Cantor Equity Partners IV Leverages Cantor Affiliate Strengths to Identify Target Acquisition in Competitive SPAC Market

Cantor Equity Partners IV remains positioned with substantial trust capital and a Cantor-backed management team to pursue value-accretive acquisitions within its 24-month combination window.

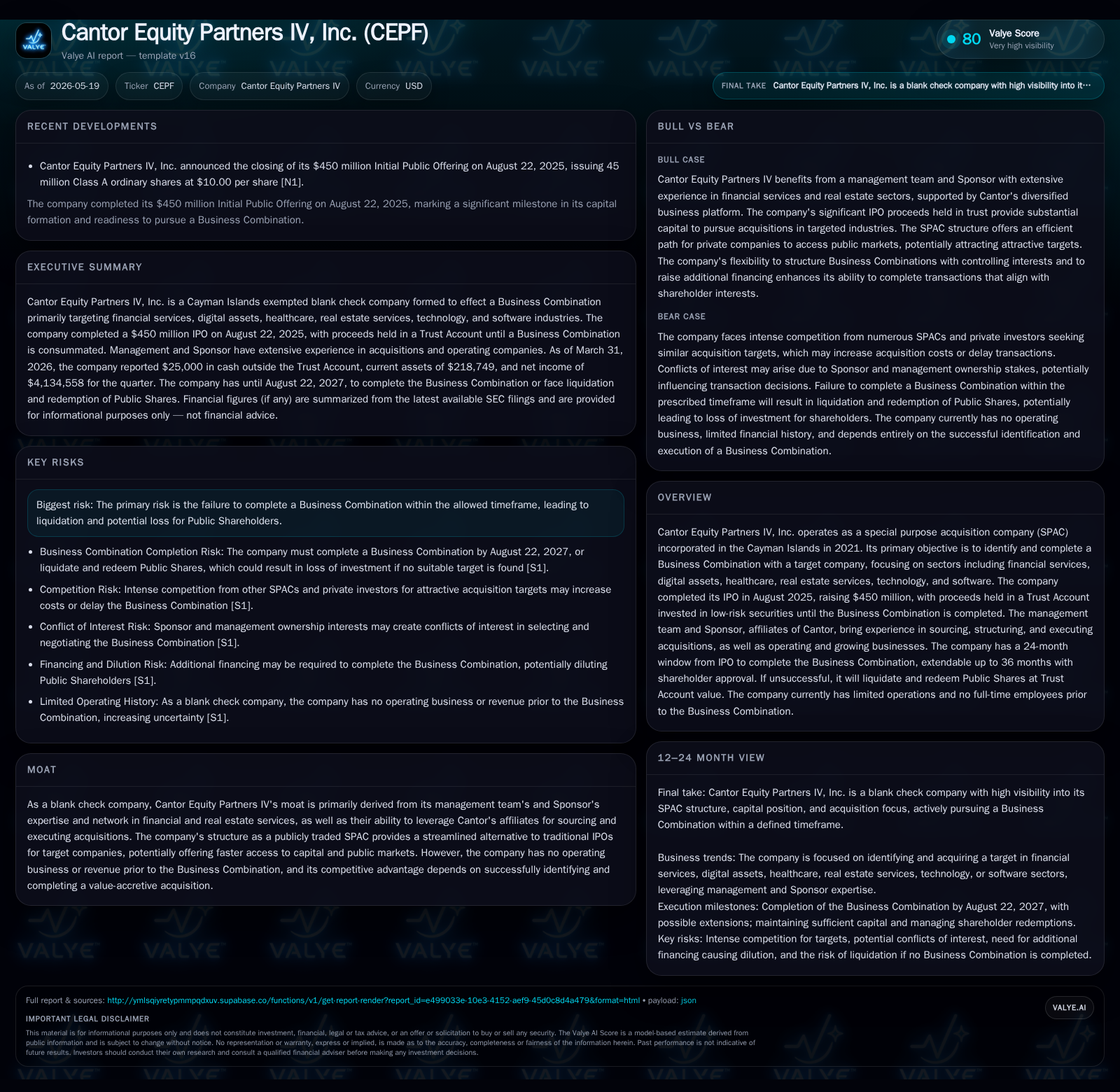

Cantor Equity Partners IV, a Cayman Islands-incorporated SPAC, closed its IPO in August 2025 raising $450 million placed in a trust account pending business combination. The latest Q1 2026 filing reaffirms no material change in risk factors while underscoring the approaching deadline to consummate a deal by August 2027. The company's strategic advantage lies in leveraging Cantor’s diverse financial services and real estate expertise alongside an extensive sponsor network for sourcing and structuring transactions. Sector focus targets financial services, digital assets, healthcare, real estate services, technology, and software industries. Competition among SPACs heightens pressure on deal pricing and timing. Key risks include the finite combination period and execution complexity. Upcoming milestones hinge on identifying attractive targets and securing shareholder approvals for potential extensions or deals.

Latest Quarterly Update: Current Status and Significance

The May 14, 2026 Form 10-Q filed by Cantor Equity Partners IV underscores a steady operating posture centered on readiness to consummate a Business Combination ahead of the August 22, 2027 deadline mandated by its corporate charter. Notably, the filing states explicitly that there have been no material changes to previously disclosed risk factors since the IPO prospectus or the year-end 2025 Annual Report [S2][S27]. This absence of new risk disclosures signals management's confidence in maintaining operational stability during the combination search phase.

The urgency intrinsic to the approaching two-year timeframe adds strategic pressure to identify a suitable target company promptly. Successfully closing a Business Combination within this window is requisite; failure mandates dissolution and redemption of Public Shares at their pro-rata trust value. Therefore, every quarter closer heightens significance for evaluating deal pipeline progression and market receptivity.

Business Model Overview: SPAC Structure and Cantor’s Role

Cantor Equity Partners IV operates as a Special Purpose Acquisition Company (SPAC). It conducted its Initial Public Offering (IPO) on August 22, 2025, generating gross proceeds of $450 million through issuance of Class A ordinary shares at $10 each plus a $9 million private placement to the Sponsor — affiliates of Cantor — cumulatively resulting in approximately $459 million raised [S1][S8]. These proceeds are currently sequestered in a Trust Account invested exclusively in low-risk U.S. government securities or money market funds pursuant to strict regulatory constraints until deployment upon completion of a Business Combination.

This blank check structure entails no operating business or revenue prior to combining with a target company. The core revenue mechanics pivot entirely on successfully completing this Business Combination; post-combination, revenue generation will depend on the acquired entity's operations.

Crucially, CEPF leverages affiliations with Cantor entities which specialize across investment banking (CF&Co.), global brokerage operations (BGC Group), and commercial real estate services (Newmark Group). This ecosystem provides synergistic advantages spanning deal sourcing channels, capital markets access expertise, due diligence capabilities, and operational growth strategies — collectively forming CEPF’s strategic backbone [S1][S5][S8].

Competitive Environment: SPAC Peer Pressure and Deal Dynamics

The SPAC marketplace has seen explosive formation rates recently. While this abundance increases capital availability for deals, it simultaneously intensifies competition for quality target companies meeting fundamental attractiveness criteria. CEPF explicitly acknowledges facing heightened rivalry not only from other SPACs but also private investors and established financial sponsors pursuing similar acquisition targets [S1][S23].

Heightened competition manifests as upwards pressure on acquisition cost structures since sought-after targets may demand improved financial terms such as higher valuations or enhanced earnouts. This inflationary effect can dilute potential returns for Public Shareholders or slow deal completion timing when negotiations stall amidst multiple interested acquirers.

Sponsor Expertise and Network as a Differentiating Asset

CEPF’s moat is largely realized via its Sponsor’s deep domain knowledge bolstered by Cantor’s institutional footprint across complementary sectors. Management possesses multifaceted skills spanning structuring complex transactions globally under variable market conditions; nurturing seller relationships; negotiating terms; integrating post-combination operations; and deploying capital efficiently via debt/equity hybrids tailored to each deal’s context [S1][S5]

This broad competence suite plus proprietary industry contacts confers an edge over competitors lacking such integrated platform support. While no explicit guaranteed moat exists—as typical among SPACs—the qualitative benefits provide partial insulation from commoditized bid scenarios by enhancing both deal flow quality and execution agility.

Investment Criteria and Sector Focus

While CEPF remains corporate flexible about sector choices, it prioritizes industries aligning with management’s experience including financial services, digital assets, healthcare-related businesses, real estate services firms, technology companies and software developers [S1][S5]. Within these verticals favor is given to companies demonstrating positive long-term growth trajectories; potential for recurring revenues offering earnings visibility; opportunities for consolidation or operational improvements enhancing margins; plus scalability prospects either organically or via bolt-on acquisitions.

This focused yet diverse sector approach balances specialization benefits against portfolio diversification considerations post-combination.

Growth Drivers: Deal Sourcing, Structural Advantages, and Market Timing

Key expansion levers include proactive utilization of Sponsor’s network effects for sourcing high-quality targets often not broadly marketed—an important differential versus open-market auctions limiting available runway for negotiation [S3][S6]

Furthermore, CEPF’s ability to deploy multiple forms of consideration—cash from trust accounts combined with debt or equity issuances—endows significant transactional flexibility enabling bespoke deal structuring responsive to seller preferences or market conditions. This structural adaptability enhances potential deal completion probabilities especially in complex integrations.

Another driver is timing virtue: with approximately $456 million held securely pending business combination acceptance as of year-end 2025 [F1][S4], CEPF wields substantial dry powder relative to many peers seeking incremental financing. The possibility of extending the combination window beyond an initial two years with shareholder approval also adds optionality to maximize match quality rather than rushing suboptimal transactions [S6].

Risks and Constraints: Time Window, Competition, and Deal Execution

The cardinal risk remains failure to consummate any Business Combination within prescribed deadlines culminating either in mandatory liquidation or shareholder-approved extensions—a scenario which would extinguish Sponsor investment stake while returning capital principal minus operational expenses to Public Shareholders [S2][S24].

Competitive dynamics exacerbate this risk by elevating acquisition cost bases amid crowded buyer fields thus potentially deterring deals meeting valuation thresholds conducive to accretive shareholder outcomes. Regulatory constraints requiring audited financial statements compliant with U.S. GAAP or IFRS present another hurdle limiting viable candidate diversity since some high-growth private companies may lack audited histories suitable for SEC filings ahead of proxy solicitations [S9].

Post-transaction uncertainties further complicate outlooks such as integration challenges or management transitions given CEPF currently operates without dedicated employees relying primarily on executive officers whose roles fluctuate based on combination progress stages [S23][S24].

Key Upcoming Catalysts: Milestones and Investor Signals

Market attention should focus keenly on announcements regarding identified prospective targets as management refines its acquisition thesis into firm proposals accompanied by proxy materials soliciting shareholder votes. Shareholder approval events constitute critical junctures not only validating due diligence outcomes but also allowing redemption elections that materially influence deal economics.

Should circumstances warrant an extension beyond August 2027 completion date expectations exist that CEPF will seek formal shareholder consent for prolongation thereby buying additional evaluation time—an event likely accompanied by disclosures relating to pipeline status plus terms under consideration including any parallel private financing transactions intended to shore up transaction capital shelves [S3][S6][S9]

Regulatory milestones involving compliance with proxy solicitation rules under SEC jurisdiction also act as monitoring points signaling progress toward finalizing merger agreements.

Financial Context: Liquidity and Capital Deployment Readiness

CEPF reported holding approximately $456.7 million in its Trust Account at the end of December 2025 which consists mainly of net proceeds collected from IPO transactions less permissible withdrawals used for tax payments or organizational expenses per regulatory agreement terms governing SPACs [F1][S4]. This liquidity represents near-total capital availability reserved exclusively for funding future acquisitions ensuring ample purchasing capacity over near-term horizons.

There is no indication of outstanding indebtedness constraining this capital base nor any leveraging reported that might limit financial flexibility before or after deal closure according to latest regulatory filings reviewed through Q1 2026 [F1][S27]. The trust funds’ conservative treasury investments yield minimal risk exposure preserving principal values crucial for Public Shareholder protection prior to consummation.

This analysis synthesizes all relevant public disclosures up through May 19th, 2026 including recent quarterly filings facilitating an informed perspective on CEPF’s position within its peer framework without offering investment advice.

Financial position in context

As of 2025-12-31, companyfacts shows $25000 in cash and equivalents [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments