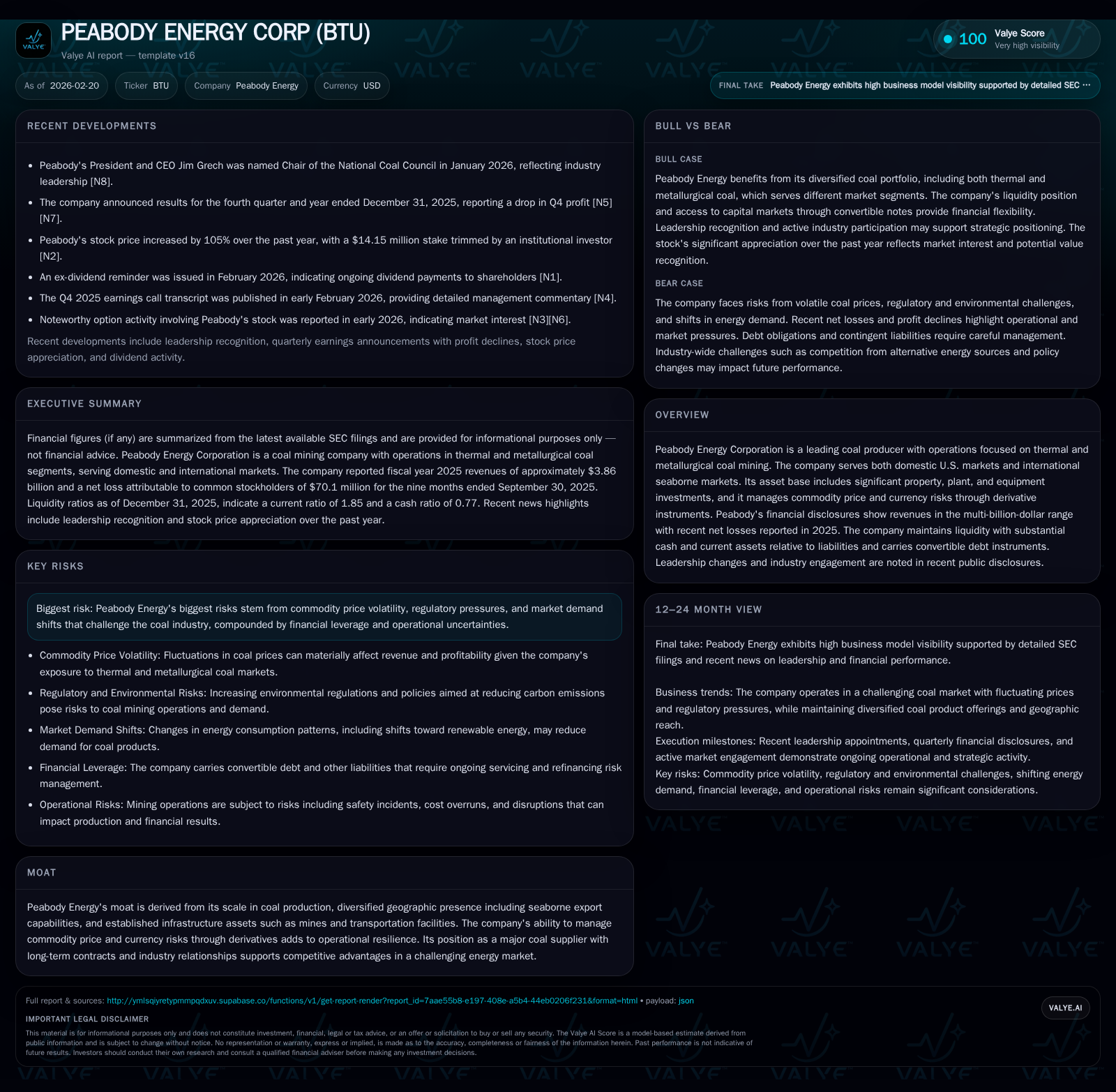

Peabody Energy’s Revenue Decline and Strategic Challenges in 2025

Peabody Energy’s 2025 financial setbacks highlight the complex interplay of coal market pressures, operational scale, and capital structure amid energy transition dynamics.

Peabody Energy Corp, a leading coal producer with diversified thermal and metallurgical coal operations, saw its revenue decline by 8.9% year-over-year to $3.86 billion in 2025 from $4.24 billion in 2024 amid falling commodity prices and regulatory pressures. Operating income swung from a $445 million profit in 2024 to an $80 million loss in 2025 driven by margin compression despite continued investments in property, plant, and equipment. The company maintains a robust liquidity position with a current ratio of 1.85 and manageable debt including $320 million in convertible notes due 2028. CEO Jim Grech’s industry engagement as chair of the National Coal Council underscores efforts to influence policy amid market challenges. Dividend payments persisted modestly while no share repurchases occurred in 2025. Near-term guidance remains qualitative; key watchpoints include coal price trends, regulatory developments, and convertible note conversion metrics.

Historical Earnings and Margin Contraction: A Timeline of Declining Revenue

Peabody Energy Corporation experienced notable revenue contraction culminating in fiscal year 2025 with revenues declining to approximately $3.86 billion from $4.24 billion in fiscal year 2024 — an approximate decrease of 8.9% year-over-year [F1]. This decline reflects sustained headwinds from lower global coal demand accelerated by competition from alternative energy sources and increased regulatory scrutiny.

Operating income deteriorated substantially with Peabody posting an operating loss of about $80 million in FY2025 compared to an operating profit of $445 million the prior year [F1]. Margin compression stemmed mainly from falling thermal and metallurgical coal prices alongside cost pressures related to compliance and asset maintenance amidst production scale optimization efforts [S1].

Net income data for FY2025 is limited to the nine months ended September but indicates a loss near $70 million, underscoring bottom-line challenges amid cyclical vulnerabilities faced by coal producers during secular demand shifts [F1].

Historical performance (annual)

| FY | Rev ($bn) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 3.9 | 334 | -80 | 411 | -8.9% |

| 2024 | 4.2 | 607 | 445 | 401 | -14.4% |

| 2023 | 4.9 | 1036 | 1075 | 348 | -0.7% |

| 2022 | 5.0 | 1174 | 1382 | 222 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Net, Div, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 0 | -78 |

| 2024 | 183 | 205 |

| 2023 | 348 | 687 |

| 2022 | 952 |

Source: SEC companyfacts cache [F1].

Note: Net income data beyond FY2019 is not explicitly reported in available tags; figures shown are based on latest nine-month data for FY2025[F1]

Operational Drivers and Cost Structure: Scaling Amid Declining Demand

Peabody’s significant asset base includes over $3 billion net book value invested in property, plant, equipment, and mine development supporting both thermal coal primarily for power generation and metallurgical coal used in steelmaking markets [S6][S13]. Its geographic diversification spans key U.S.-based Powder River Basin mines alongside export terminals serving Asia-Pacific markets which provide operational flexibility despite segment-specific challenges.

Commodity price risks are partially managed through derivative instruments including foreign currency options and commodity hedges; however, these do not qualify for cash flow hedge accounting resulting in earnings volatility directly impacted by market fluctuations [S28]. Operational cost controls face offsetting pressures from higher reclamation bonding costs and compliance expenses driven by evolving environmental legislation affecting the industry [S5].

Commodity Price Risks and Regulatory Hurdles Impacting Growth Outlook

Peabody’s risk disclosures highlight commodity price volatility as a core constraint on growth prospects compounded by heightened regulatory scrutiny around carbon emissions controls and mine safety oversight [S5]. Global decarbonization trends continue reshaping demand patterns—thermal coal faces particularly acute challenges in developed markets while metallurgical coal sales remain subject to international steel production cycles affecting export volumes [N12].

Regulatory restrictions potentially limit expansion or impose costly operational changes that bear on margins and capital allocation decisions going forward.

Leadership Engagement and Strategic Positioning

In January 2026, Peabody’s President & CEO Jim Grech was appointed Chair of the National Coal Council—an advisory body offering counsel to the U.S. Department of Energy on coal-related matters—reflecting strategic industry engagement aimed at influencing policy frameworks critical to Peabody's business model amidst energy transition challenges [N8].

While such advocacy may alleviate some regulatory risks, it does not fully offset secular demand headwinds.

Capital Structure, Liquidity Profile, and Debt Analysis

Peabody maintains a balanced capital structure highlighted by approximately $320 million senior unsecured convertible notes due March 2028 bearing a fixed coupon rate of 3.25%, payable semi-annually [S8][S10]. Conversion rights tied to stock price thresholds have not been triggered as of Q3’25 despite dividend-linked conversion rate adjustments implemented earlier in the year [S4].

A revolving credit facility established January ’24 with a maximum principal amount of $320 million is primarily utilized for letters of credit supporting reclamation bonding requirements rather than direct borrowings; about $270 million remained available at September ’25 with all financial covenants met [S9][S16].

Liquidity remains solid with cash & equivalents totaling approximately $575 million at December ’25 end alongside a current ratio near ~1.85 given current assets close to $1.56 billion versus current liabilities around $842 million as per latest filings [F1][S23]. Total long-term debt approximates $322 million exclusive of capital leases reflecting prudent leverage management consistent with covenant compliance [S6][S23].

Interest expense totaled roughly $33 million year-to-date Sept ’25 including amortization of debt issuance costs as non-cash charges; capitalized interest partially offsets cash interest payments maintaining financing cost control [S10][S16].

Dividend Policy, Share Repurchases & Shareholder Returns

Dividend payments have been sustained at approximately $0.225 per share annually ($0.075 quarterly), representing cautious capital return aligned with net income declines amid earnings pressure [N3][S11]. No common stock repurchases occurred during fiscal year 2025 following prior-year buybacks totaling about $183 million aimed at enhancing shareholder value through capital return programs [F1][S11].

The absence of repurchases combined with dividend preservation signals conservative capital allocation prioritizing balance sheet strength over aggressive yield strategies given free cash flow constraints—estimated free cash flow was negative roughly $77 million when subtracting capex from operating cash flow for FY2025 [F1].

Near-Term Guidance & Market Sentiment Observations

During its February ’26 earnings call covering Q4’25 results Peabody provided qualitative guidance emphasizing stable operations without explicit quantitative targets for Q1 or full-year ’26 results disclosed publicly [N1][N2]. Commentary underscored sensitivity to seaborne coal prices alongside evolving regulatory landscapes.

Market activity showed notable option trading volume on Peabody shares indicative of speculative or hedging positioning among institutional investors reflecting underlying uncertainty but also potential anticipation ahead of inflection points [N5][N7][N9]. The equity rallied strongly over the prior twelve months exceeding +105%, though recent stake trimming suggests selective profit-taking amid fundamental volatility [N4].

Key Milestones & Watchpoints Going Forward

Analysts should monitor:

- U.S. domestic policy developments impacting thermal coal demand including clean energy standards or federal support mechanisms.

- Metallurgical coal pricing linked closely to global steel production cycles affecting export revenues.

- Convertible note conversion rates influenced by cumulative dividends which affect potential timing of equity dilution.

- Management’s capital expenditure discipline balancing maintenance needs against constrained free cash flow outlooks.

- Outcomes from industry advocacy via bodies like the National Coal Council shaping legislative or subsidy environments.

- Operating cost trends related to environmental compliance or reclamation obligations that could further pressure margins.

Peabody’s position as one of the largest global coal suppliers coupled with substantial asset scale but facing secular deceleration requires vigilant assessment against broader macroeconomic shifts.

Disclaimer: This analysis is based solely on reported SEC filings, company press releases, news reports, and observed market data as cited; it does not constitute investment advice or recommendations but aims to present an informed view grounded strictly on available information up to February 20th, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments