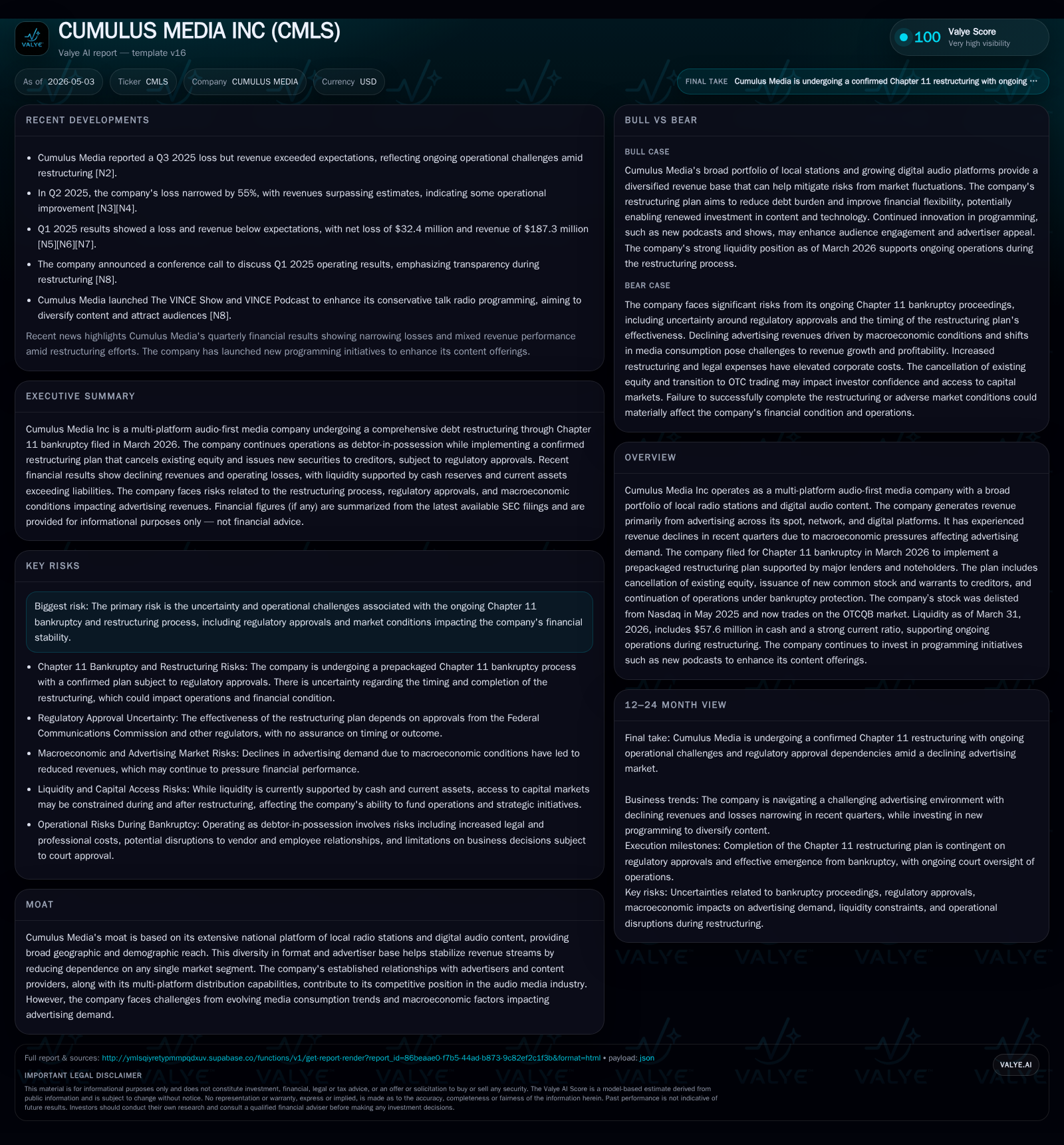

Cumulus Media's Chapter 11 Restructuring Highlights Pressures on Radio Advertising Revenue

The company continues operating during bankruptcy amid declining ad sales and plans a significant equity reset.

Cumulus Media's latest quarterly report reveals a 12.2% drop in net revenue primarily caused by macroeconomic weakness impacting spot and network advertising. The company filed for Chapter 11 bankruptcy in early 2026 to implement a prepackaged restructuring plan that cancels existing equity and issues new stock to creditors, aiming to stabilize liquidity with $57.6 million in cash on hand. Despite challenges from digital media competition and economic pressures on advertising budgets, Cumulus maintains a broad geographic radio footprint and digital assets providing some operational resilience. Key risks include execution of the restructuring plan, regulatory approvals, and continued demand softness in audio advertising.

Recent Operating Update

Cumulus Media's Q1 2026 Form 10-Q [S2] reports net revenues of $164.4 million, a decline of approximately $22.9 million or 12.2% from $187.3 million in Q1 2025 [S21]. This decrease predominantly reflects weaker spot and network advertising revenues down by $13.2 million and $10.9 million respectively due to unfavorable macroeconomic conditions impacting advertiser demand [S21]. Digital revenues fell by $3 million mainly affected by lower podcasting and streaming income but were partially offset by increases in digital marketing services revenue along with higher trade and barter revenues [S21]. Content costs dropped $13.4 million (-16.9%), largely driven by renegotiated broadcast rights contracts and reduced third-party inventory expenses aligned with revenue declines [S21]. Selling, general & administrative (SG&A) expenses also decreased by nearly $9 million (-9.6%) due to lower personnel costs including incentives, alongside reduced ratings fees but offset somewhat by increased barter expenses [S21]. Depreciation expense was down modestly (-17%). Corporate expenses surged almost double primarily due to higher legal and restructuring-related costs as Cumulus navigates ongoing bankruptcy proceedings [S21]. The company reported an operating loss of $26.4 million for Q1 versus an operating loss of $14.8 million the prior year period [S21]. Adjusted EBITDA—a key non-GAAP metric focused on operational cash generation—decreased from $3.5 million in Q1 '25 to $2.7 million in Q1 '26 [S21], indicating continued margin pressure.

Liquidity remains tight but manageable; as of March 31, 2026, Cumulus held approximately $57.6 million in cash equivalent reserves with current assets exceeding current liabilities by nearly sixfold (current ratio ~5.86) [F1][S24]. The company filed for Chapter 11 bankruptcy protection on March 4, 2026 to implement a court-approved restructuring plan negotiated with major lenders holding roughly 83% of the company's Term Loans and Senior Notes due in the late 2020s [S2]. The restructuring support agreement prescribes cancellation of all existing equity securities with creditors receiving new common stock plus exit convertible notes representing approximately 95% ownership post-reorganization [S2]. The company operates as debtor-in-possession during this process under Bankruptcy Court supervision.

Business Model

Cumulus Media operates as a multi-platform audio-centric media enterprise focused on local radio broadcasting complemented by growing digital content offerings including streaming audio and podcasts [S1]. Revenue is predominantly generated through advertising sales distributed across spot (local), network (national), and digital platforms where clients pay for airtime or targeted campaign placements based on listener reach and demographics — critical levers being audience size/engagement metrics, market coverage, and creative formats available.

The company's diverse portfolio comprises hundreds of local stations spread across numerous U.S. markets capturing varied demographic segments (music genres, news/talk formats) which mitigates exposure to any single region or advertiser vertical allowing for some revenue stability amid advertising cyclicality [S1][S24]. Digital components such as programmatic advertising on streaming platforms and emerging podcast monetization remain smaller but strategically vital parts aimed at future growth given shifts in consumer audio consumption habits.

Margins are influenced heavily by content licensing fees, royalties tied to broadcast rights agreements, dealer commissions tied to station sales or trades (notably reflected within barter activities), and general operational overhead including talent contracts as well as corporate administrative costs which can fluctuate during restructuring or litigation-related periods [S21][S24]. The company highlights that SG&A expenses can be managed via personnel adjustments while content-related expenditures tend to follow revenue scales albeit with contractual minima constraining short-term flexibility.

Industry Structure and Competitive Position

The U.S. radio broadcasting industry faces disruptive pressures from rapid adoption of on-demand streaming services (Spotify, Apple Music), free ad-supported streaming channels (Pandora), and podcasting alternatives capturing younger demographics typically less engaged with traditional AM/FM radio [S1]. Despite this trend, terrestrial radio retains relevance for local advertisers targeting regional audiences through trusted brands and personalities.

Cumulus’ moat stems from its extensive footprint spanning multiple formats (sports talk, country music, top-40 pop etc.) offering advertisers geographic granularity plus multi-platform integration combining traditional airwaves with digital channels providing cross-selling opportunities [S1]. Competitors include similarly large broadcasters like iHeartMedia along with regional groups as well as purely digital competitors vying for advertiser budgets.

Regulatory constraints include maintaining FCC licenses associated with broadcast frequencies that require compliance with various operational parameters limiting rapid consolidation or drastic format changes without approvals [S2]. The recent filing disclosed that certain subsidiaries holding FCC licenses did not take part directly in the bankruptcy filing ensuring operational continuity for critical market licenses [S2].

Growth Drivers

While legacy spot/network advertising has declined recently due to macroeconomic headwinds suppressing marketing spends broadly, Cumulus aims to grow its digital marketing services segment which showed resilience despite other declines [S21]. This includes targeted online campaigns leveraging user data analytics merging radio listeners' profiles with online platforms taking advantage of cross-device marketing trends.

Podcasting investments represent another strategic avenue given increasing audience adoption nationally; however, currently this segment contributes modestly relative to core radio revenues but offers potential long-term upside if monetization models mature adequately.

Additionally, barter transactions have increased recently contributing incremental revenues through reciprocal deals reducing cash outflows while maintaining service levels enhancing short-term liquidity management during restructuring phases [S21][S24].

Post-emergence from Chapter 11 restructuring is expected to grant Cumulus balance sheet relief enabling capital redeployment towards content innovation or acquisitions pending market conditions improving advertiser sentiments.

Risks / Watchpoints / Growth Constraints

The foremost risk is the inherent uncertainty accompanying bankruptcy proceedings including timely regulatory approvals required for reorganization consummation plus potential delays arising from creditor negotiations or adverse court rulings [S2]. Execution risks around emerging from Chapter 11 intact will influence longer-term viability.

Macroeconomic volatility driving reductions in corporate advertising budgets particularly affects Cumulus’ largest revenue source—local spot advertising—which is vulnerable to cyclical economic downturns exacerbated currently by inflationary pressures reducing discretionary marketing spending overall.

Evolving consumer audio habits increasingly shift away from traditional radio towards digital streaming platforms posing a structural challenge requiring successful strategic pivots into digitally-focused products at scale.

FCC licensing compliance remains critical; any unexpected revocations could materially impair operations in key markets affecting revenue stability.

What To Watch Next

- Confirmation of completion of the Chapter 11 Plan effective date following court approval anticipated shortly after Q1 filings [S2][S3].

- Quarterly financials post-emergence to assess stabilization or improvement trajectory particularly focusing on adjusted EBITDA trends versus historical lows.

- Digital segment growth metrics including podcast audience expansion rates or new advertising partnerships demonstrating scaling effectiveness.

- Monitoring advertiser spending patterns especially local spot categories linked closely to broader economic indicators such as consumer sentiment or retail sales performance.

- Any regulatory developments impacting FCC license renewals or modifications relevant to the company's station portfolio.

- Management commentary concerning strategic priorities addressing technology shifts or competitive responses post-restructuring announcements.

Financial Profile Snapshot (As of March 31, 2026) [F1]

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $58mm | |

| 2026-03-31 | ||

| Current assets | $214mm | |

| 2026-03-31 | ||

| Current liabilities | $36mm | |

| 2026-03-31 | ||

| Current ratio | 5.86x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Total debt figure last updated early prior fiscal year-end; actual current amount subject to Chapter 11 adjustments.

Disclaimer: This analysis is based solely on publicly available SEC filings up through April 29, 2026 ([S2], [S3], [S1]) supplemented with companyfacts data ([F1]) as provided and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments