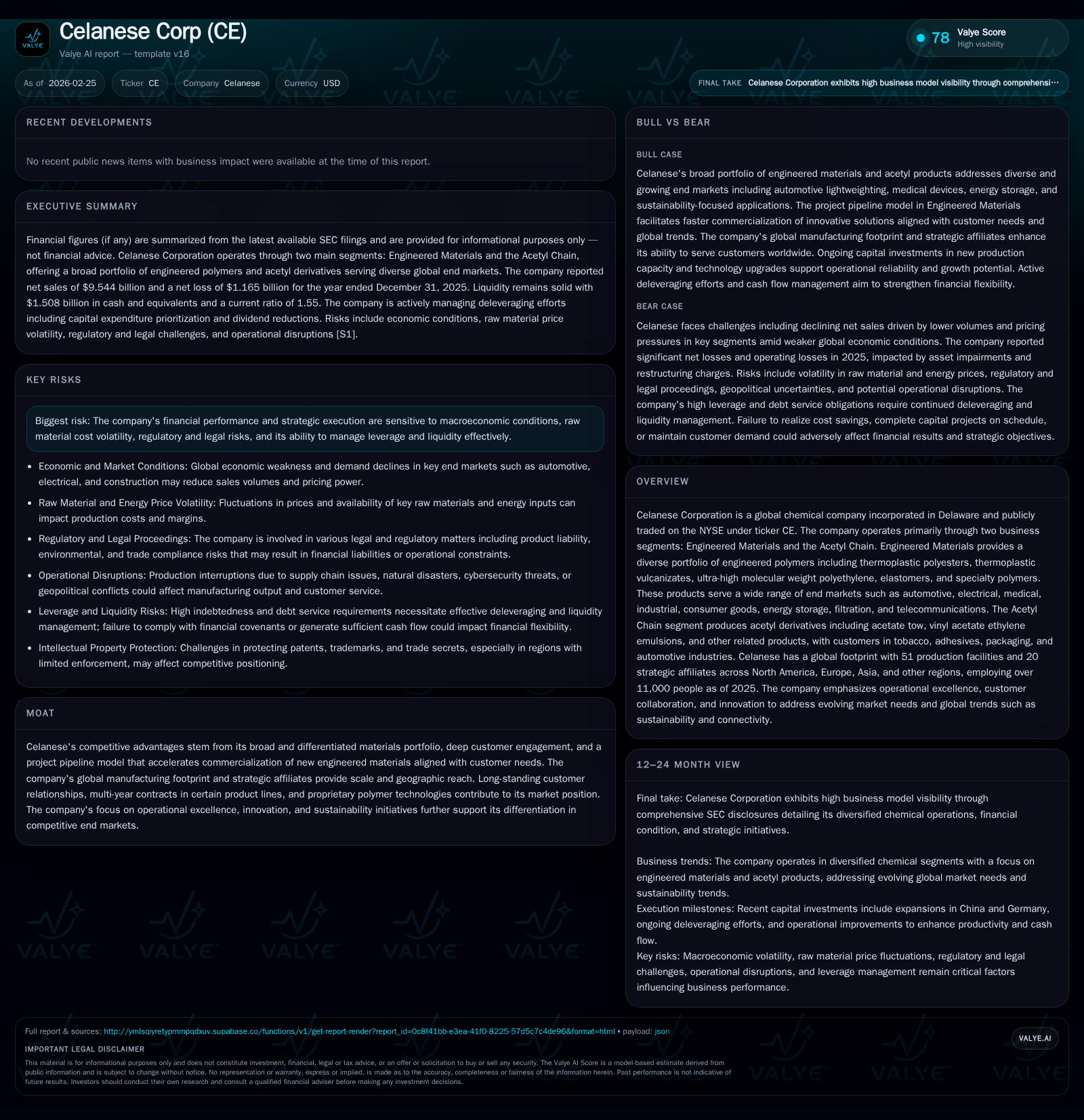

Celanese Faces Growth Ceiling Amid Profitability Challenges and Deleveraging Efforts

The global chemical company wrestles with declining sales, negative earnings, and leverage constraints, balancing expansion plans with capital discipline.

Celanese Corporation experienced a notable downturn in financial performance in 2025, evidenced by declining revenues and persistent operating losses across its Engineered Materials and Acetyl Chain segments, driven by weaker economic conditions and competitive pressures. Despite this, the company maintains substantial operational cash flow and pursues targeted capital investments to support select growth initiatives. Its near-term outlook centers on navigating economic headwinds while addressing leverage covenant challenges through deleveraging and cost-efficiency programs. Monitoring revenue recovery, margin stabilization, and successful capital allocation will be key milestones for validating strategic execution.

Company Overview

Celanese Corporation operates as a global chemical enterprise organized into two main business segments: Engineered Materials and the Acetyl Chain [S1]. The Engineered Materials segment offers specialty polymers including thermoplastic polyesters, vulcanizates, ultra-high molecular weight polyethylene, elastomers, and other proprietary materials aimed at diversified industrial end markets such as automotive, electrical equipment, medical devices, energy storage, filtration, telecommunications among others. Complementing this is the Acetyl Chain segment focusing on acetyl derivatives like acetate tow used predominantly in tobacco filtration as well as vinyl acetate ethylene emulsions catering to adhesives and packaging industries [S1]. The company maintains a substantial manufacturing footprint with 51 production facilities globally supporting its complex supply chain demands.

Historical Financial Performance

Celanese experienced significant challenges during the fiscal years 2024 and 2025 after several years of solid profitability. Operating income shifted from positive territory in 2023 ($1.69 billion) to losses of $697 million and $786 million in 2024 and 2025 respectively – a roughly 12.8% worsening year-over-year from 2024 to 2025 [F1]. This deterioration resulted primarily from reduced volume caused by weaker global economic activity coupled with downward pricing pressure driven by intense market competition across most product lines [S1]. Negative operating margins – approximately -17.8% for Engineered Materials and -19.9% to 12.7% for the Acetyl Chain — further reflect squeezed profitability [S1].

Net income mirrored this trend with substantial losses reaching -$1.52 billion in 2024 and improving slightly but remaining negative at -$1.17 billion in 2025 [F1]. These results reflect the impairment charges related to goodwill/trade name assets as well as severance costs that partially abated from their peak in 2024. Currency effects were mildly favorable due mainly to a stronger euro relative to the U.S. dollar which cushioned revenue declines modestly [S1].

Despite earnings headwinds, the company preserved robust operating cash flow (CFO), generating $967 million in 2024 increasing by nearly 19% year-over-year to approximately $1.15 billion in 2025. When factoring capital expenditures that decreased from $435 million in 2024 to $343 million in 2025 (down over 21%), Celanese posted free cash flow near $803 million for the latest fiscal year [F1]. This divergence between earnings and cash generation highlights effective working capital management and ongoing operational efficiencies achieved partly via synergy realization efforts.

Compact Financial Summary

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1165 | 1146 | -786 | 343 | +23.5% |

| 2024 | -1522 | 966 | -697 | 435 | -177.7% |

| 2023 | 1960 | 1899 | 1687 | 568 | +3.5% |

| 2022 | 1894 | 1819 | 1378 | 543 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 13 | 803 | |

| 2024 | 307 | 0 | 531 |

| 2023 | 305 | 0 | 1331 |

| 2022 | 297 | 17 | 1276 |

Source: SEC companyfacts cache [F1].

Business Segment Performance Details

Engineered Materials: Net sales declined by about $205 million (-3.7%) from prior year due principally to lower volume attributable to weaker economic conditions globally combined with decreased average pricing influenced by competitive market dynamics and product mix shifts [S1]. Operating losses narrowed vs prior year by roughly $239 million due mainly to reduced goodwill impairments plus lower severance costs alongside benefit from raw material cost decreases and synergy-driven spending reductions totaling nearly $98 million [S1]. Depreciation lowered resulting mainly from asset retirements connected with facility shutdowns.

Acetyl Chain: This segment exhibited sharper net sales contraction of approximately $531 million (-11.1%) driven mostly by price declines reflecting supply exceeding demand and volume decreases especially for acetate tow used predominantly in tobacco filters [S1]. Operating profit fell steeply by roughly $407 million pressured by these sales headwinds combined with increased accelerated depreciation costs related to planned plant closures like the Lanaken Belgium site [S1]. Partially offsetting this were productivity improvements lowering raw material sourcing expenses.

Other Activities: Operating loss improved by around $102 million following cost containment efforts linked to synergy realization actions [S1]. A turnaround from a pension-related expense last year to pension income also contributed positively.

Future Growth Prospects

Celanese’s growth outlook hinges on several factors intrinsic to its industry positioning and external market environment:

- Growth Drivers: Continued innovation via proprietary polymer technology pipelines aligned tightly with customer needs provides potential for new engineered materials penetrating high growth end markets such as energy storage polymers or advanced medical materials . Capital projects including expansions of high-margin product plants — like liquid crystal polymer compounding scaling up at its Nanjing facility or vinyl acetate ethylene emulsion capacity extension planned at Frankfurt — could unlock incremental volume opportunities starting mid-2026 [S22]. Sustained operational excellence focusing on reducing carbon footprint through energy optimization projects may also enhance competitive positioning over time.

- Growth Constraints: Macroeconomic volatility remains a chief risk as global economic slowdown can suppress demand across automotive, industrial applications, packaging etc., while volatile raw material costs could compress margins further . Competitive pricing pressures continue affecting key product lines exacerbated by excess worldwide acetyl chain capacity leading to oversupply scenarios described recently [S10]. Regulatory compliance costs—especially evolving environmental standards—pose additional cost burdens that may cap margin recovery efforts.

- Market Dynamics: The global specialty chemical space sees accelerating emphasis on sustainability credentials pushing customers towards suppliers demonstrating green chemistry practices which Celanese has embraced but requires sustained investment commitment.

Overall growth trajectories depend on how effectively Celanese manages these tradeoffs while navigating its portfolio mix towards higher value-added engineered materials versus the more commoditized acetyl derivatives.

Forecasts / Milestones / What To Watch

Explicit forward-looking guidance is limited within public disclosures as of February 2026; however several operational milestones are scheduled or underway including:

- Completion of the liquid crystal polymer expansion at Nanjing expected H2-2026 aiming at tapping growing demand segments needing advanced polymer properties.

- First half-2026 start-up of Frankfurt VAE emulsion plant expansion aligned with anticipated market recovery signals for adhesives sectors.

- Execution progress on energy optimization project at Frankfurt's POM unit targeting emission reductions while maintaining capacity reliability.

- Monitoring leverage ratios under U.S Revolving Credit Facility covenants related to upcoming step downs scheduled commencing Q1-2026 requiring mitigation strategies such as amendments or asset divestitures [S4][S7][S17].

From an investor standpoint (analysis), tracking sequential quarterly revenue trends especially volume/price components within each segment will be critical along with margin progression indicators revealing efficacy of cost control measures versus top-line pressures.

Returns / Capital Allocation

Celanese has experienced strained profitability reflected in negative ROE approximated at -28.8% based on most recent net loss relative to equity levels as of end-2025 [F1]. Despite net losses spanning the past two years financially tangible returns remain supported by cash flows.

Operating cash flow generation was solid at $1.15 billion during FY25 implying strong underlying business cash conversion even amidst earnings volatility; after deducting capital expenditures totaling about $343 million (down substantially from prior years), free cash flow measured near $803 million marks a positive lever maintaining liquidity for strategic deployment or debt service needs [F1][S22].

Dividend distributions plummeted drastically dropping from around $307 million paid out in dividends during FY24 to just $13 million in FY25 reflecting prudent restraint consistent with deleveraging priorities under current strained profit conditions [F1][S22]. Share repurchase activity has been halted since before FY24 signaling capital preservation focus.

On debt management front:

- Company refinanced multiple term loans fully repaying March ’22 and November ’24 facilities while securing a new senior unsecured revolving credit facility worth $1.75 billion maturing in 2030 enhancing liquidity buffers although leverage covenant tightening requires continued attention [S8][S13][S20][S21].

- During FY25 substantial long-term debt repayments occurred including tender offers amounting several billions but accompanied by refinancing charges pushing total debt servicing costs higher recently.

Strategically future capital allocation emphasis remains directed towards measured reinvestment into core manufacturing expansions supportive of longer-term portfolio upgrades complemented by ongoing deleveraging via asset divestitures or enhanced cost management programs aimed at restoring margin strength [S22].

Risks Summary

Major risks impacting Celanese span macroeconomic slowdown-induced demand reduction across diversified customers globally to raw material price swings undermining margins particularly pronounced under commodity-like acetyl chain products [S10][S11][S16]. Regulatory risks include stricter environmental legislation potentially leading to higher compliance costs or forced production curtailments especially problematic for facilities located within jurisdictions enforcing aggressive emission controls such as China or Europe[S10][S16].

Litigation exposures related to product liability claims across highly regulated applications (medical devices/pharmaceuticals) add uncertainty requiring adequate insurance coverage which may not always be sufficient[S10][S11]

Further financial risk arises from tightening financing covenants tied to leverage ratios under revolving credit agreements necessitating successful mitigation steps or risk facility termination scenarios impacting liquidity [S4][S17][S19].

Conclusion

Celanese’s current phase underscores a classic industry cycle tension balancing legacy business softness amid broader economic headwinds against proactive reinvestment into advanced materials underpinning future growth aspirations. While operating profitability has been challenged significantly over recent two years leading to negative earnings and constrained returns metrics, resilient operating cash flows provide cushioning enabling ongoing capex investments focused primarily on expansions designed to exploit structural end-market opportunities such as advanced polymers tailored for electrification or sustainable packaging applications.

Nonetheless near-term financial flexibility is circumscribed by increasingly stringent credit facility covenants compelling active deleveraging strategies alongside disciplined capital allocation prioritizing core projects over dividends or share repurchases presently.

Investors should monitor upcoming plant commissioning milestones alongside sequential revenue/margin recovery trends together with covenant compliance updates which collectively frame Celanese’s trajectory out of its current cyclical trough towards sustainable profitable growth within the dynamic specialty chemicals landscape.

This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments