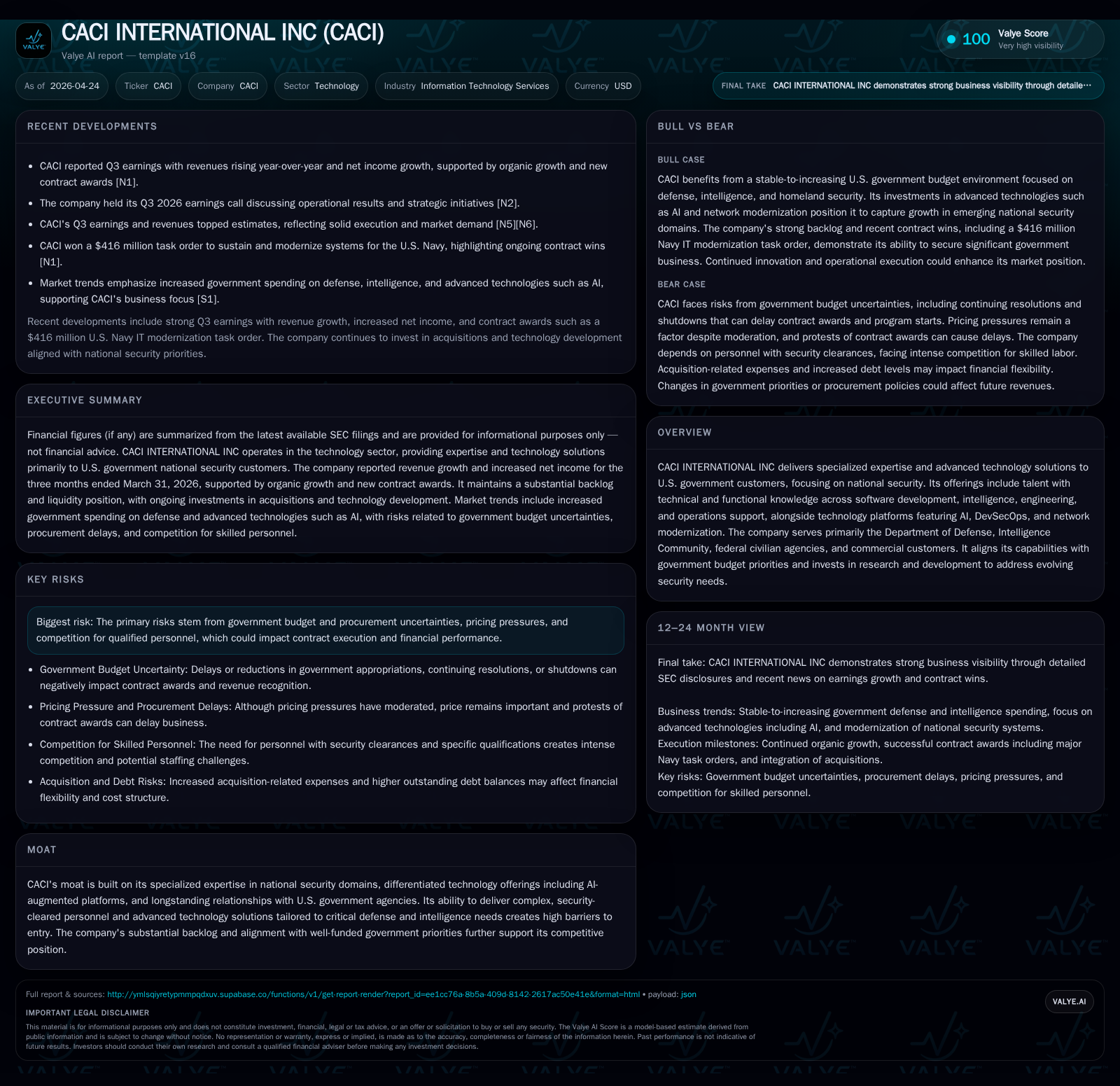

CACI International Advances Specialized National Security Solutions with Strong Q3 Momentum

Q3 fiscal 2026 results highlight CACI’s revenue growth, backlog expansion, and continued alignment with national security priorities.

CACI International demonstrated notable top-line resilience and backlog growth in its latest quarter, reinforcing its specialized position within the U.S. government IT services sector. The company’s distinct model, blending cleared technical expertise with AI-augmented technology platforms, remains closely tied to defense and intelligence budgetary trends. While operating leverage benefits margin expansion, risks from budget timing and talent scarcity persist. Financially, strong operating cash flow supports ongoing investments amid elevated leverage levels.

Latest Quarterly Update Highlights Resilient Revenue and Pipeline Strength

CACI International posted third quarter fiscal 2026 revenues of approximately $2.35 billion, marking an 8.5% increase compared to the same period last year [S2][S3][N1][N5]. This growth outpaced consensus estimates while reflecting a mix of organic expansion across core defense and intelligence customer segments combined with contributions from recent acquisitions. Significantly, the company’s total contract backlog increased by 6.4% year-over-year to $33.4 billion as of March 31, 2026 [S16][S17], underscoring a strong pipeline that enhances near-to-medium term revenue visibility.

Operating income grew at an even faster pace with a 16.6% jump over prior year quarters [S8], evidencing operational leverage benefits despite modest inflationary pressures on labor costs related to acquisition integration expenses noted in indirect cost components [S18]. The firm highlighted ongoing alignment with evolving U.S. government budget priorities amid heightened geopolitical tensions driving national security investments [S2].

Meanwhile, appropriations dynamics remain complex: continuing resolutions (CRs) occasionally delay new program starts and contract awards; however, passage of supplemental funding via reconciliation legislation (such as the One Big Beautiful Bill Act signed in mid-2025) provides additional near-term financial tailwinds beyond baseline presidential budget requests [S2][S23]. CACI management noted ongoing reviews of potential program risk exposure but expressed confidence in operating continuity due to broad bipartisan support for defense-related spending.

Business Model Focused on Expertise and Advanced National Security Technologies

CACI’s business model is deeply rooted in delivering Expertise — highly cleared personnel possessing specialized technical knowledge spanning software engineering, intelligence support operations, naval architecture, lifecycle services, and network exploitation analytics — combined with advanced Technology offerings [S1][S2]. This hybrid approach addresses unique U.S. government demands that general commercial IT providers cannot easily replicate due to stringent clearance requirements and deep domain knowledge barriers.

The company's technology stack includes DevSecOps agile software practices built around open modern architectures supporting rapid deployment cycles favored by government customers [S2]. Further enhancing value are AI-augmented data platforms for intelligence analysis, photonics technologies enabling enhanced sensor capabilities in space-based systems, sophisticated electromagnetic spectrum management tools, and network modernization solutions critical for cyber-hardened communications.

CACI's tailored contract economics contrast sharply with commoditized IT outsourcing — contracts often involve long sales cycles due to extensive vetting but benefit from durable relationships and multi-year funded backlogs [S1]. This positioning allows CACI some insulation from pricing volatility seen elsewhere while providing opportunities to upsell incrementally innovative solutions matching evolving threats.

Competitive Edges in a High-Barrier Government IT Services Market

CACI’s moat rests heavily on factors such as the complexity of obtaining security clearances for personnel alongside its track record delivering mission-critical solutions across DoD and IC spheres [S1]. Strict regulatory obstacles limit new entrants’ ability to compete effectively at scale.

Moreover, differentiated technology investments — notably sustained R&D in AI-enhanced analytics and DevSecOps agility — solidify its standing above peers reliant on legacy platforms or lower-tier contracting strategies . Long-established client relationships built over decades afford trust advantages crucial when handling classified or sensitive work.

Competition remains intense primarily among a handful of large integrators capable of managing complexity at scale; yet CACI's focus on niche domain expertise coupled with continuous innovation elevates it beyond commoditized commercial IT firms constrained by price wars or non-security-cleared workforce challenges [S1].

Top-Line Growth Drivers: Government Budget Priorities and AI-Enabled Solutions

A stable-to-increasing defense budget backdrop underpins fundamental demand growth [S2]. Bipartisan congressional support for national security initiatives drives expenditures on cyber warfare capabilities, space force enhancements including photonics sensors, electromagnetic spectrum dominance programs, and application modernization programs requiring agile software frameworks.

Beyond traditional defense spend categories, accelerated adoption of artificial intelligence for data analytics presents a compelling incremental growth vector as CACI leverages its R&D pipeline to deliver AI-augmented solutions ahead of government adoption curves [N13][S2]. This investment not only expands total addressable market but also reinforces differentiation versus competitors slower to integrate cutting-edge tech.

Federal civilian agencies’ rising cybersecurity priorities coupled with border protection initiatives financed under reconciliation bills add further diversification beyond core DoD/IC revenue streams [S8][S23].

Growth Constraints: Budget Timing, Contracting Dynamics, and Talent Competition

Despite constructive long-term outlooks driven by government funding priorities, near-term execution faces challenges arising from continuing resolutions (CRs) which temporarily freeze or delay contract awards pending appropriations approval [S2]. These governmental stopgaps introduce cyclical timing volatility affecting revenue cadence quarter-to-quarter.

Pricing pressures persist as some procurement vehicles retain lowest price/technically acceptable criteria from previous cycles; while moderated recently from peak intensity levels, pricing remains an important evaluation factor limiting margin expansion potential during highly competitive bids [S12].

Furthermore,cacis dependence on highly skilled cleared personnel faces supply-side constraints given intense competition across industry peers for scarce cybersecurity experts and engineers who meet security clearance thresholds and possess requisite domain experience [S2]. Retention efforts must balance cost control against talent scarcity premiums.

Key Execution Metrics and Upcoming Milestones to Monitor

Investors should gauge trajectory via several near-term indicators including backlog evolution — any sequential expansion or contraction provides insight into new wins versus revenue recognition patterns inherent to multiyear contracts [S17][S23]. Speed of converting funded backlog into billings reflects operational execution health amid shifting government priorities.

Watch contracting award announcements post-CR resolution phases particularly within cyber modernization and emerging AI-centric initiatives requested under the Golden Dome initiative embedded within supplemental funding packages [N2][S23].

Talent acquisition success rates coupled with attrition trends among cleared technical staff will impact capacity utilization metrics influencing deliverables quality plus margin sustainability.[N2]

Legislative developments around GFY26-finalized appropriations or further reconciliation funding additions present critical external catalysts shaping fiscal outlooks beyond baseline scenarios detailed in recent filings.[S23]

Financial Position Reflecting Strong Operating Cash Flow Amid High Leverage

As of March 31, 2026, CACI reported cash & equivalents totaling approximately $158 million contrasted against total debt outstanding near $5.21 billion resulting in net debt around $5.05 billion; the current ratio stood at a healthy 1.61 indicating sufficient short-term liquidity coverage [F1].

Operating income increased roughly 16.6% YoY through nine months ended March 31 demonstrating improving profitability trends consistent with revenue growth dynamics [F1][S8]. Net income exhibited a solid double-digit rise reflecting operating leverage benefits despite modest interest expense increases linked to debt balances accrued for acquisitions executed recently including ARKA Group L.P.[F1][S21]

Operating cash flow generation remained strong at about $547 million in the previous fiscal year supporting capital expenditure levels just below $66 million annually plus enabling disciplined strategic acquisitions without immediate equity dilution pressures[F1].

Selected Financials Summary Table:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 500 | 547 | 764 | 66 | +19.0% |

| 2024 | 420 | 497 | 650 | 64 | +9.1% |

| 2023 | 385 | 388 | 568 | 64 | +4.9% |

| 2022 | 367 | 746 | 496 | 75 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 169 | 481 | |

| 2024 | 161 | 434 | 11.9 |

| 2023 | 273 | 324 | 11.9 |

| 2022 | 10 | 671 | 12.0 |

Source: SEC companyfacts cache [F1].

- FY25 revenue is trailing twelve months estimated via quarterly aggregation

The financial profile reflects steady top-line progression buffered by prudent cost management despite acquisition-related expenses reflecting disciplined capital allocation within the government services sector environment.[F1]

This analysis is based solely on publicly available information as of April 24, 2026 and does not constitute investment advice or recommendations regarding securities of CACI International Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments