Ceribell's Profitability Challenges Amid Rapid Growth and Competitive Pressures

Ceribell, Inc. faces a critical juncture balancing operational expansion, intensifying lawsuits, and constrained profitability.

Since launching commercial sales in 2018, Ceribell has expanded rapidly with its AI-enabled rapid EEG system in acute care settings, backed by FDA clearances and patents. Despite robust top-line growth trends implied by increased headcount and investments, the company remains unprofitable with widening operating losses and negative cash flow in latest fiscal years. Key growth drivers include expanding hospital adoption and subscription revenues for its wearable EEG headbands combined with cloud analytic platform. Yet, significant challenges loom from manufacturing scale-up, ongoing patent litigations, reimbursement uncertainties, regulatory compliance complexities, and entrenched competition from legacy EEG providers. Monitoring quarterly financials for inflection towards operating leverage and progress on patent litigation outcomes will be essential to assess long-term viability.

Company Background and Product Offering

Ceribell, Inc., established in 2014 and commencing sales in 2018, specializes in rapid electroencephalogram (EEG) monitoring technology tailored for acute care environments like hospitals [N1][S1]. The Ceribell System integrates wearable EEG headbands with a recorder device and a cloud-based portal that leverages AI algorithms to accelerate seizure detection and other neurological assessments. Multiple FDA clearances for both hardware (recorder and headband) and software components have been secured since initial approvals in 2017–2019 [S1]. Proprietary headband designs are covered by patents, underpinning a moat premised on faster accessibility of neurological monitoring relative to conventional stationary EEG systems.

Historical Performance

Exact annual revenues are not disclosed in the available XBRL data [F1]. However, Ceribell has experienced rapid organizational scaling alongside increasing headcount topping 300 employees as of end-2025 [S1], reflecting progressive adoption primarily within US hospitals via subscription-based recurring revenue models.

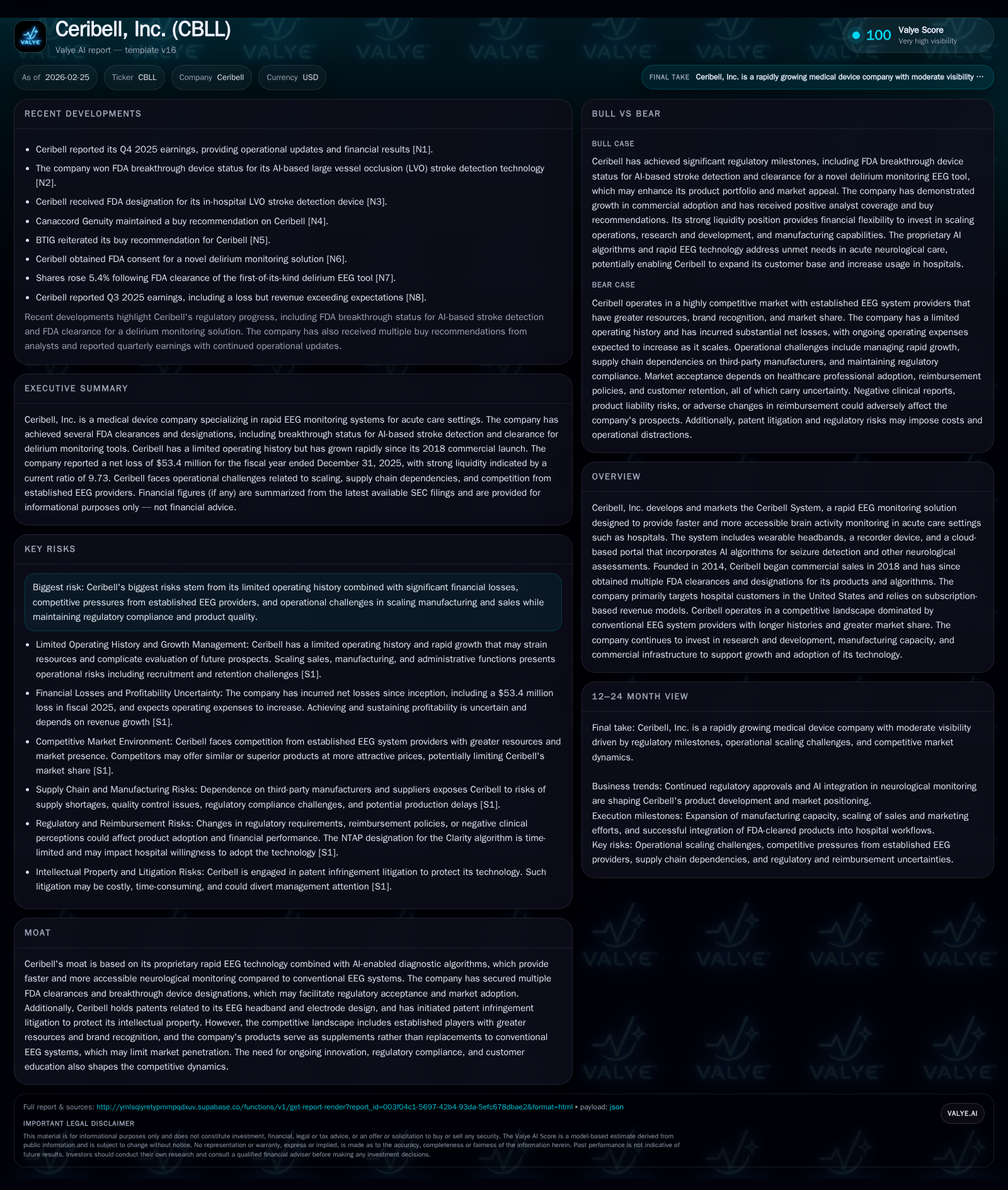

Operating results show persistent unprofitability with operating losses increasing approximately 47% year-over-year to $58.4 million in FY2025 from $39.7 million in FY2024 [F1]. Net losses widened by about 32% YoY to $53.4 million last fiscal year. This corresponds to an approximate return on equity (ROE) of -34%, highlighting capital-consuming expansion without near-term profitability [F1]. Operating cash flow declined roughly 16% YoY to a negative $40.8 million, resulting in free cash flow (operating cash flow minus capex) of approximately -$41.6 million after accounting for reduced capital expenditures [F1].

Capital investments decreased by about 43% YoY to $0.77 million in FY2025, focusing on optimizing manufacturing capacity rather than expanding physical assets during emphasis on scaling commercial distribution [F1].

The balance sheet shows strong liquidity supported by $40.5 million cash reserves at year-end FY2025, supplemented by a venture loan facility with $20 million principal outstanding that imposes restrictive covenants limiting certain corporate actions including dividends and stock repurchases [S4][S9]. Current assets of $186.7 million against current liabilities of approximately $19.2 million yield a current ratio around 9.73x, indicating solid short-term financial flexibility despite ongoing cash burn [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -53 | -41 | -58 | 767000 | -32.0% |

| 2024 | -40 | -35 | -40 | 1340000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -42 | -34.4 |

| 2024 | -36 | -21.2 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures unavailable; Dividends and stock buybacks not reported or disclosed.

Growth Prospects

Ceribell aims to drive growth through broader hospital adoption of its wearable EEG devices combined with subscription services delivering continuous neurological analytics via cloud platforms [N1][S1]. Potential product enhancements improving AI diagnostic accuracy or geographic expansions may further support this trajectory.

However, the company's products currently complement rather than replace traditional EEG systems, which may limit rapid market share gains given entrenched clinical practices.

Growth is also contingent on favorable reimbursement policy developments for remote EEG interpretation amid evolving U.S healthcare payment landscapes characterized by cost containment efforts and prior authorization requirements [S15][S23]. Regulatory milestones such as new FDA clearances or breakthrough device designations could influence commercialization pace.

Competitive pressures persist due to legacy players' extensive sales networks and brand recognition [S6][S14], while ongoing patent infringement litigation adds uncertainty around intellectual property protection and potential licensing costs or injunction risks if rulings are unfavorable [S10][S16][S19].

Forecasts and Milestones

No explicit forward-looking revenue guidance or milestone timelines are provided in the available disclosures [N1][S1]. Investors should monitor quarterly earnings for signs of improved operating leverage, sales conversion metrics post-clinical validation efforts, receivables management under payer adjustments, and updates on patent litigation outcomes.

Returns and Capital Allocation

Ceribell is currently not generating shareholder returns through dividends or share buybacks; such data are not available from filings [F1]. The company is focused on allocating capital toward R&D product development alongside manufacturing capacity enhancements aligned with anticipated volume growth [N1][S1].

Liquidity appears sufficient entering calendar year 2026 but is subject to constraints imposed by the $20 million venture loan facility's covenants restricting dividends, repurchases, asset sales, additional indebtedness, mergers/acquisitions, and affiliate transactions [S4][S9].

Industry Context Analysis

The EEG market traditionally relies on bulky stationary equipment operated by trained technicians causing diagnostic delays; Ceribell's rapid wearable EEG system with AI analytics aims to disrupt this paradigm by enabling faster neurological event detection especially in emergency settings.

Widespread adoption requires overcoming clinical inertia among neurologists accustomed to established methods along with payer reimbursement realignments favoring innovative point-of-care diagnostics amid U.S healthcare cost containment initiatives.

Risks Summary

Ceribell's limited operating history combined with escalating losses pose risks related to managing rapid growth including manufacturing scale-up complexities, workforce expansion challenges, quality assurance under stringent FDA regulations, cybersecurity obligations linked to cloud data handling [S1][S26].

Patent infringement litigation presents additional legal risks potentially diverting management attention while imposing unpredictable expenses or operational constraints if adverse rulings arise [S10][S16][S17][S19].

Volatility risk exists due to shifting reimbursement landscapes marked by increased scrutiny of coding/billing practices potentially affecting claim approvals or recoupments which could dampen customer adoption rates [S15][S23][S25].

Compliance burdens related to Anti-Kickback statutes, False Claims Act provisions, HIPAA privacy/security standards remain resource-intensive but critical to mitigate penalties or reputational harm [S6][S8][S25].

Conclusion

Ceribell stands at a strategic inflection point where proprietary rapid EEG wearables combined with AI diagnostics offer disruptive potential within acute neurological monitoring dominated historically by legacy incumbents. Significant execution risks remain spanning operational scaling efficiencies, regulatory/reimbursement navigation complexity, IP defense amidst active litigation exposure, and achieving profitability amid heavy R&D/sales investments. Careful monitoring of forthcoming quarterly financial results alongside patent litigation developments will be vital to assess prospects for translating technological innovation into sustainable commercial success.

Disclaimer: This analysis is presented for informational purposes only without any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments