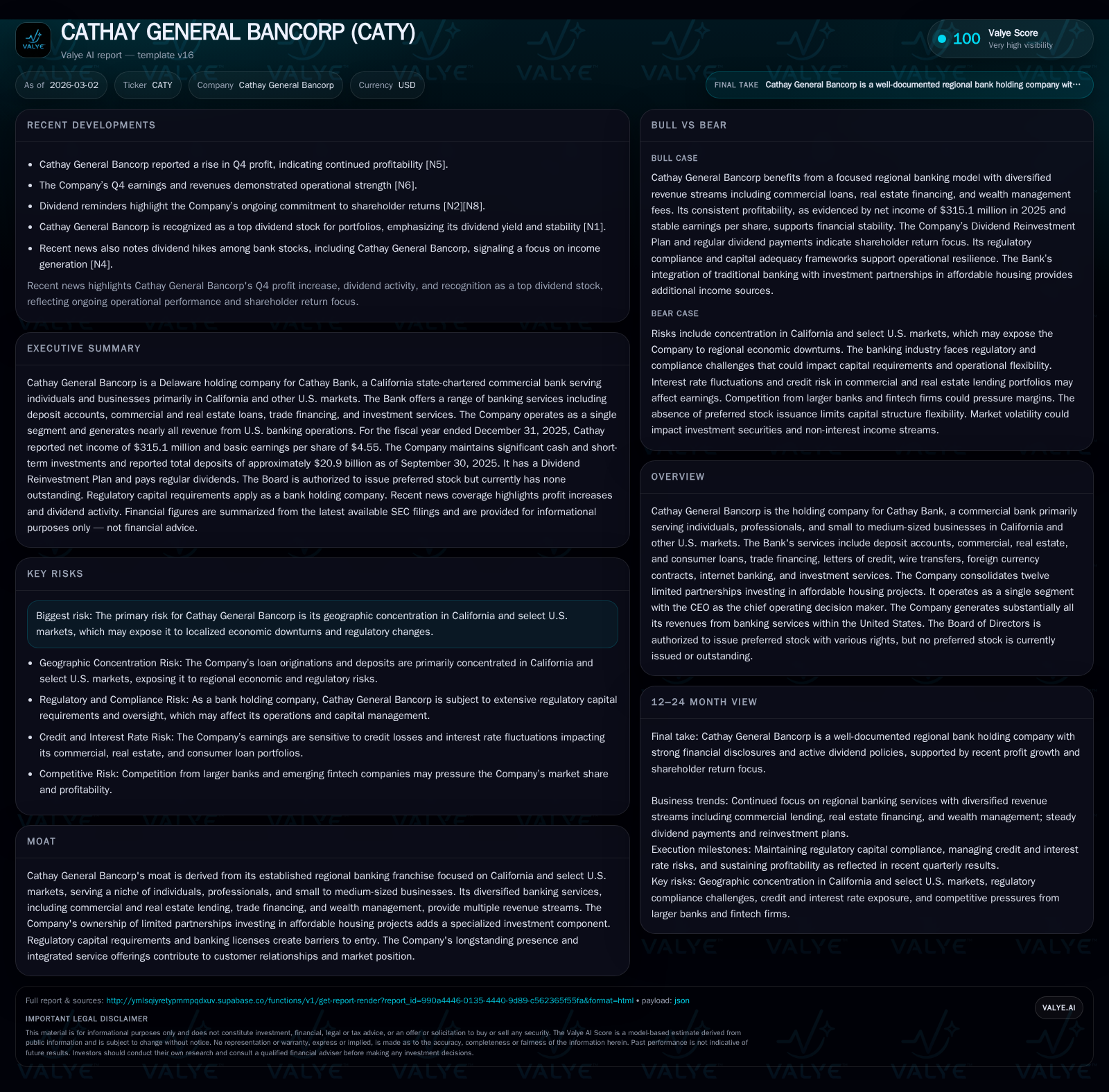

CATHAY GENERAL BANCORP’S Earnings Momentum and Capital Allocation Signal Resilience in Regional Banking

Cathay General Bancorp demonstrates sustained earnings growth and disciplined capital deployment anchored in its California-centric niche banking.

Cathay General Bancorp has reported a 10.2% increase in net income for FY2025, driven by strong performance in its commercial and real estate lending portfolios. The company leverages its deep regional expertise in California’s diverse markets to offer a range of banking services tailored to individuals and SMEs. Its capital allocation strategy balances dividend payments with an accelerated share repurchase program, supporting shareholder returns while maintaining solid equity. Robust risk grading frameworks underpin portfolio quality, complemented by an experienced cybersecurity governance structure bolstering operational resilience amid evolving threats.

Steady Earnings Growth Driven by Niche Commercial and Real Estate Lending

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 315 | 369 | 5 | +10.2% |

| 2024 | 286 | 329 | 4 | -19.2% |

| 2023 | 354 | 385 | 3 | -1.8% |

| 2022 | 361 | 467 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 94 | 180 | 364 |

| 2024 | 98 | 85 | 326 |

| 2023 | 99 | 17 | 381 |

| 2022 | 101 | 141 | 464 |

Source: SEC companyfacts cache [F1].

Cathay General Bancorp's financial trajectory through FY2025 showcases steady earnings expansion paced by its specialized lending activities. The holding company generated net income of $315.1 million for the fiscal year ending December 31, 2025, representing a healthy 10.2% increase compared to $286 million earned in the prior year [F1]. This upward momentum is attributed primarily to robust performance within commercial loans and commercial real estate financing segments, which constitute core components of Cathay Bank’s portfolio.

The bank's ability to sustain revenue streams from trade financing activities, letters of credit issuance, along with consumer and small business loans, contributed incrementally to non-interest income diversification. Additionally, operating cash flow registered an increase of 12% year-over-year to about $368.6 million, illustrating effective cash generation capacity despite modest capital expenditures totaling approximately $4.9 million (up 35% YoY) as Cathay invests prudently in technology and facilities maintenance [F1], [N1], [N7].

This consistency aligns with the bank’s niche positioning serving California-based individuals and small- to medium-sized enterprises (SMEs), reinforcing stable client engagement that underpins predictable fee income profiles.

Strategic Footprint Focused on California’s Diverse Market Needs

Operating predominantly within California and select U.S. markets, Cathay leverages nuanced understanding of regional dynamics to tailor its banking products for distinct customer cohorts including professionals, entrepreneurs, and SMEs involved in real estate development and commerce.

The company's regional specialization translates into a concentrated but strategically sound footprint where it navigates benefits such as established market presence and customer loyalty against inherent risks from local economic or regulatory fluctuations , [S5]. For example, half or more of lending commitments are rooted in commercial real estate—a sector historically sensitive to shifts in vacancy rates and construction activity—but Cathay's underwriting discipline cushions credit exposure.

Further emphasizing this approach is Cathay's utilization of trade finance instruments like letters of credit facilitating both domestic and cross-border transactions vital for businesses entrenched in the Californian export-import supply chains.

Dividend Consistency and Share Buybacks: Tailoring Returns for Income Investors

Maintaining appeal for income-focused shareholders, Cathay General Bancorp continued its track record of dividend payments totaling approximately $93.8 million in FY2025, slightly down from nearly $98 million in FY2024 but consistent with an unchanged dividend per share of $1.36 annually [F1], [N3], [N4], [N6]. This steadiness reflects the Bank's commitment to shareholder income stability even amid moderate variability in earnings.

Simultaneously, the bank markedly accelerated its share repurchase program with buybacks expanding more than twofold year-over-year from $84.7 million in FY2024 to $180.3 million in FY2025—a strategic deployment aimed at reducing share count and enhancing per-share value metrics while flexibly managing capital resources in compliance with regulatory constraints [F1], [N4].

Balance between dividends and buybacks highlights a calibrated capital return policy sensitive to both investor preferences and capital adequacy requirements.

Balance Sheet Strength: Loan Portfolio Quality and Liquidity Positioning

Cathay General Bancorp manages its loan book through a rigorous risk grading matrix that segments credits into categories ranging from Pass/Watch (minimal or acceptable risk) to Special Mention (borrowers showing adverse trends yet viable repayment sources) and further into substandard tiers when weaknesses could jeopardize repayment prospects [S7]. As of December 31, 2025, there were no modified loans under distress nor significant delinquency flagged in the portfolio documentation.

The loan portfolio encompasses sizable proportions locked in residential mortgage lines alongside commercial real estate loans aggregated around $15 billion pledged under blanket lien programs facilitating liquidity access through Federal Home Loan Bank arrangements—a testament to prudent collateralization practices [S9], [S20].

Deposits extended robust support with total balances exceeding $20 billion by year-end 2025 providing stable funding sources; key deposit segments included time deposits amounting close to $9.7 billion complemented by demand deposits bearing competitive yields across money market accounts and NOW deposits ensuring transactional flexibility for diverse clientele groups.

Liquidity reserves allowed for nimble responses to unforeseeable market stress events without compromising operational continuity.

Capital Allocation Framework Underlining Sustainable ROE Above 10%

Cathay’s capital management framework sustains profitability with an approximate return on equity calculated at 10.8% for FY2025 based on net income relative to shareholders’ equity approximating $2.93 billion at fiscal year-end—a reputable metric among mid-sized regional banks balancing growth aspirations alongside regulatory capital maintenance obligations [F1],[S29].

Free cash flow generation remains robust given operating cash flows consistently outpace benign capital expenditures resulting in about $364 million annual free cash flow available for corporate initiatives including dividends distributions or share repurchases.

Indeed, the firm exercised measured discretion increasing stock buybacks while retaining dividend levels steadily aligned with historical payout ratios underscoring a philosophy embedding sustainable shareholder remuneration amid evolving economic cycles.

Cybersecurity Governance and Risk Mitigation as Competitive Moat Enhancers

Cyber resilience constitutes a critical dimension of Cathay's operational risk strategy overseen by a seasoned Chief Information Security Officer (CISO) who orchestrates enterprise-wide cybersecurity frameworks encompassing preventative controls alongside incident detection, mitigation protocols reporting directly to executive risk committees including the Board-level oversight committee [S1].

Such governance rigor reflects best practices essential within financial institutions given their data sensitivity and regulatory scrutiny intensity. The CISO’s background combining over 25 years of experience—both military service and senior security leadership roles—provides credibility underpinning Cathay’s defense posture against escalating cyber threats impacting banking infrastructure nationwide.

This integrated security architecture enhances trust among clients reliant on uninterrupted transactional capabilities supporting continuous revenue streams.

What to Watch: Loan Portfolio Composition and Geographic Concentration Risks

While Cathay’s focused footprint affords tangible competitive advantages nurtured over decades, it inherently concentrates exposure predominantly within California posing vulnerability linked to localized economic downturns or tightening regulatory environments affecting important sectors like commercial real estate development or SME financing conditions as highlighted in the company's regulatory filings , [S5].

Future monitoring should target potential shifts in loan composition toward higher-risk categories or increased reliance on contingent liquidity lines which could signal early credit stress points requiring proactive mitigation.

Additionally, macroeconomic developments such as changes in interest rate policy impacting borrowers’ debt servicing costs or housing market volatility could translate into credit quality fluctuations necessitating careful surveillance.

Careful navigation through these headwinds coupled with ongoing disciplined underwriting will remain pivotal determinants shaping Cathay General Bancorp's forward earnings trajectory.

Disclaimer: This report is prepared solely for informational purposes reflecting facts disclosed by Cathay General Bancorp through filed reports and publicly available news sources as of March 2, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments