Concrete Leveling Systems Faces Liquidity Crisis Despite Niche Market Presence

The company's June 2026 quarter reveals severe liquidity stress alongside modest project revenue in the concrete repair niche.

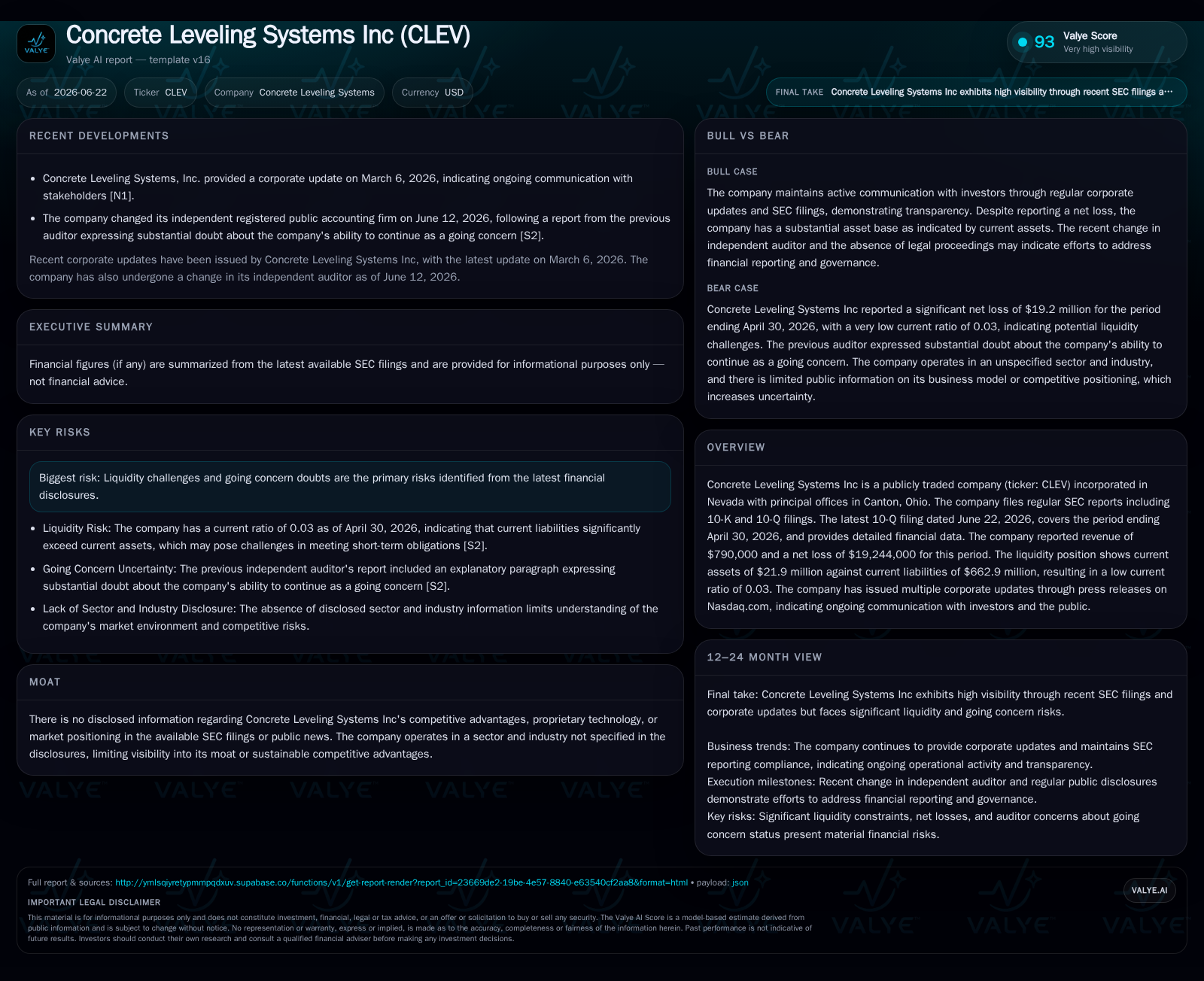

Concrete Leveling Systems Inc reported $790,000 in revenue but a substantial net loss of $19.2 million in its latest quarter ending April 30, 2026, highlighting acute financial distress exacerbated by an extremely low current ratio of 0.03. Operating within the fragmented concrete leveling and surface restoration sector, the company depends on project-based contracts for residential and commercial customers, with tight margins influenced by labor and equipment utilization. Despite growth drivers like aging infrastructure and rising repair demand, liquidity constraints and cash flow timing risks pose significant operational challenges. Moving forward, key focus areas include backlog development, cost management, and stabilizing working capital to address going concern doubts.

Latest Quarterly Operating Update Highlights Financial Strain

Concrete Leveling Systems Inc’s most recent quarterly report dated June 22, 2026 (10-Q) discloses deeply troubling financial dynamics that define its near-term outlook. Revenue remained very low at approximately $790,000 for the period ended April 30, 2026, while a staggering net loss of $19.2 million was recorded [S2][F1]. This unprecedented loss dwarfs the revenue base and reveals significant operating inefficiencies or one-time impairments affecting the bottom line. More critically from a financial health perspective is the company’s current assets of $21,886 against liabilities nearing $662,850—amounting to an extremely low current ratio of roughly 0.03 [F1].

This acute liquidity squeeze heightens risk surrounding the company’s ability to continue as a going concern—a status explicitly noted by its auditor Stephano Slack LLC in prior fiscal-year statements [S3]. The firm’s struggle with working capital positions reflects typical challenges faced by small construction subcontractors reliant on timely project payments amid variable contract sizes and durations.

Concrete Leveling Systems’ Business Model and Service Offering Dynamics

Concrete Leveling Systems operates principally as a specialty construction service provider focused on concrete leveling, foundation repair, surface restoration, and related sub-contracting activities [S1]. Revenue is generated through discrete projects serving a mix of residential clients, commercial property owners, and potentially local infrastructure maintainers. These operations typically involve techniques such as slab jacking or polyurethane foam injection to restore uneven concrete surfaces efficiently without full replacement.

The company’s business model hinges on efficiently managing job site personnel and equipment utilization to optimize margins in a low-scale operation context. Given industry norms, revenues are subject to significant variability based on project backlog size—a key leading indicator that tracks contracted work awaiting completion—and average project size which directly influences cash flow timing. Warranty or service contracts may provide some recurring elements but likely represent a minor share or emergent aspect given CLEV's modest scale.

Labor productivity remains paramount since construction services are intrinsically labor-intensive with costs tied closely to skilled crew availability and compliance with safety standards. Material costs — particularly specialized polyurethane foams used in leveling — also impose margin pressures if inflationary.

Competitive Positioning Amid Fragmented Concrete Repair Sector

The concrete repair segment is notably fragmented with numerous small to midsize entities competing regionally rather than nationally. Local market presence establishes competitive advantage alongside reputation for quality workmanship and timely delivery. Larger peers such as U.S. Concrete offer scale-based efficiencies that smaller operators like CLEV cannot replicate but cater primarily to different client segments or geographies.

CLEV thus faces direct competition from regional foundation repair specialists who leverage established customer relationships with general contractors or property managers outsourcing specialized tasks. The company's success or struggles heavily depend on maintaining skilled crews capable of executing compliant repairs that withstand warranty inspections — service quality being a critical differentiator.

Growth Catalysts: Infrastructure Demand and Service Innovation Potential

Industry-wide growth prospects derive from several secular trends including accelerating infrastructure repair spending driven by aging highways, public works, and residential renovations—areas where concrete leveling offers cost-effective alternatives to demolition-and-replacement. Urbanization further fuels demand as cities seek maintenance solutions for sidewalks and parking infrastructure.

Technological advances such as polyurethane foam injection have expanded repair options enabling faster job completion times with less disruption compared to traditional slab jacking techniques—potentially broadening client acceptance.

Geographic expansion into new regions or forging strategic partnerships with general contractors present additional levers for scaling project backlog value — the principal pipeline metric influencing future revenue streams. Regulatory incentives supporting infrastructure upkeep may further stimulate demand.

Constraints: Liquidity Pressures and Industry Operational Risks

Although market fundamentals appear supportive, CLEV’s operational progress is severely constrained by its deteriorated liquidity position [S2][F1]. Project-based cash flows are inherently lumpy due to milestone billing schedules—delayed payments can cascade into working capital shortages undermining the ability to fund payroll or materials purchases promptly.

Moreover, seasonality effects linked to weather impede continuous crew utilization especially during winter months impacting labor productivity metrics. Rising raw material costs exacerbate gross margin erosion unless price increases can be effectively passed onto customers—often difficult given competitive pressures.

Warranty claims pose reputational risks amplifying customer service costs if workmanship fails prematurely; high frequency of service calls diminishes customer retention rates vital for repeat business.

Notably, the company’s multiple recent auditor changes culminating in Sadler Gibb & Associates’ appointment reflect increasing regulatory scrutiny triggered by prior going concern disclosures highlighting historical financial reporting sensitivities [S3][S21].

Next Steps for Investors: Milestones to Monitor and Execution Challenges Ahead

Key indicators that will inform updates on Concrete Leveling Systems’ trajectory include any reported changes in project backlog values which would signal improved visibility into upcoming revenue streams post-quarter-end [S2]. Monitoring trends in utilization rates of labor crews and specialized equipment offers insight into operational efficiency gains or setbacks mitigating large losses.

Cost-control measures addressing material purchasing strategies amid inflation will also be critical.

Further clarity on auditor reports coupled with management commentary on turnaround plans could temper ongoing going concern concerns.

Financial Snapshot: Liquidity Metrics Underpinning Ongoing Viability Concerns

Quantitatively, as of April 30, 2026 Concrete Leveling Systems faced an unbalanced liquidity profile with current assets approximately $21.9k sharply contrasted by current liabilities near $662.9k yielding a dangerously low current ratio of about 0.03 [F1]. Total debt stood around $187k – modest in absolute terms but significant relative to cash reserves estimated below $1k indicating stressed short-term funding capacity [F1].

This imbalance underpins the substantial net loss for the period ($19.2 million) reflecting either exceptional charges or deeply inefficient operations that jeopardize sustainable cash generation needed for ongoing business functions absent corrective actions [S2][F1]

This analysis synthesizes Concrete Leveling Systems Inc’s recent operating disclosures anchored primarily on its June 2026 quarterly filing alongside sector-informed context relevant to its concrete repair niche. The company faces formidable near-term headwinds centered on liquidity strains compounded by inherent volatility in project-driven revenues typical among regional construction subcontractors. While macro demand drivers remain intact owing to infrastructural maintenance needs and technological innovation in repair methods, unlocking durable profitability will depend on disciplined operational execution addressing cash flow timing mismatches and cost efficiency improvements.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or research views regarding specific securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments