Commercial Bancgroup’s Hybrid Growth Strategy Drives Regional Banking Success

Commercial Bancgroup, Inc. combines its strong community banking presence and newly public status to grow through strategic acquisitions and organic expansion in select Southeast markets.

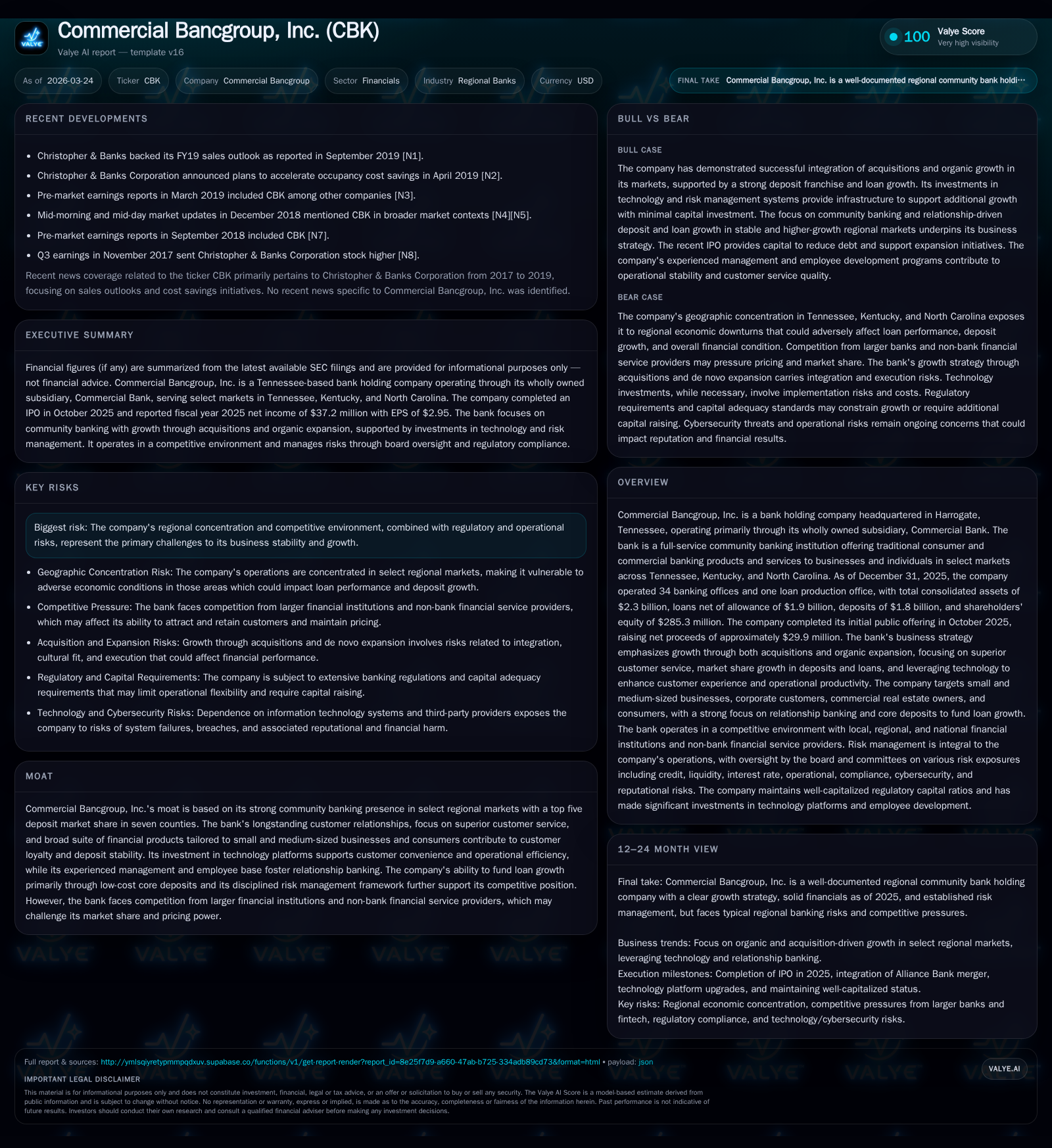

Commercial Bancgroup, Inc. closed 2025 with solid financial results highlighted by $37.2 million in net income and a 13% return on equity, supported by a $2.3 billion asset base primarily funded through stable core deposits. The October 2025 IPO raised nearly $30 million in net proceeds, which were largely deployed to retire holding company debt, enhancing capital flexibility for growth initiatives. The bank's growth strategy balances acquisitive expansion—exemplified by the 2024 Alliance Bank merger—with organic growth across Tennessee, Kentucky, and North Carolina markets where it holds top five deposit market shares in key counties. Investments in technology platforms like Jack Henry support operational scalability and customer experience. Key risks include regional economic concentration, competitive pressures from larger banks and fintechs, interest rate sensitivity, and regulatory compliance costs. Capital management remains conservative with a focus on maintaining well-capitalized status and a disciplined dividend policy.

Heritage and Historical Growth Drivers: Building on Community Strengths

Commercial Bancgroup traces its roots to a community bank chartered in Tennessee in 1976. Its footprint encompasses key metropolitan statistical areas (MSAs) including Nashville-Davidson–Murfreesboro–Franklin, Knoxville, Tri-Cities (Johnson City, Kingsport-Bristol), parts of Southeast Kentucky such as Barbourville and Harlan, alongside a recent expansion into North Carolina’s Charlotte-Concord-Gastonia MSA via the Alliance Bank acquisition. This regional mix balances urban growth centers with stable rural economies fostering durable client relationships.

The bank holds top five deposit market shares in seven counties across these states serving small to medium-sized businesses (annual revenues up to $300 million), owner-occupied commercial real estate borrowers, and retail consumers utilizing mortgage products or home equity lines. This client base supports a low-cost funding structure with approximately 91.6% core deposits excluding brokered or large time deposits as of December 31, 2025 [S6][S23]. Such stability enables loan-to-deposit ratios exceeding 100%, facilitating measured balance sheet growth.

Organic growth is driven by relationship-based lending practices consistent with community banking ethos sustained through its network of 34 branches plus one loan production office.

2025 Performance Snapshot: Financial Results and Operational Highlights

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

(Source: SEC filings consolidated data snapshot) [F1][S1]

The year featured robust earnings despite macroeconomic challenges including interest rate volatility impacting fixed-income portfolios but not materially affecting profitability or capital adequacy.

Net income of $37.2 million generated an approximate return on equity of 13%, reflecting effective equity utilization while producing about $35 million free cash flow after capital expenditures.

Proceeds from the October 2025 IPO totaling roughly $29.9 million net were principally used to retire outstanding holding company debt ($20.5 million), reducing leverage at the parent level and positioning the company for continued growth [S1][S3].

Growth Strategy: Balancing Acquisition with Organic Expansion

The bank follows a hybrid growth approach combining strategic acquisitions with organic market development.

The July 2024 merger with Alliance Bank & Trust Company expanded Commercial Bancgroup’s presence into North Carolina’s Charlotte MSA including branches in Shelby, Kings Mountain, Gastonia and an LPO in Lincolnton—a market noted for its economic dynamism.

Integration has proceeded without material disruption though disclosures highlight typical acquisition risks such as cultural fit challenges or cost overruns during consolidation phases [S7].

Organic initiatives focus on deepening credit relationships within existing MSAs where customer loyalty supports cross-selling commercial loans over $2 million alongside treasury management services incorporating remote deposit capture technology [S6][S23].

Management intends to pursue selective acquisitions and de novo expansions targeting adjacent markets aligned with existing capabilities while preserving asset quality and shareholder value [S23].

This balanced model facilitates asset growth while enhancing technological infrastructure critical for scalable operations without compromising community banking culture.

Market Footprint and Competitive Positioning

Operating primarily across Tennessee, Kentucky, and North Carolina provides geographic diversity but also concentrates exposure to regional economic conditions:

- Urban centers like Nashville enable access to corporate clients requiring sophisticated financial solutions.

- Knoxville and Tri-Cities offer steady consumer deposit bases amid smaller metropolitan populations.

- Southeast Kentucky serves largely rural communities supported by small businesses often underserved by larger banks.

- Charlotte MSA represents a high-growth area benefiting from urban expansion trends [S4][S6].

Competition includes local community banks targeting similar niches; larger regional/national banks leveraging scale for aggressive pricing; credit unions appealing via fee advantages; and fintech firms challenging transactional services though currently less impactful given Commercial Bancgroup’s relationship-driven model [S4][S22].

The bank’s comprehensive product suite spanning predominantly commercial loans (approximately four-fifths of loan portfolio), mortgages, and personal lines combined with proactive customer service reinforces competitive positioning within these markets.

Technology Investments Enhancing Efficiency and Customer Experience

Strategic investments target both front-end client interfaces and back-office productivity gains.

Utilization of Jack Henry & Associates’ core banking platform provides scalable processing capacity supporting increased transaction volumes triggered by geographic expansion or loan/deposit growth [S6].

Customer-facing digital channels include mobile apps offering functionality comparable to larger institutions while cybersecurity protocols safeguard sensitive data amidst heightened cyber threats.

Internal workflow automation reduces manual errors and accelerates reporting enhancing risk controls while freeing bankers for client engagement—strengthening relationship banking fundamentals vital for retention [S6].

This technology balance between innovation adoption and personalized service sustains relevance against fintech disruptors and traditional banks alike.

Regulatory Environment and Risk Management Framework

Commercial Bancgroup operates under extensive federal and state regulations impacting operational costs and strategic options:

- Classified currently as a “small bank holding company,” it is exempt from consolidated Federal Reserve capital requirements but may face expanded oversight if assets exceed $3 billion or nonbank activities increase [S10][S15].

- Maintaining “well capitalized” status at the Bank level is essential to avoid restrictions on brokered deposits or dividends—a standard actively maintained [S24].

- Concentration risks arise from geographic focus coupled with sector exposures including owner-occupied commercial real estate loans comprising roughly one-quarter of CRE portfolio; hospitality sector exposures occasionally breach internal limits raising vulnerability to local economic shocks [S26].

- Interest rate fluctuations can cause unrealized losses on securities portfolios; rising deposit rates driven by competition can compress net interest margins impacting profitability if unmanaged [S1][S5].

- Compliance obligations span consumer protection laws affecting underwriting practices requiring ongoing training and system controls mitigating legal risks [S14][S19].

- Cybersecurity forms a critical component of risk management featuring regular testing layered defenses overseen at Board level [S23].

Overall risk architecture aims for timely threat identification preserving capital resilience typical of regional community banks.

Capital Allocation: IPO Proceeds Deployment and Shareholder Returns

The October 2025 IPO provided approximately $29.9 million net proceeds used mainly ($20.5 million) to retire holding company debt owed to Community Trust Bank promptly post-offering [S1][S3].

A conservative dividend policy has been adopted with quarterly dividends declared since early 2026; most recently $0.10 per share payable March end—supported by earnings largely derived from subsidiary dividends reflecting bank profitability [F1][S27]. No share repurchase programs have been disclosed indicating focus on balance sheet strengthening rather than capital return through buybacks.

This approach supports reported ROE near 13%, balancing profitability reinvestment aligned with measured growth objectives while maintaining liquidity buffers evidenced by approximately $144 million cash equivalents at year-end [F1]. By avoiding excessive leverage yet investing strategically in technology alongside selective acquisitions, management seeks long-term value creation consistent with articulated risk appetite.

Such stewardship underscores commitment to institutional safety mandated by regulators while delivering incremental shareholder value amid regional franchise expansion.

Forward-Looking Considerations for Investors

Key factors warranting attention include:

- Successful integration post-Alliance Bank acquisition ensuring synergy realization without asset quality deterioration or shareholder dilution risks inherent to mergers

- Maintenance or enhancement of satisfactory Community Reinvestment Act (CRA) ratings critical for preserving branch opening or acquisition flexibility supporting inorganic growth avenues

- Ability to grow deposit bases amid competitive pressure from larger banks leveraging scale pricing advantages alongside fintech entrants potentially eroding traditional deposits requiring innovation balancing price versus service differentiation

- Management of interest rate environment impacts influencing net interest margin spreads necessitating calibrated pricing strategies minimizing attrition while sustaining margin health amidst macroeconomic volatility expected mid-decade

- Adaptation to evolving regulatory frameworks potentially increasing compliance costs demanding operational efficiencies supported by technology investments alongside proactive regulatory engagement developed over recent years’ complex environment post-Dodd Frank reforms continuation outlasting varied administration policies including potential CBLR adjustments proposed nationally for community banks

- Strategic discipline regarding selective acquisitions balancing accretive benefits against integration complexities determining optimal pace of scaling without compromising returns historically yielding above-peer ROEs among comparable Southeastern regional banks servicing similar demographics

Monitoring these alongside broader macroeconomic indicators such as regional GDP trends and employment stability within core MSAs can provide directional insights into future performance trajectories underpinning valuation narratives grounded firmly upon fundamental operating results.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments