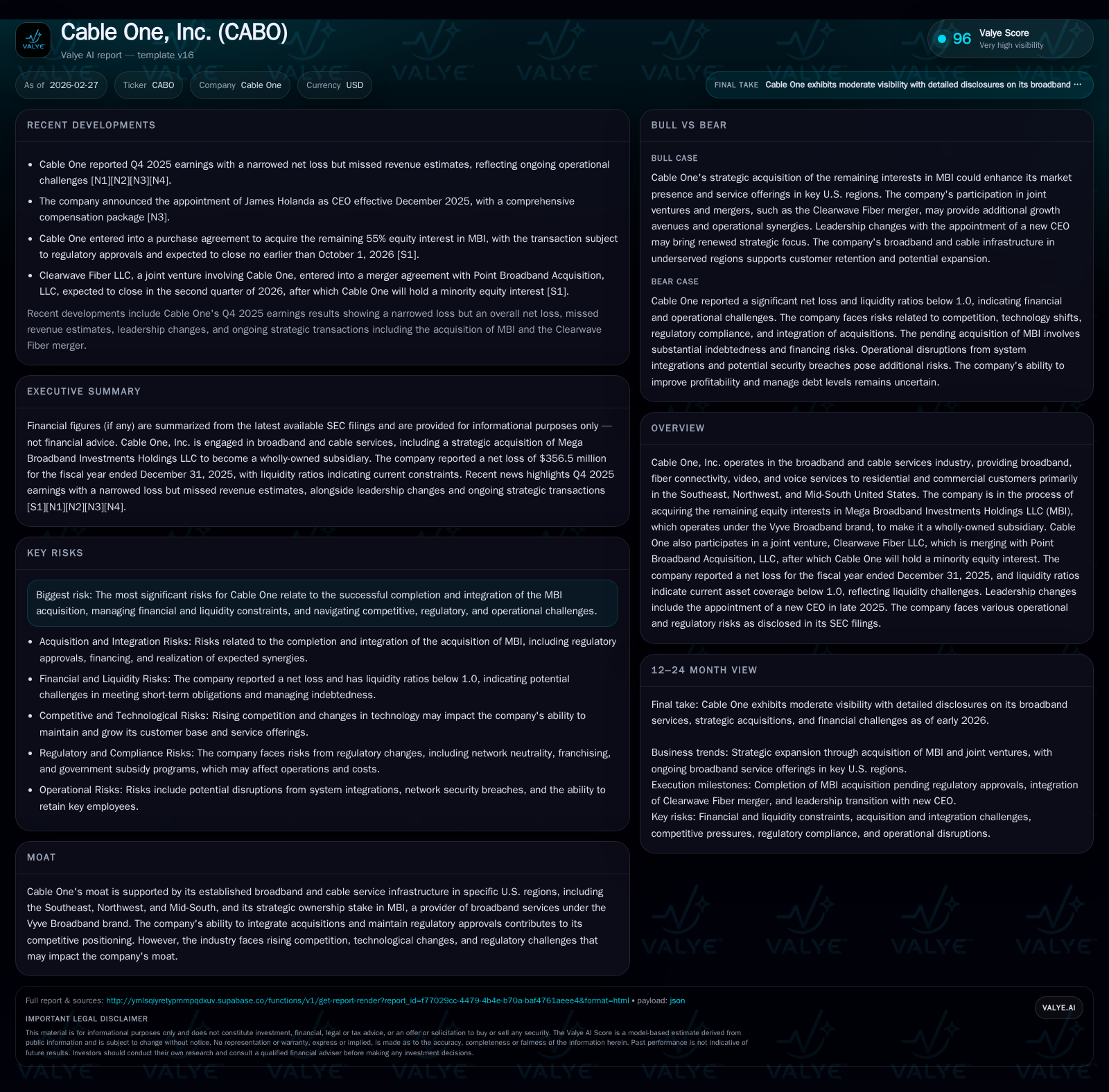

Cable One Faces Integration and Liquidity Pressures While Expanding Broadband Footprint

The company grapples with a net loss in 2025 as it pursues full ownership of Vyve Broadband, balancing growth ambitions against financial strain.

Cable One, Inc. experienced a sharp decline in profitability in fiscal 2025, posting a significant net loss after years of positive earnings, largely driven by costs related to its ongoing acquisition of Mega Broadband Investments Holdings LLC (MBI). The company’s broadband and cable services have expanded geographically through its stake in Vyve Broadband and joint ventures like Clearwave Fiber, signaling future growth opportunities. However, liquidity constraints and integration risks weigh heavily on near-term prospects. Investors should monitor the closing of the MBI transaction expected in late 2026 and Cable One’s ability to generate free cash flow while managing debt and operational costs.

Historical Performance and Key Financial Metrics

Cable One’s financial trajectory over recent years shows robust revenue growth juxtaposed with escalating profitability challenges in the latest period. From fiscal year (FY) 2017 through FY 2024, the company generally reported growing revenues alongside solid operating income and positive net income figures. In FY2017, revenue stood at roughly $258 million; by FY2024 revenues had increased materially (exact figures not provided in recent filings), corresponding with strong operating income exceeding $440 million and net income surpassing $14 million [F1].

This trend reversed sharply in FY2025, when operating income plunged nearly $650 million into the red (-$207 million) alongside a substantial net loss of approximately $356 million. Such deterioration contrasts starkly with the prior three years where operating income steadily exceeded $500 million and net income ranged up to $234 million (FY2022) before declining but remaining positive [F1].

A compact summary table illustrates core annual financial results:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -356 | 563 | -207 | 285 | -2561.7% |

| 2024 | 14 | 664 | 442 | 286 | -86.0% |

| 2023 | 103 | 663 | 527 | 371 | -55.8% |

| 2022 | 234 | 738 | 539 | 414 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 17 | 0 | 278 |

| 2024 | 68 | 0 | 378 |

| 2023 | 66 | 100 | 292 |

| 2022 | 66 | 353 | 324 |

Source: SEC companyfacts cache [F1].

Table notes: Operating income (OpInc), net income (Net), cash flow from operations (CFO), capital expenditures (Capex), dividends (Div), and share repurchases (Buybacks).

Operating cash flows remain positive despite net losses at about $563 million for FY2025 but have declined moderately from previous years (around $660-740 million range) indicating some resilience on the cash generation front [F1]. Capex spending has slightly decreased from peak levels necessary for infrastructure maintenance and expansion.

Dividend reductions reflect caution around liquidity preservation and are consistent with an absence of stock buybacks during FY2025 – both depart from prior capital return trends indicating tighter capital discipline [F1][S22][N7].

Business Overview and Strategic Context

Cable One operates primarily as a broadband and cable service provider focused on residential and commercial customers across the Southeast, Northwest, and Mid-South United States. Its core services include broadband internet access, fiber connectivity, video programming distribution, and voice services under various brand names.

A pivotal element shaping recent developments is the company’s initiative to acquire the remaining equity interests it does not already own in Mega Broadband Investments Holdings LLC (MBI), which operates under the Vyve Broadband brand. Cable One currently owns approximately a 45% interest in MBI with other ownership held by private equity interests including GTCR LLC affiliates [S12][S20].

In early January 2026, these Gwider investors exercised their put option compelling Cable One to purchase their remaining shares for an estimated price ranging between $475 million to $495 million based on adjusted EBITDA multiples as per MBI’s latest financials ending June 30, 2025 [S12][S20]. This transaction is expected to close no earlier than October 1, 2026 subject to regulatory approvals including Hart-Scott-Rodino clearance and Federal Communications Commission consent.

Completion of this acquisition will consolidate Cable One’s footprint significantly by making Vyve Broadband a wholly owned subsidiary. The deal entails assuming significant debt within MBI's capital structure – forecasted net indebtedness at closing is approximately $845–$895 million maturing November 2027 – increasing Cable One's overall leverage profile materially [S12][S20]

Cable One is also involved through its joint venture Clearwave Fiber LLC which is merging with Point Broadband Acquisition LLC; post-merger Cable One will hold a minority equity stake in the resulting parent entity Point Holdings. This move signals strategic emphasis on expanding fiber infrastructure capabilities critical for high-speed data services demand growth amid industry transformation [S17].

Industry Dynamics and Competitive Positioning

The broadband/cable sector remains intensely competitive as incumbents face pressure from alternative technologies such as wireless home internet providers alongside rapidly evolving consumer preferences favoring streaming over traditional video packages.

Cable One’s moat historically rests on its regional broadband infrastructure providing scale economies within select U.S. geographies plus strategic investments like Vyve Broadband enabling broader market presence without full acquisition risk until now. The company’s ability to successfully integrate acquisitions while navigating regulatory compliance shapes its competitive positioning going forward.

Regulatory uncertainties include potential changes related to network neutrality rules or franchise renewals whereas operational risks involve supply chain disruptions affecting equipment procurement—all material considering ongoing capex demands necessary for service upgrades [S4][S9]. Moreover, pricing pressures relating to programming costs or retransmission fees remain challenges impacting margin sustainability.

Future Growth Prospects

Growth drivers center on further penetration of broadband services fueled by rising residential internet consumption trends alongside commercial customer expansions.

Full ownership of Vyve Broadband post-acquisition offers enhanced scale advantages potential cross-selling synergies, cost rationalization benefits (once integration concludes), and a more unified billing platform rollout anticipated but currently associated with transition risks as previously disclosed [N3][S10].

Fiber infrastructure investments linked to Clearwave Fiber's merger augment long-term service capability enhancements supporting higher bandwidth demand segments albeit accompanied by capital intensity.

Risks that could cap growth include escalating competition from both legacy operators expanding gigabit cable offerings and disruptive entrants leveraging wireless technologies; additionally, failure to realize anticipated synergies or disruption from billing system integrations could impair customer experience negatively impacting retention rates [S10].

Financial Forecasts, Milestones & Capital Allocation Expectations

Explicit guidance for financial metrics has not been detailed publicly beyond transaction timing milestones.[N3][N7] Key events investors should watch are:

- Closing date of MBI remaining equity acquisition expected October 1, 2026,

- Successful regulatory approvals including HSR expiration and FCC/state commission consents by May/June timelines,

- Progress on integrating Vyve’s operations fully into Cable One’s systems,

- Completion of Clearwave Fiber merger within Q2 calendar year reportedly scheduled,

- Cash flow generation capacity relative to incremental debt servicing requirements post-acquisition.

Capital allocation has pivoted toward conserving liquidity; dividend reductions substantiate this stance while share repurchases ceased entirely during FY25.[F1][S22] Leverage metrics will require close monitoring considering additional indebtedness assumed via acquisition financing arrangements structured potentially through revolver borrowings or issuance of new instruments [S20]. Return metrics deteriorated sharply: approximate ROE turned negative circa -25%, reflecting large losses relative to equity base as per last reported period's results highlighting immediate profitability pressures absent yet offset by operational cash flows supporting investment activities.[F1]

Management Transition & Leadership Considerations

Late CY25 saw appointment of an interim CEO accompanied shortly thereafter by hiring of Mr. Holanda as permanent CEO commencing early CY26 with substantial compensation package inclusive of salary, bonuses, equity awards aiming at steering company through current strategic inflection points involving integration complexity plus operational improvements.[S23] Such leadership transitions often herald shifts toward renewed strategic focus or cultural realignment critical during distressed profitability periods coinciding with expansive M&A activity.

Conclusion: Balancing Acquisition Growth Against Financial Strain

Cable One stands at a pivotal juncture where its expansion efforts via acquiring full ownership of Vyve Broadband coupled with fiber joint ventures position it well for longer-term broadband market relevance across key U.S regions. However, these moves impose near-term financial stresses documented clearly by an outright loss position in FY25 amid liquidity constraints reflected by subpar working capital ratios. Success hinges largely on smooth execution of pending transactions especially meeting regulatory conditions timely alongside effective operational integration that realizes expected synergies without alienating customers or incurring excessive cost overruns. Investors should monitor cash flow evolution relative to debt servicing capacity given reliance on credit facilities for acquisition funding plus progress on management initiatives aimed at stabilizing profitability metrics moving forward.

Disclaimer: This report is intended solely for informational purposes based on available financial filings and industry context as of early calendar-year 2026. It does not constitute investment advice or endorsements regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments