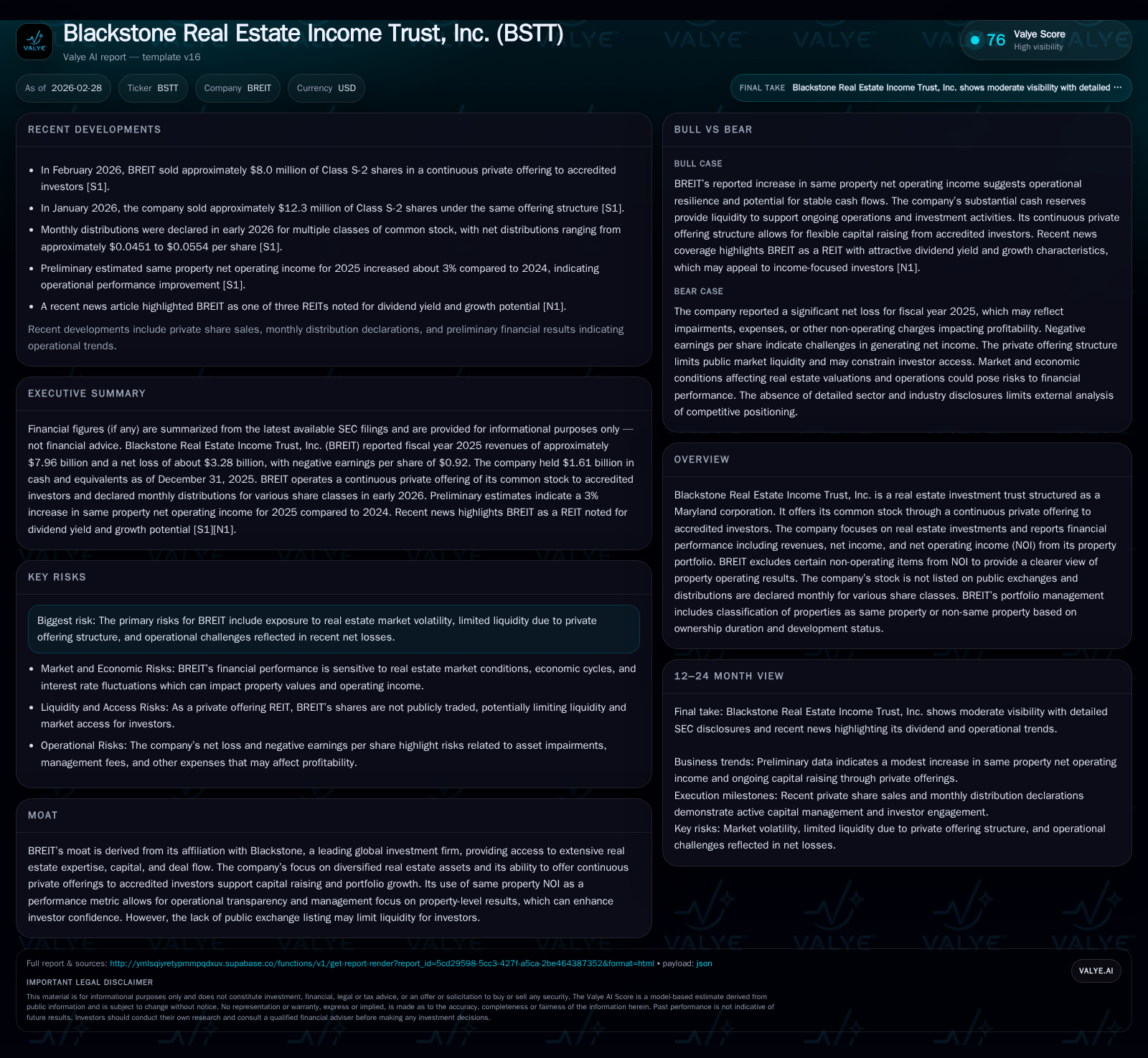

Blackstone Real Estate Income Trust (BREIT) exhibits resilient Same Property NOI growth amid significant net income volatility stemming from non-operational factors. While FY2025 revenue declined 6.7% and operating income fell 25.3%, property operations remain robust, supported by a diverse portfolio and disciplined management of real estate debt exposure. The firm's capital strategy balances monthly distributions, substantial share repurchases, and continued private equity offerings, all under a liquidity-constrained private market framework. A recent CFO transition may signal strategic continuity or recalibration going forward.

From Growth to Contraction: BREIT’s Recent Financial Trajectory

Blackstone Real Estate Income Trust’s most recent fiscal years encapsulate a tale of operational resilience shadowed by dramatic earnings deterioration driven predominantly by non-cash impairments and financial instrument impacts. Revenues peaked at $8.93 billion in FY2023 before trimming down steadily to $8.53 billion in FY2024 and further to $7.96 billion in FY2025, marking a 6.7% year-over-year (YoY) decline at the latest fiscal year-end [F1]. Operating income mirrored this trend more steeply with a drop of approximately 25%, from $5.41 billion in FY2024 to $4.03 billion in FY2025.

More strikingly, net income swung deeply negative: deteriorating from losses of around $890 million in FY2024 to an expansive loss of over $3.28 billion in FY2025 [F1]. This divergence reflects the pronounced influence of impairments, loss on extinguishment of debt, derivative losses, and other non-operating expenses that do not affect the core property operating results but significantly weigh on headline profitability.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8.0 | -3.3 | 2.3 | 4.0 | -6.7% | -268.8% |

| 2024 | 8.5 | -0.9 | 2.1 | 5.4 | -4.5% | -28.7% |

| 2023 | 8.9 | -0.7 | 2.7 | 6.0 | +16.8% | +21.7% |

| 2022 | 7.6 | -0.9 | 2.7 | 3.9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 1146 | 6.1 | -17.0 |

| 2024 | 1248 | 9.3 | -3.3 |

| 2023 | 1457 | 12.4 | -1.9 |

| 2022 | 1249 | 10.4 | -2.0 |

Source: SEC companyfacts cache [F1].

Revenue and income trends depict a peak followed by contraction amid intensifying non-operational charges.

Dissecting Operations: Property NOI and Investment Income Trends

BREIT’s management relies heavily on Same Property Net Operating Income (NOI) as a transparent barometer for actual real estate operation performance aside from accounting irregularities or transaction timing effects . For the year ended December 31, 2025, preliminary unaudited estimates indicated approximately a 3% increase in Same Property NOI over the prior year [S16], underscoring operational resilience despite the broader erosion in GAAP earnings.

This metric excludes items such as impairment losses, depreciation/amortization, asset disposals gains/losses, corporate costs, and derivative-related fluctuations, focusing instead on recurring rental income less property-level expenses . Notably absent from Same Property NOI are investment returns on real estate debt or equity securities which are reported separately.

The company’s ability to sustain same property NOI growth signals effective asset management and leasing strategies even as external market conditions produce headwinds elsewhere.

Navigating Market Risks: Interest Rate and Debt Exposure in Real Estate Debt Portfolio

BREIT holds about $4.8 billion invested in real estate debt instruments as of December 31, 2025 [S1]. These holdings predominantly carry floating interest rates indexed to Reference Rates akin to SOFR or LIBOR replacements common in commercial real estate lending markets.

Income from this segment is sensitive to rate movement: a quarter basis point (25bps) decline could trim annual income by roughly $10.4 million [S1]. This sensitivity flags exposure risks amid volatile interest rate environments, impacting net investment returns intermittently.

Risk mitigation strategies include diversification across collateral types and credit ratings aimed at managing market risk attributed to fair value fluctuations [S1]. However, fair value changes impose inherent uncertainty over realizable gains or losses upon asset disposition.

Capital Flow Strategies: Distributions, Share Repurchases, and Equity Issuance

Despite net losses at the GAAP level, BREIT continues supporting investor cash flows through monthly declared distributions differentiated by share class due to servicing fee variations [S4][S5]. February and January 2026 monthly distributions averaged approximately $0.0544 gross per share with net payouts varying slightly post-fees across classes such as Class I ($0.0544 net) versus Class S ($~0.0451 net).

For FY2025 overall dividends paid contracted modestly to roughly $1.15 billion from $1.25 billion prior year [F1], suggesting prudent alignment with cash flows.

Concurrent buyback programs remained robust albeit scaled back somewhat compared with previous years: FY2025 buybacks totaled about $6.13 billion versus over $9 billion in FY2024 [F1]. Share repurchases serve dual purposes—returning capital while managing NAV per share amid fluctuating market conditions.

Additionally, BREIT sustains capital raising through continuous private offerings exclusively available to accredited investors evidenced by several unregistered equity sales totaling tens of millions early in calendar year 2026 [S6][S7][S8][S18][S19]. These inflows support portfolio expansion or debt reduction without public-market constraints.

Private Market Challenges: Liquidity, Investor Access, and Structural Implications

BREIT’s exclusion from public exchanges confines investor liquidity relative to publicly traded REIT peers . The continuous private offering model limits secondary market transactions primarily to accredited institutional or high-net-worth individuals capable of meeting initial minimums.

While this private structure affords Blackstone consistent access to permanent capital coupled with fee structures aligned to long-term asset management objectives , it raises inherent challenges for investors seeking quick divestiture or price discovery mechanisms seen publicly.

As flagged among risk factors are operational complexities tied to funding liquidity needs during stressed markets without public market pricing transparency or immediate resale avenues [S9][S14][S16]. This tradeoff represents a key dynamic when assessing BREIT's investment proposition compared with listed vehicles.

Key Metrics to Monitor: Forecasts, NAV Trends, and Investment Milestones

The firm has not provided explicit forward-looking guidance or milestone targets at this reporting juncture within disclosed filings [N/A]. Going forward for analysts tracking BREIT:

- Stability or acceleration in Same Property NOI growth will be crucial,

- NAV accretion or depreciation trends will indicate asset revaluation momentum,

- Continuity of consistent monthly distributions per share class,

- Levels of fresh equity raised via continuous offerings reflecting demand,

- Progression on portfolio repositioning reducing impaired assets or enhancing stabilized rental cash flows. These markers collectively would convey directionality for earnings recovery potential under BREIT's hybrid real estate operating plus debt investment model.

Assessing Return on Equity and Cash Flow Sustainability

In light of net losses aggregating over -$3 billion for FY2025 against total equity near $19.33 billion at year-end [F1], implied ROE stands near -17%, reflecting accounting impairments overshadowing underlying economics.

However, operating cash flow tells a more constructive story — totaling approximately $2.29 billion in FY2025 up nearly 10% versus prior year [F1] — pointing towards strong property-level cash generation capable of underpinning continued distribution payments despite negative GAAP bottom line.

This divergence between accounting loss recognition (impairments/non-cash charges) versus tangible cash inflows is consistent with sector dynamics where mark-to-market volatility is decoupled from operating fundamentals.

Leadership Transition Impacts and Governance Overview

A significant governance update underlines the February 27th, 2026 appointment of Paul Kolodziej as Chief Financial Officer and Treasurer replacing Anthony Marone who steps down but remains integral as Blackstone’s Global Head of Real Estate Finance [S3][S21][S22].

Kolodziej's extensive internal experience within BREIT — spanning Controller roles through Deputy CFO since joining Blackstone Real Estate in mid-2016 — denotes a seamless succession supporting continuity amid complex financial landscapes.

His CPA background combined with deep SEC filing expertise adds robustness potentially critical as BREIT navigates evolving disclosure demands alongside strategic fiscal optimization initiatives moving forward.

Disclaimer: This analysis is based solely on publicly available documents including SEC filings that contain historical data without explicit forecasts or price data; it does not constitute investment advice nor recommendation concerning any security referenced herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments