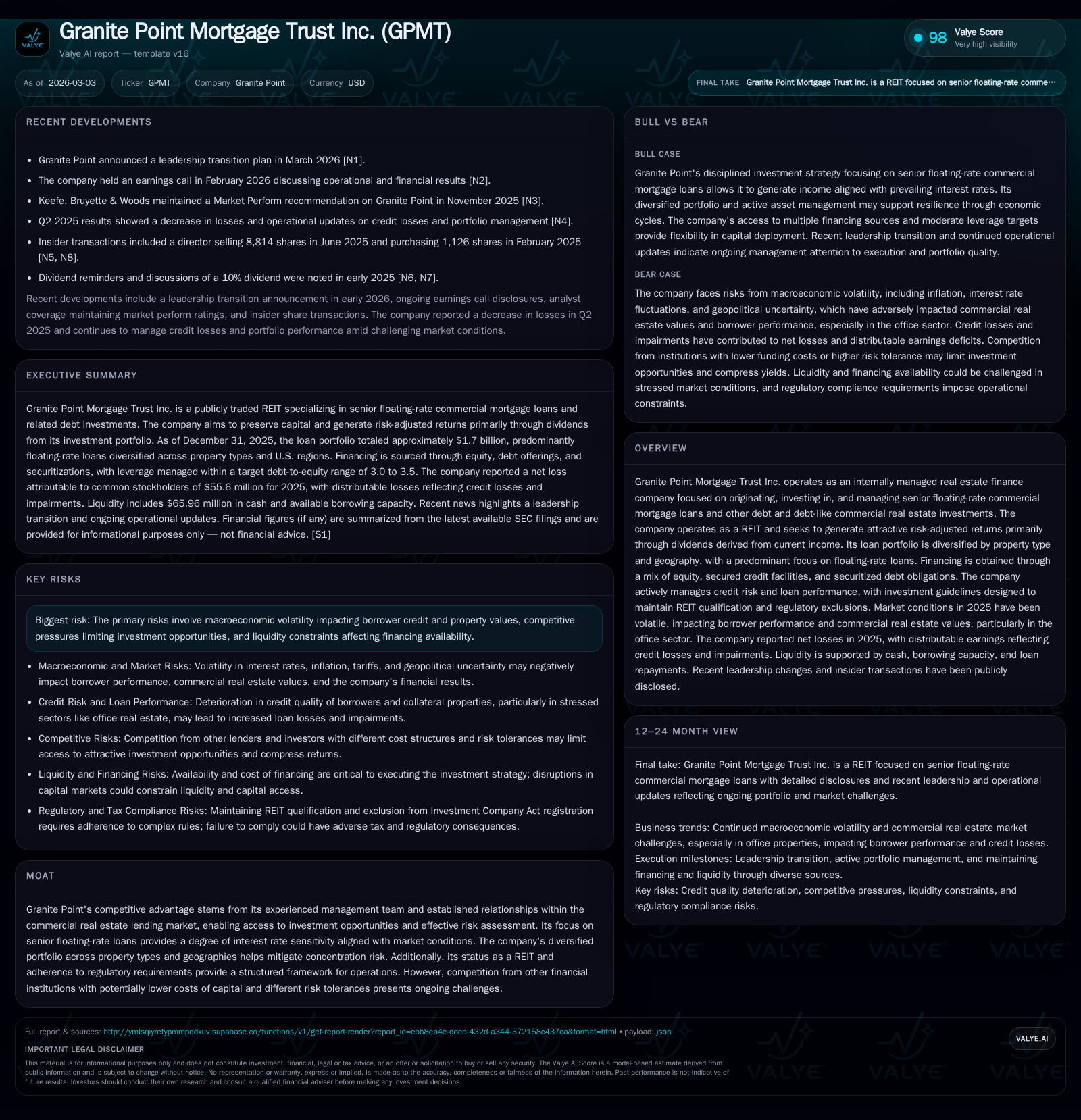

Granite Point Mortgage Trust Refines Its Floating-Rate Strategy Amid CRE Volatility

GPMT leverages its senior floating-rate loan portfolio and disciplined capital management to sustain dividends during a turbulent 2025 commercial real estate market.

Granite Point Mortgage Trust (GPMT) faced a challenging 2025 commercial real estate environment, marked by elevated interest rates, tariff uncertainties, and persistent office sector weakness that pressured borrower credit quality and property values. The company’s historically floating-rate senior loan focus moderated interest rate risk but did not insulate against macro-induced performance volatility. GPMT reduced leverage ratios, actively managed its diversified portfolio, and preserved shareholder income through dividend adjustments and share repurchases amid constrained cash flows. A recent leadership transition adds a layer of strategic uncertainty as the firm weighs future growth opportunities within continuing market headwinds.

Operating History: Growth Drivers and Recent Performance Trends

Granite Point Mortgage Trust Inc., an internally managed REIT specializing in senior floating-rate commercial mortgage loans, delivered a notable improvement in net income metrics during fiscal 2025 despite significant challenges in the commercial real estate (CRE) environment. According to final year-end figures [F1], GPMT reported a net loss of approximately $41.2 million for 2025, a marked improvement versus the prior year's loss of $207.1 million — an 80.1% enhancement year-over-year. This narrowing loss reflects ongoing portfolio restructuring and credit management as macroeconomic pressures persisted.

However, operating cash flow (CFO) exhibited a substantial contraction, declining nearly 70% year-over-year from $8.8 million to $2.7 million in 2025 [F1]. This drop underscores the impact of slowed loan repayments during elevated borrowing costs for tenants and borrowers constrained by weakening CRE fundamentals. Dividend distributions followed suit with a sharp reduction from $24.0 million in 2024 to $10.4 million in 2025 [F1], indicative of prudent income preservation strategies under strained cash flows.

The company also engaged in share repurchases totaling $5.7 million last year, down from $7.6 million the previous year [F1], signaling cautious capital allocation intent while balancing shareholder returns.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -41 | 3 | +80.1% |

| 2024 | -207 | 9 | -227.6% |

| 2023 | -63 | 52 | -54.8% |

| 2022 | -41 | 59 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 10 | 6 | -7.4 |

| 2024 | 24 | 8 | -33.4 |

| 2023 | 43 | 10 | -7.4 |

| 2022 | 54 | 16 | -4.2 |

Source: SEC companyfacts cache [F1].

Note: Net income YoY reflects improvement but operating cash flow shrank significantly; dividends and buybacks show parallel cutbacks to conserve liquidity [F1].

Portfolio Composition and Credit Quality amid Macroeconomic Uncertainties

Granite Point's loan portfolio as of December 2025 was composed predominantly of senior floating-rate commercial mortgage loans diversified by property type and geography [S1][S6]. Approximately 97% of loans earn interest indexed to SOFR with floating-rate liabilities providing natural hedging against interest rate volatility [S25]. The weighted average stabilized loan-to-value (LTV) at origination stood near a conservative mid-60% level — around 65% — aligning with institutional underwriting standards for CRE lending.

Nevertheless, commercial real estate credit quality faced pressure notably from the office property segment which continues experiencing elevated vacancies and tenant churn due to shifts toward remote work arrangements post-pandemic [S1]. Some loans secured by office buildings were downgraded or placed on nonaccrual status as collateral values deteriorated amidst uncertain leasing prospects [S22]. Specific instances included modification or resolution of impaired loans tied to hotel properties in Minneapolis and student housing assets indicating selective portfolio risk management [S21][S24].

The company's diversification approach mitigated concentration risk across various asset classes including retail, multifamily, industrial and hotel sectors alongside geographic dispersion across major US markets [S6]. Furthermore, Granite Point employed rigorous quarterly evaluations of collateral performance incorporating property financials and market fundamentals leveraging third-party servicers under internal oversight [S18]. Targeted originations remain focused on intermediate-term bridge or transitional financing characterized by floating-rate terms supportive of rising rate environments [S1].

Capital Structure and Financing Strategy: Navigating Leverage and Liquidity

In maintaining financial flexibility during volatile markets, Granite Point actively managed its capital stack comprising repurchase agreements ($439 million), securitized debt obligations via CRE CLOs ($644 million), secured credit facilities ($72 million), and recently added mortgage loan payable ($17.5 million) as of December 31st, 2025 [S4][S9][S11]. Total borrowing capacity approximated $1.1 billion collateralized largely by loans held-for-investment along with some REO holdings.

Leverage parameters showcased prudent deleveraging from prior years: total leverage ratio (debt minus cash/equity) declined from roughly 2.2x at end-2024 to around 2.0x at end-2025 while recourse leverage improved from around 1.0x to approximately 0.8x [S25]. These reductions resulted primarily from scheduled principal payments on repurchase agreements/CRE CLOs alongside partial paydowns of held-for-investment loans [S20].

Financial covenant compliance remains solid with unrestricted cash liquidity exceeding $66 million versus required minimums well above $30 million or regulatory percentage thresholds; tangible net worth stood at $701 million surpassing covenant floors; leverage ratios remained well below maximum caps of ~77%-80%; interest coverage ratio exceeded minimum targets at ~1.35x versus required ~1.20–1.30x [S10][S16][S26].

Maturity profiles indicate bulk of secured borrowings mature within one year but are subject to revolving extensions under facility agreements that were recently extended into mid-2026 for key counterparties including Morgan Stanley Bank and JPMorgan Chase Bank [S17][S23]. The residential refinance of REO asset in Maynard MA introduced a longer-dated financing option maturing in October 2030 providing additional liquidity certainty beyond short-dated revolvers [S5][S11].

Dividend Policy and Capital Allocation: Preserving Income for Shareholders

Dividend distributions have been scaled back markedly over recent years consistent with operating cash flow limits imposed by market dislocations and borrower performance challenges [F1][S27]. Common dividends declined from $54 million paid in FY2022 to just over $10 million in FY2025 representing an approximate fourfold reduction coinciding with loss periods reducing dividend coverage ratios substantially.

Despite these headwinds, Granite Point maintained an ongoing share repurchase program with about $5.7 million deployed last year against a lower authorization balance remaining for repurchase as per latest disclosures [F1][S27]. This balanced approach suggests management prioritizes capital preservation while cautiously supporting equity price stability given constrained distributable earnings.

REIT status compels the company to distribute taxable income primarily via dividends; thus they must navigate a fine balance between compliance-driven payout requirements against liquidity preservation considerations amid uncertain earnings trajectories [S1]. Dividend policy going forward is expected to remain conservative as GPMT evaluates continuing market stressors affecting borrower health.

Executive Leadership Update: Implications for Strategy and Governance

On March 3rd, Granite Point announced a planned leadership transition involving its CEO that will be effective shortly [N2]. While exact strategic shifts have yet to be articulated publicly beyond standard succession protocols, this change injects additional governance considerations as the firm confronts complex external challenges including evolving CRE demand dynamics and tightening financing markets.

Continuity of investment philosophy focusing on senior floating-rate loans paired with meticulous asset management appears likely given entrenched industry expertise within the senior team; however operational execution risks linked to transition periods warrant close observation particularly if accompanied by consequential strategic recalibrations or new capital market initiatives.

Forward-Looking Perspectives: Market Risks and Growth Opportunities

External factors casting uncertainty over Granite Point’s near-term growth include macroeconomic volatility driven by tariff disruptions impacting inflation rates; prolonged elevated interest rates adversely affecting borrower refinancing costs; geopolitical instability influencing capital market liquidity; and structural shifts in CRE demand favoring logistics or multifamily segments over traditional office spaces [S1][N1].

Nonetheless there remain tactical growth avenues anchored in selective originations targeting transitional financing niches less sensitive to economic cycles combined with anticipated easing or stabilization in credit spreads that could revive loan prepayment/refinance volumes crucial for liquidity recycling [N1]. Monitoring key metrics such as nonaccrual loan trends within office-heavy exposures alongside securitization issuance activity will be critical barometers for assessing risk-adjusted return prospects absent formal guidance provided by management.

Key Metrics Summary: Financial Snapshot and Efficiency Ratios to Watch

Synthesizing core financial metrics reveals persistence of negative returns on equity (ROE), approximately -7.4% for FY2025 derived from net loss relative to equity base ($552 million) despite improvements over prior years [F1]. Concurrently operating cash flow contractions indicate mounting pressures on internal funding generation requiring vigilance around dividend coverage levels.

Leverage reduction efforts have improved balance sheet resilience evidenced by declining total debt/equity ratios that remain comfortably within covenant limits; liquidity buffers retained well above minimum thresholds provide noteworthy operational flexibility despite compressed margins inherent to current CRE lending milieu.

| Year | Net Income (USD) | YoY % | CFO (USD) | YoY % | Dividends Paid (USD) | YoY % | Buybacks (USD) | YoY % |

|---|---|---|---|---|---|---|---|---|

| 2022 | -40,825,000 | 58,898,000 | 54,277,000 | 15,714,000 | ||||

| 2023 | -63,198,000 | -54.8% | 52,096,000 | -11.5% | 42,895,000 | -20.9% | 10,298 ,000 | -34.% |

| 2024 | -207 ,051 ,000 | >100% | _8 ,756 ,000 | -83 .2 % | _24 ,009 ,000 | -44 .0 % | _7 ,621 ,000 | -26 .0 % |

| 2025 | -41 ,152 ,000 +80 .1 % | _2 ,667 ,000 | -69 .5 % | _10 ,370 ,000 | -56 .8 % | _5 ,662 ,000 | -25 .7 % |

Approximate ROE for FY2025 stands near negative -7.4%, reflecting operating losses albeit improved versus prior years relative to equity base.

This analysis compiles Granite Point’s publicly filed SEC statements supplemented with credible news sources as current through early March 2026 without speculating beyond disclosed data or guidance intentions.[F1][S1][N1][N2] Investors should conduct their own due diligence considering evolving macro-financial conditions impacting the commercial real estate finance sector before forming views on future prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments