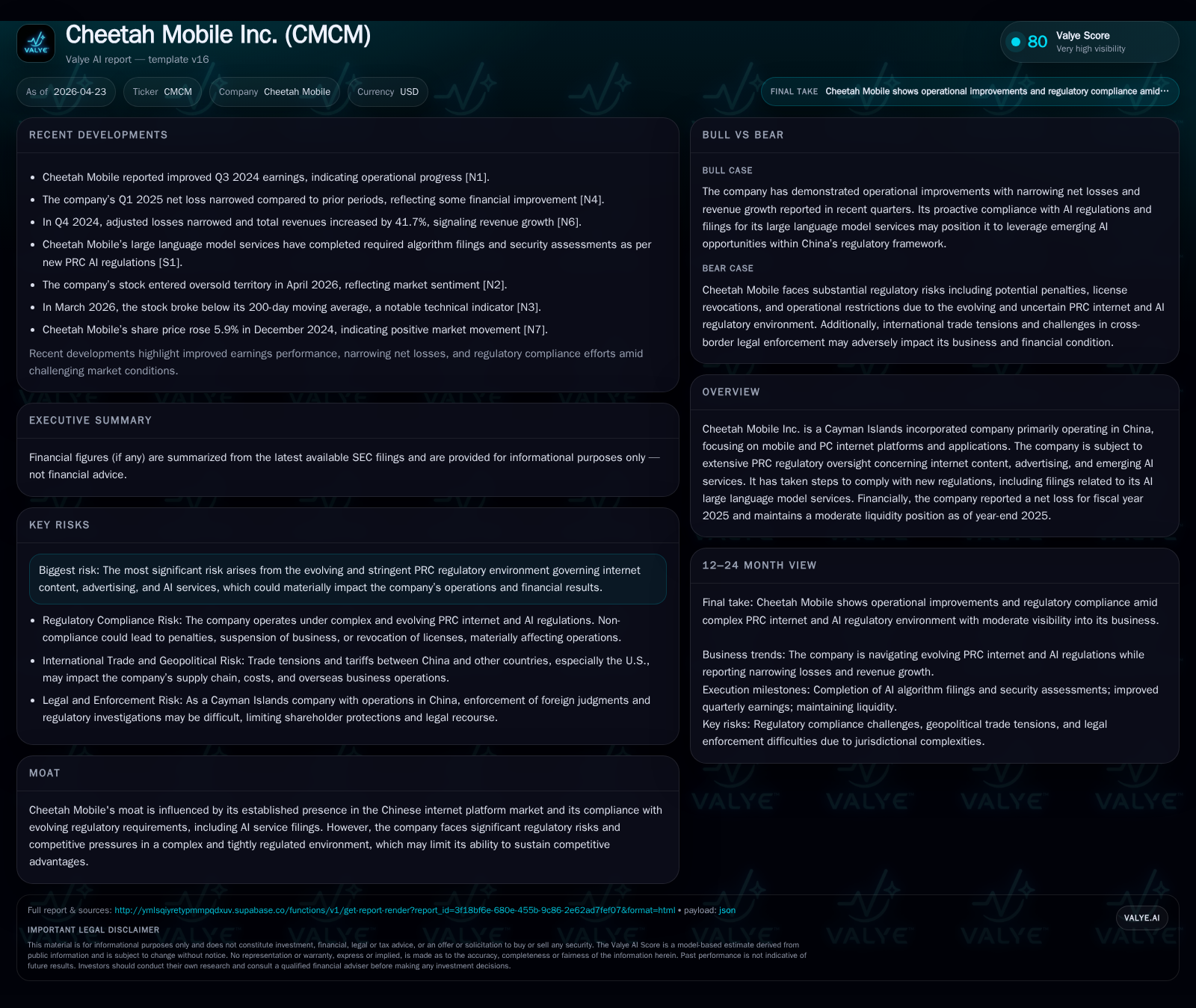

Cheetah Mobile Innovates AI amid Regulatory and Competitive Pressures

Q4 2025 results reveal a strategic pivot to AI-driven services, improving margins and reducing losses amid a challenging Chinese regulatory landscape.

Cheetah Mobile’s latest quarterly filing highlights a substantial revenue shift toward its AI and others segment, which grew to represent 46.5% of total revenues in 2025 from 35.9% in 2024, signaling a strategic emphasis on AI-powered applications, cloud services, and robotics. This transition underpins improved gross margins (up to 72.5%) and substantially reduced operating losses, reflecting early operational leverage despite ongoing net losses. The company continues to operate under tight regulatory scrutiny in China, particularly relating to internet content and emerging generative AI regulations, necessitating strict compliance measures which could constrain growth but also cement competitive positioning for compliant innovators.

Recent Quarterly Results Highlighting Growth Shifts

Cheetah Mobile's Q4 2025 report filed on March 24, 2026 ([S2]) marked a pivotal shift in its revenue composition with substantial growth in the AI and others segment. Fiscal year 2025 revenues surged to RMB1.15 billion (US$164.5 million), up from RMB807 million in 2024 ([S1], [F1]) — powered largely by an 84.7% increase in AI-related services which now comprise nearly half (46.5%) of total revenue versus just over one-third the prior year.

Notably, gross margin improved materially to 72.5% from 67.6%, driven by the higher profitability profile of advertising agency services within the AI segment as well as better operational efficiencies realized through scale ([S4]). The operating loss narrowed dramatically to RMB179 million (US$25.7 million) from RMB437 million the prior year — a >57% reduction that reflects both revenue mix improvement and cost containment strategies. Although still unprofitable at the net level (RMB257 million net loss attributable), the company’s trajectory indicates early operating leverage linked to its strategic repositioning.

Evolving Business Model Anchored in Internet Platforms and AI Innovation

Cheetah Mobile derives revenue primarily from two broad segments: the legacy Internet business focused on online advertising and value-added subscription services; and a burgeoning "AI and others" category encompassing overseas advertising agency services, multi-cloud management offerings targeting corporate clients, sales/rental of robotics products (notably following its acquisition consolidation of UFACTORY mid-2025), and other AI applications ([S1], [S6], [S9]).

The Internet business remains significant at ~53.5% of revenue but is shrinking proportionally due to intensified competition and user base fluctuations exacerbated by shifting consumer preferences ([S17]). Advertising revenues depend heavily on supply-demand bid dynamics within platforms while value-added subscription conversions require continuous product innovation to retain engagement.

In parallel, the company has accelerated R&D investments (+42% YoY increase reaching RMB346 million or US$49.5 million in expenditure) concentrating on proprietary and third-party AI agent technologies alongside robotics engineering talent acquisition ([S3], [S4], [S7]). Strategic partnerships with global cloud providers (e.g., Amazon Web Services) and social media giants (e.g., Meta) as authorized advertising agencies underpin their international expansion efforts for both multi-cloud management services and overseas advertising operations.

Competitive Landscape and PRC Regulatory Environment

Within China’s intensely competitive utility software market—characterized by rapid innovation cycles and fierce pricing pressures—Cheetah Mobile’s differentiation rests upon its expanding portfolio of AI-powered applications integrated with robotic hardware offerings (, [S20]). However, deriving sustainable pricing power is complicated due to platform partners’ dominant roles controlling access to advertising inventories; this dynamic limits pass-through pricing agility.

Regulatory compliance constitutes a dominant risk vector for Cheetah Mobile. The company operates under rigorous PRC government oversight governing internet content distribution via CAC directives implementing algorithm filing mandates specifically for generative AI service providers ([S1], [S20]). Cheetah Mobile successfully completed the required algorithm filing for its OrionStar large language model service—an important milestone affirming regulatory adherence—but uncertainties remain regarding evolving measures such as security assessments linked to public opinion control aspects embedded in these regulations.

Moreover, legal restrictions around foreign ownership via Variable Interest Entity arrangements complicate capital flows that impact liquidity deployment across its subsidiaries; withholding tax implications further constrain dividend repatriation potential ([S1], [S16]). These factors collectively mold a cautious operating environment where compliance sophistication becomes a competitive necessity.

Drivers and Constraints for Medium-Term Growth

Growth catalysts center on Cheetah Mobile's ability to deepen user engagement through enhanced AI-driven features embedded within existing software products while cultivating new revenue streams from innovative robotic devices targeting enterprise automation segments ([S4], [Valye moat & risks]). International expansion leverages cross-border partnerships to offset domestic market saturation but introduces currency risk, additional taxation complexity, and local market entry hurdles ([S6], [S7]).

Conversely, constraints persist including volatile user bases vulnerable to competitor aggressiveness or changing device ecosystems; regulation-induced delays or caps on product launches; increased compliance costs associated with mandatory filings; risks of slower-than-expected adoption rates for multi-cloud management tools; plus maintaining production cost efficiencies critical for robot sales profitability ([S17], [S7]). Technological investments must balance speed-to-market against expense discipline amid resource-intensive R&D commitments.

Key Milestones and Near-Term Catalysts to Monitor

Several upcoming developments merit attention: quarterly updates detailing improvements or deterioration in segment-level contribution margins will illuminate whether operating leverage gains continue alongside scaling revenues ([S2]). Regulatory updates shaping approval processes or modifications of generative AI service mandates could materially affect rollout schedules or scope of offerings.[N1]

Integration progress of acquisitions such as UFACTORY—which contributed roughly RMB36 million (~US$5.2 million) post-July 2025—will serve as an indicator of execution capabilities ([S4]). Lastly, tracking liquidity trends amid capital expenditures aimed at technology upgrades versus cash burn rates will reveal financial resilience needed during this transition phase.[F1],[S11]

Financial Overview: Profitability, Liquidity, and Investment Trends

Cheetah Mobile’s financial position reflects ongoing transformation challenges with a recorded operating loss of approximately US$25.7 million for FY2025 compared with US$59.9 million the prior year—signifying notable improvement though sustained operating deficits persist ([F1]). Net losses contracted alongside operating loss reduction yet remained negative at around US$36.8 million owing partly to non-cash impairment adjustments decreasing from previous years.

The company maintains moderate liquidity headroom supported by about US$215 million cash and equivalents coupled with a current ratio near 1.27x indicating sufficient short-term asset coverage relative to liabilities ([F1], [S11]). Capital expenditure was curtailed sharply (-72%) illustrating prudence amid heightened uncertainty while R&D ramped up significantly highlighting priorities shifted toward future-proofing through technology innovation ([S3],[F1]).

| Year | Total Revenue (RMB mil) | Internet Business % | AI & Others % | Gross Margin % | Operating Loss (USD mil) |

|---|---|---|---|---|---|

| 2024 | 806.9 | 64.1 | 35.9 | 67.6 | -59.9 |

| 2025 | 1150.4 | 53.5 | 46.5 | 72.5 | -25.7 |

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -37 | -25 | -26 | +56.4% |

| 2024 | -85 | -33 | -60 | +0.4% |

| 2023 | -85 | 78 | -30 | -14.1% |

| 2022 | -74 | -62 | -33 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -16.0 |

| 2024 | -32.5 |

| 2023 | -24.5 |

| 2022 | -16.9 |

Source: SEC companyfacts cache [F1].

Overall, improvements illustrate early success reorienting business model toward higher-value AI verticals amidst a complex regulatory framework unique to China's tech ecosystem.

This analysis is based solely on information contained in Cheetah Mobile Inc.’s SEC filings as of April 23, 2026 and related news items . It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments