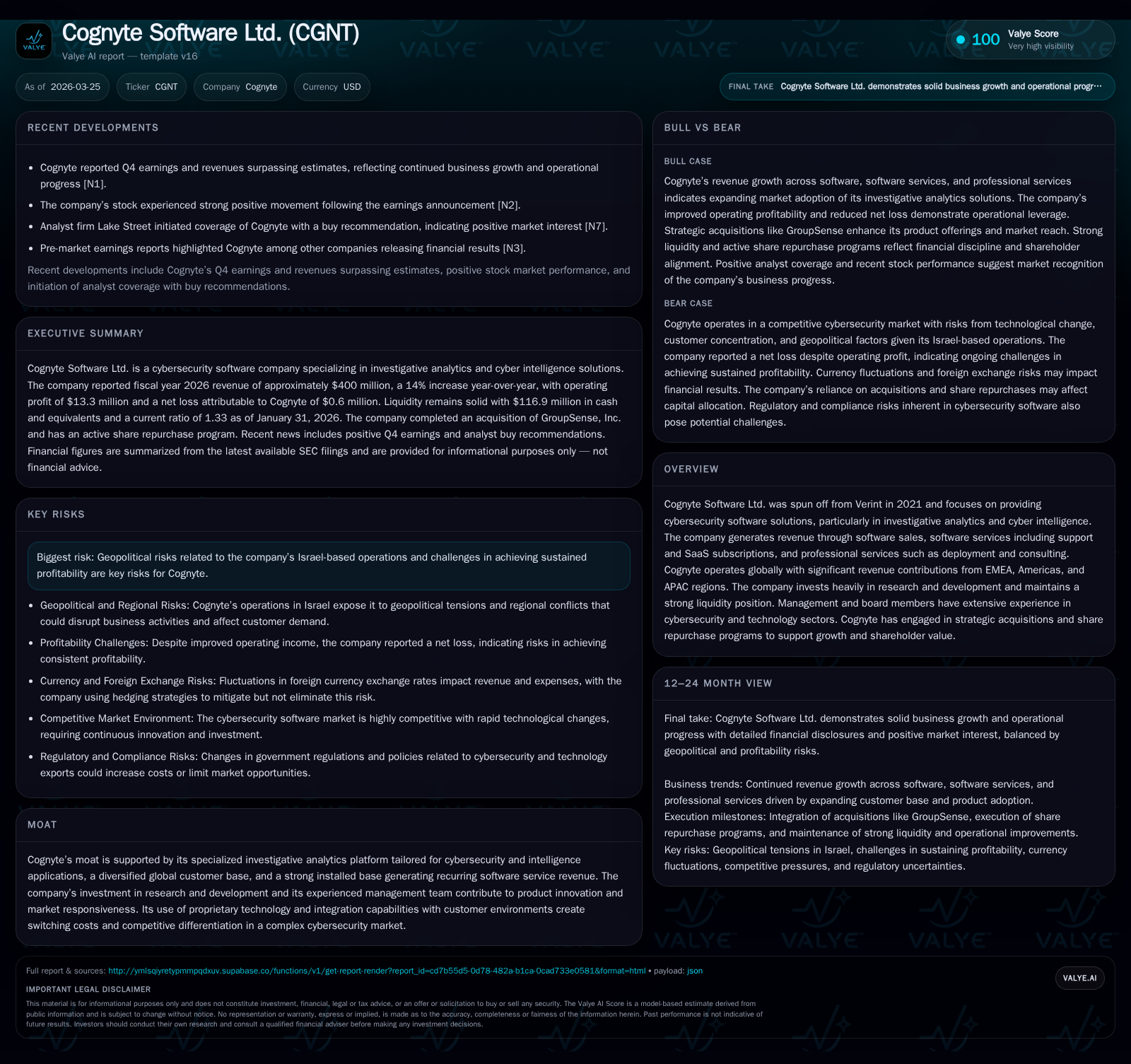

Cognyte Software’s Earnings Turnaround and Strategic Outlook for Cybersecurity Innovation

Cognyte has transitioned from sustained operating losses to profitability, leveraging software and service revenue growth alongside disciplined capital management.

Cognyte Software Ltd. reversed a multi-year trend of operating losses with a $13.3 million operating profit in the fiscal year ended January 31, 2026, reflecting robust top-line expansion driven by software sales and recurring service revenues. The company’s strong focus on research and development, combined with strategic acquisitions and sustained share repurchases, underpins its competitive position in investigative analytics for cybersecurity. While geopolitical risks tied to its Israel-based operations persist, Cognyte’s improving cash flow generation and capital discipline suggest resilient operational leverage. Going forward, market watchers should monitor subscription growth, margin expansion, and execution against strategic milestones amid evolving cyber threat landscapes.

From Losses to Operating Profit: Tracking Cognyte’s Recent Financial Rebound

Cognyte Software Ltd., since its spin-off in 2021 focusing on cybersecurity investigative analytics and cyber intelligence solutions, has experienced a marked financial turnaround culminating in fiscal year 2026 (FY2025) with operating income of $13.3 million — a sharp reversal from the prior year’s operating loss of $5.1 million [F1][S1]. This represents a substantial year-over-year (YoY) increase of approximately 173.5%. While operating expenses rose materially—driven largely by increased research & development (R&D) and selling general & administrative (SG&A) costs—the escalation in gross profit by $42.8 million outpaced these cost increases.

Net loss attributable to Cognyte narrowed significantly to $0.6 million from a loss of $12.1 million the prior fiscal year, evidencing operational discipline and improving profitability dynamics despite heavier tax provisions and slightly reduced other income contributions [F1][S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | 40 | 13 | 10 | |

| 2023 | -16 | 35 | -18 | 7 | +86.4% |

| 2022 | -114 | -37 | -103 | 8 | -666.5% |

| 2021 | -15 | 3 | 11 | 12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 21 | 30 | -0.3 |

| 2023 | 0 | 28 | -7.9 |

| 2022 | 0 | -45 | -58.8 |

| 2021 | 0 | -9 | -5.2 |

Source: SEC companyfacts cache [F1].

Table notes: “NM” indicates not meaningful due to negative base or large percentage swings; CFO is operating cash flow.

Segment Insights: Software Sales and Services Driving Revenue Expansion

The company’s revenue growth was primarily fueled by significant increases across its three principal segments: software license sales surged by $35.9 million; software service revenues—including support and SaaS offerings—increased by $6.7 million; and professional services such as deployment and consulting rose by another $6.7 million [S1][N1]. These figures underscore Cognyte's growing footprint within specialized cybersecurity domains where investigative analytics platforms integrate deeply with customers’ operations.

Notably, recurring revenue streams from software services like SaaS subscriptions provide sticky income that smooths revenue volatility common in license-centric models within cybersecurity markets [N1]. The company’s strategic emphasis on expanding SaaS offerings complements traditional perpetual licensing—an essential balance that addresses evolving customer preferences towards subscription consumption while maintaining high-margin product sales.

Regional Revenue Breakdown Reflecting Global Customer Engagement

Geographically, Cognyte draws revenue broadly: approximately 54% stems from the Europe, Middle East & Africa (EMEA), 34% from Asia-Pacific (APAC), and the remaining ~12% from the Americas [F1][S1]. This distribution reflects both the company's historic strength in EMEA intelligence communities and increasing penetration into APAC markets.

Such diversification mitigates region-specific risks but simultaneously exposes results to currency fluctuations—as noted by the company’s disclosure on exchange rate impacts that modestly enhanced reported revenue yet also elevated operating expenses when compared to prior-year rates [S1]. Currency headwinds remain an inherent consideration given the Israeli shekel base versus multinational sales.

Technology Leadership and R&D: Fueling Product Innovation and Market Stickiness

Cognyte’s moat principally derives from its focused R&D investment underpinning its investigative analytics platform tailored for cyber intelligence workflows—a complex niche requiring proprietary algorithms capable of real-time threat detection alongside deep data integration capabilities.

In FY2025, R&D spend rose by approximately $14.1 million or 13%, reaching $122.3 million—chiefly due to personnel-related cost increases as well as reduced capitalization of software development costs [F1][S8]. Such elevated R&D outlays highlight the company’s commitment to innovation vital for sustaining differentiation in a crowded cybersecurity landscape where switching costs hinge on platform integration depth.

The ongoing funding accentuates capability enhancement efforts including AI-driven analytics modules designed to improve investigator productivity—a feature increasingly critical as global cyber threats evolve rapidly [S8].

Future Challenges: Geopolitical Risks and Profitability Sustainability

Cognyte openly acknowledges geopolitical risk linked to its Israel-based operations—a region characterized by political volatility including conflicts with Iran and other hostile actors—which may disrupt operational continuity or restrict product sales internationally [S9][S15].

Further operational risks include achieving sustained profitability given substantial fixed-cost bases inherent in software development coupled with foreign currency exposures.

These elements warrant close monitoring as they bear on margin stability and long-term return profiles amidst cyclic cybersecurity budget environments compounded by governmental scrutiny in export controls affecting technology transfers.

Capital Allocation Discipline: Share Repurchases and Strategic Acquisitions

Cognyte has pursued disciplined capital management policies reflecting confidence in its intrinsic value creation trajectory.

During FY2025 alone, the company executed share repurchases totaling approximately $21.4 million across more than two million shares—significantly ramped compared to prior years—and maintains ongoing buyback authorizations aggregating up to an additional $40 million through mid-2027 [F1][S5][S12].

Additionally, Cognyte acquired digital risk protection firm GroupSense for ~$4.4 million in cash with contingent earn-outs capped at $5 million—illustrating tactical use of M&A aligned with product portfolio expansion without overextending balance sheet leverage [S4].

No dividends were declared or discussed explicitly confirming reinvestment priority remains central while buybacks complement equity value support.

Operating Cash Flow and Capital Expenditure Trends: Signs of Operational Leverage

Operational cash flow generation has been positive for three consecutive years post-spin-off—reaching $40.3 million for FY2025 despite higher working capital needs—compared to negative cash flow seen prior to separation (e.g., negative $37 million in FY2022) [F1].

Capital expenditures increased nearly 48% to roughly $10.4 million owing chiefly to property/equipment purchases and capitalized development costs invested back into platform capabilities [F1][S8].

Subtracting capex yields free cash flow around $29.9 million—solid proof the company is unlocking robust operational leverage amid scaling endeavors.

Liquidity remains ample; end-FY25 current assets stood at roughly $298 million relative to current liabilities near $224 million—a current ratio roughly estimated at 1.33 providing adequate short-term flexibility [F1].

What to Watch Next: Milestones and Market Catalysts

With no explicit forward financial guidance provided recently, investors should track several key performance indicators:

- Expansion rate of SaaS subscriptions contributing toward recurring revenue growth,

- Further progression towards consistent net profitability supported by R&D-driven innovation,

- Execution of announced share buyback programs underscoring board confidence,

- Potential follow-on acquisitions strengthening complementary cybersecurity capabilities,

- Geopolitical developments impacting export compliance or regional client engagements.

Successful navigation will demonstrate whether Cognyte can sustain this momentum within a highly competitive cyber intelligence sector known for rapid product obsolescence risk coupled with stringent market regulations.

This report synthesizes publicly available filings and news as of March 25, 2026 without providing investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments