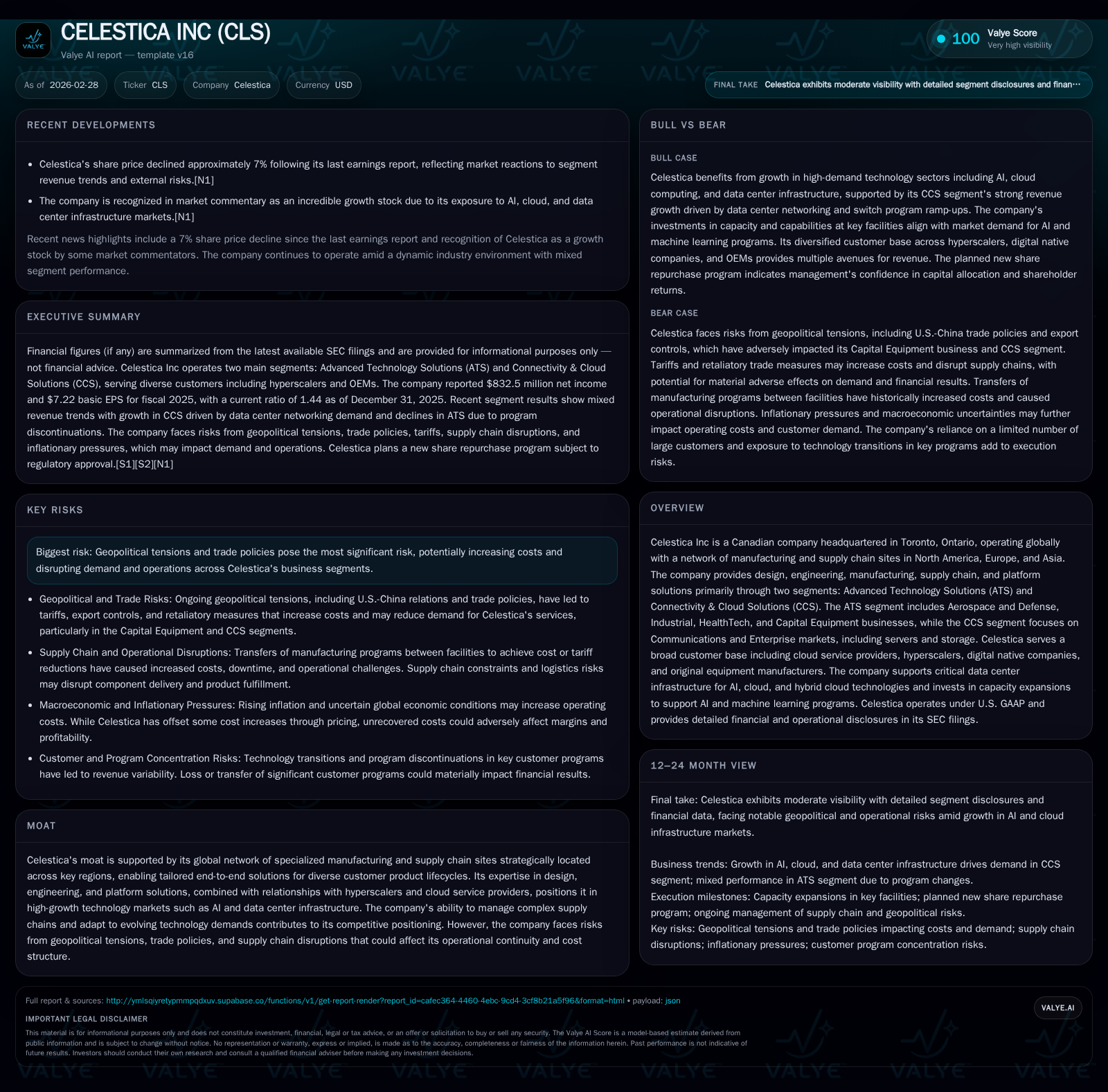

Celestica Inc Advances Profitability Through AI-Driven Capacity Expansions and Segment Diversification

Celestica's 2025 financials reflect strong profitability gains amid targeted growth in high-demand AI and data center markets.

Celestica Inc demonstrated notable earnings growth in 2025, driven by strategic investments in AI and hyperscale data center infrastructure within its Connectivity & Cloud Solutions segment, as well as improved margins in Advanced Technology Solutions. The company’s diversified business model, with geographic manufacturing presence spanning North America, Europe, and Asia, supports resilience against geopolitical risks while facing potential headwinds from tariffs and trade uncertainties. Cash flow generation remains robust, enabling continued share repurchases and capital expenditure to sustain growth initiatives. Future growth hinges on maintaining technology partnerships with hyperscalers and navigating supply chain challenges.

Overview

Celestica Inc is a Canadian electronics manufacturing services (EMS) provider headquartered in Toronto with a global footprint spanning North America, Europe, and Asia. The firm operates primarily through two reportable segments: Advanced Technology Solutions (ATS), which includes Aerospace & Defense, Industrial, HealthTech, and Capital Equipment sectors; and Connectivity & Cloud Solutions (CCS), focusing on Communications and Enterprise markets such as servers and storage systems [S9].

Historical Financial Performance

The company’s recent annual filings reveal accelerating profitability trends. In fiscal year 2025, Celestica reported operating income of $1.04 billion — a 73.7% increase from $599 million in 2024 — while net income doubled to $832.5 million from $428 million the prior year [F1]. This margin expansion was supported by improved segment mix and operational efficiencies.

Operating cash flow strengthened to $659.5 million in 2025 from $473.9 million in 2024, highlighting solid internal liquidity generation amid higher working capital demands. Capital expenditures rose modestly by 17.7% to $201.2 million as management invested primarily in capacity expansions for AI-related manufacturing programs at key sites in Thailand, Malaysia, and Richardson, Texas [F1][S14].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 833 | 660 | 1041 | 201 | +94.5% |

| 2024 | 428 | 474 | 599 | 171 | |

| 2017 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 153 | 458 | 37.6 |

| 2024 | 152 | 303 | 22.6 |

| 2017 |

Source: SEC companyfacts cache [F1].

Note: Revenue data was not explicitly provided; focus placed on available profitability and cash flow figures.

Equity increased from approximately $1.90 billion in 2024 to $2.22 billion in 2025 reflecting retained earnings accumulation [F1], resulting in an approximate return on equity (ROE) of about 37.6%, demonstrating effective capital utilization.

Segment Performance Drivers

Advanced Technology Solutions (ATS)

Despite a revenue decline of around 4% in Q3 2025 relative to Q3 2024—primarily due to the discontinuation of a loss-making Aerospace & Defense program—the ATS segment boosted its operating margin from roughly 4.9% to about 5.5%. This improvement was driven by better program mix and increased operational efficiency within aerospace product lines [S14].

Connectivity & Cloud Solutions (CCS)

This segment experienced significant expansion with a reported revenue increase of approximately 43% year-over-year in Q3 2025 powered mainly by an explosive rise (82%) in the Communications end market linked to hyperscaler data center networking switch programs reaching volume ramp-up phases [S14]. Meanwhile, the Enterprise market saw a notable contraction of about 24%, attributed to technology transitions affecting one major AI/ML compute platform customer.

Hardware Platform Solutions revenue scaled to near $1.4 billion for Q3 alone — representing nearly half of total revenues — confirming the segment's pivotal role supporting high-growth AI and cloud infrastructure deployments [S14].

Segment margins improved accordingly, rising from around 7.6% to approximately 8.3% quarter-over-quarter due to beneficial business mix shifts favoring higher-margin hardware solutions coupled with operational leverage effects.

Future Growth Prospects

Celestica targets future expansion via ramped investments aligned with AI-driven demand surges across hyperscale data centers. The company confirmed ongoing capacity upgrades at strategic locations—especially in Southeast Asia and Texas—to meet scaling customer requirements for AI/ML platforms [S14]. These facility enhancements underscore Celestica’s positioning as a critical manufacturer behind foundational infrastructure for cloud computing advances.

Moreover, Celestica's integrated engineering design capabilities combined with global supply chain reach offer differentiated end-to-end solutions attractive in volatile EMS markets increasingly shaped by technological complexity and rapid legacy program transitions.

However, significant risks arise from geopolitical tensions notably U.S.-China trade frictions affecting tariffs and export controls on semiconductor technologies that constrain portions of the Capital Equipment business and CCS segment offerings [S6][S13]. The extent of these regulatory measures introduces uncertainty regarding cost structures and demand sustainability moving forward.

Customer program transfer frequency presents another operational challenge due to potential disruption costs related to shifting production footprint among different facilities—sometimes mandated for cost reduction or tariff mitigation reasons—which could depress short-term profitability [S20].

Forecasts / Milestones / Expectations

While explicit company guidance is limited in publicly disclosed documents for calendar year projections beyond Q3-2025 results, management has expressed expectations that high levels of capital expenditure commitments from leading hyperscalers will continue supporting ongoing growth trajectories within CCS [S14]. Investors should monitor updates relating to ramp schedules for new AI/ML compute platforms as indicative milestones signaling progression toward materialized sales expansion.

Furthermore, the preliminary announcement regarding the upcoming Annual Meeting scheduled for May 19, 2026 suggests governance continuity but provides limited financial forecasting detail so far [S3].

Returns / Capital Allocation

During fiscal year 2025 Celestica exhibited prudent capital deployment balancing reinvestment with shareholder returns:

- Approximately $153 million deployed toward common share repurchases facilitated under the company’s existing Normal Course Issuer Bid expiring October 31, 2025 [F1][S12][S24]; this amount closely aligns with the prior fiscal year’s buyback activity demonstrating disciplined commitment.

- Capital expenditures totaled $201 million earmarked mainly for capacity buildups targeting anticipated sustained demand growth areas within AI-enabled manufacturing ecosystems.

- Robust CFO after capex yielded estimated free cash flow near $458 million indicating healthy liquidity profile enabling flexibility for debt servicing or additional shareholder distributions if decided.

No dividend amounts are conspicuously noted within recent SEC filings indicative either of non-payment or immaterial yields presently; emphasis lies predominantly on accretive share repurchase programs supplemented by strategic reinvestments [F1][S12][S24].

Competitive Moat and Operational Strategy

Celestica’s moat derives extensively from its command over a geographically diversified manufacturing network strategically located to mitigate regional risk factors while providing bespoke supply chain solutions specific to customer product lifecycles across various industries—from aerospace defense applications through hyperscale digital native platforms supporting critical cloud infrastructure . This multifaceted capability aids retention amongst blue-chip customers confronted with volatile component availability constraints prevalent throughout EMS sectors.

Its engineering service depth enhances stickiness by embedding development cycles upstream relative to assembly stages — assuring adaptability against rapid technological advancement pressures typical of server/storage and industrial equipment manufacturers servicing AI workloads.

Risks

Central risks pivot around macro-political factors including:

- Escalation of tariffs or retaliatory trade actions between key economic zones affecting unit costs negatively if not recovered via pricing adjustments [S16][S13].

- U.S.-imposed export restrictions targeting semiconductor chips impact key developmental components necessary within Celestica's Capital Equipment and CCS markets thereby constraining both top-line growth and margin profiles through restricted sales or forced supply chain rerouting [S16].

- Transfer or loss of customer programs due to changing outsourcing preferences or competitive displacement could engender inefficient manufacturing utilization leading to elevated fixed cost burdens or restructuring charges associated with facility downsizing or closures [S20].

- Operational disruptions arising from logistics challenges such as labor strikes at ports or carrier constraints elevate shipping expenses possibly eroding margins despite attempts at multi-modal transport diversification strategies [S8].

- Global inflationary pressures heighten input costs that may not be entirely offsettable through price pass-through given competitive landscape dynamics impacting overall margin sustainability.

Conclusion

Celestica stands at an inflection point shaped by its successful harnessing of cloud and AI-driven market segments underpinning its Connectivity & Cloud Solutions revenues along with steady improvements in traditional aerospace/manufacturing divisions encapsulated within ATS. Its strong liquidity position combined with solid free cash flow generation allows continued reinvestment into capacity expansions vital for future contract wins while maintaining shareholder value through measured buyback activities. Nonetheless, persistent geopolitical trade uncertainties alongside evolving technological standards will require vigilant execution of global supply chain resilience strategies plus ongoing innovation within service delivery models. Monitoring quarterly sales momentum particularly linked to hyperscaler client rollouts will provide critical readouts on Celestica’s ability to convert recent investments into sustainable long-term financial performance gains.

This analysis is based solely on publicly available information sourced from SEC filings ([F1],[S#]) and recent news reports ([N#]). It aims at providing contextual understanding without making any form of investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments