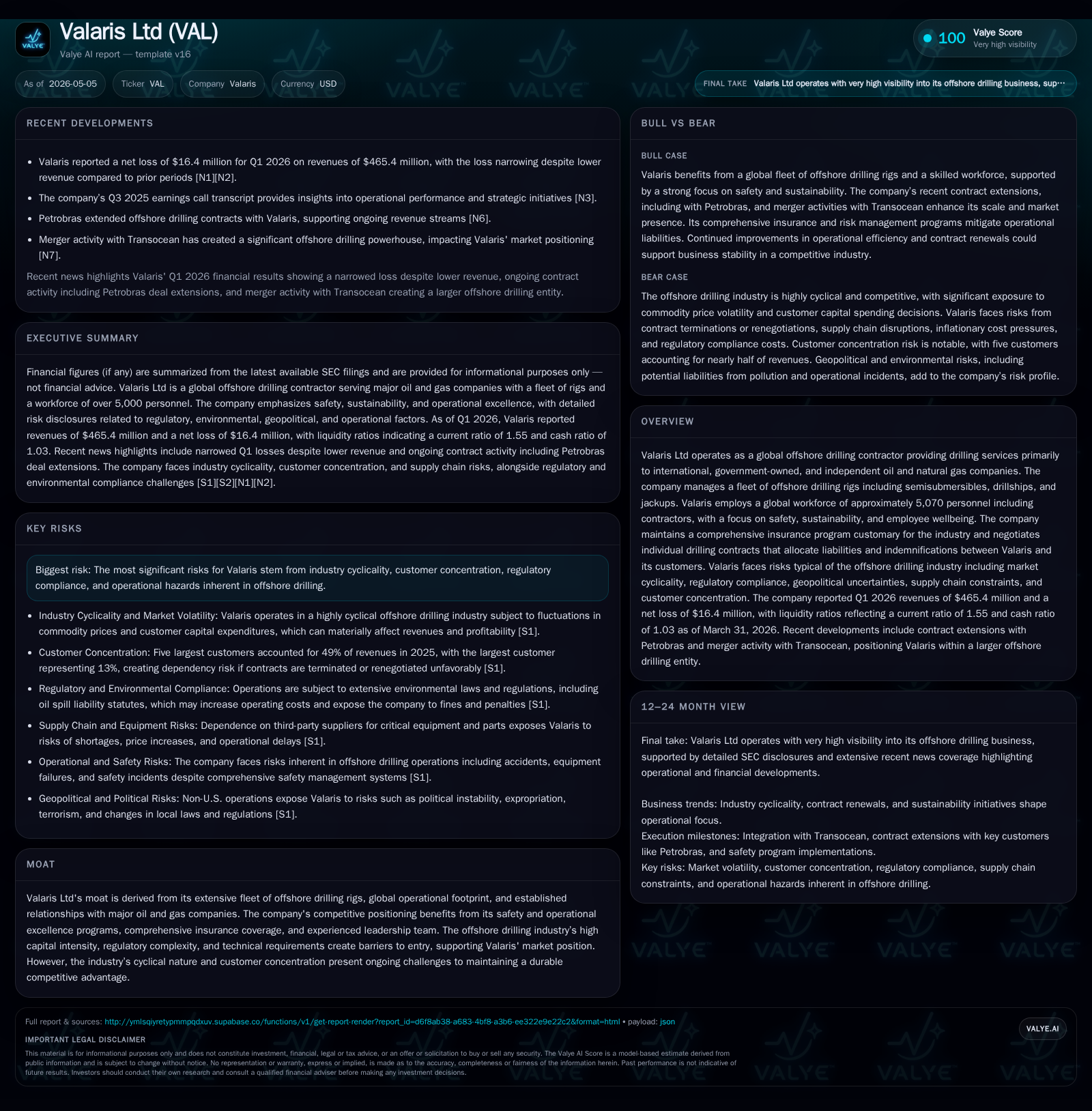

Valaris Reports Stable Q1 2026 with Ongoing Offshore Drilling Consolidation

Valaris' latest quarter highlights steady operations while navigating industry cyclicality ahead of a transformative merger.

In Q1 2026, Valaris Ltd maintained solid operational momentum with revenues reflecting the offshore drilling sector's cyclical nature. The company’s extensive rig fleet and global presence underpin its competitive standing despite concentrated customer exposure and regulatory headwinds. Key near-term growth hinges on contract renewals and integration progress following the announced merger with Transocean. Risks include tightening regulations, geopolitical uncertainties, and capital structure constraints amid an evolving energy market.

Recent Operating Update

Valaris Ltd’s Q1 2026 earnings report [S2], filed May 5th, confirms stable revenue generation of approximately $465.4 million amid ongoing sector volatility [N1][N2]. Although profitability remained pressured due to higher operating costs and transitional expenses, narrowing losses signal operational resilience. Notably, management reaffirmed commitments to safety and sustainability across its global fleet comprising semisubmersibles, drillships, and jackup rigs that underpin its service delivery to diverse oil producers [S1].

Significant near-term strategic context arises from the February announcement of a proposed merger with Transocean Ltd., aiming to consolidate two leading offshore drillers into a combined entity commanding vast rig assets worldwide [S7][S18]. This deal introduces both potential synergy benefits — such as enhanced fleet utilization — and integration risks involving contract continuity given possible change-of-control clauses impacting client relationships.

Business Model Analysis

Valaris generates revenue primarily by contracting its offshore drilling rigs under day-rate agreements or long-term contracts with international oil companies (IOCs), national oil companies (NOCs), and independent operators [S1]. Customers pay for drilling services enabling exploration or development activities; these fees are influenced by rig type specialization, geographic location, contract duration, and prevailing oil market dynamics.

Day rates can fluctuate based on rig availability globally—reflecting supply-demand imbalances—and Valaris’ pricing power is partly linked to its capability to offer premium assets compliant with stringent safety and environmental standards. However, customer contract concentrations impose dependence risks: five clients contributed roughly 49% of revenues in 2025 highlighting vulnerability if any large contract is renegotiated or terminated unfavorably [S8].

Operationally, Valaris invests heavily in rig maintenance and safety programs. Shipments of critical equipment are subject to global trade regulations affecting supply chain timing [S14], while labor regulations across multiple jurisdictions may raise costs or constrain workforce flexibility [S16]. The company also negotiates indemnification terms that allocate pollution liability generally toward customers though retains residual risk from negligent acts or limits on vendor protections [S1].

Industry Structure and Competitive Position

The offshore drilling industry features high capital intensity and technical complexity barriers deterring new entrants—favoring incumbents like Valaris with established fleets and comprehensive insurance programs that mitigate third-party liabilities up to $855 million per policy terms [S1]. This moat is fortified by operational expertise required to meet escalating environmental regulations post major accidents such as the Macondo well incident.

Competition includes peers like Transocean (future merger partner), Noble Corporation, and Seadrill. Valaris’ differentiation lies in its fleet size diversity enabling service across shallow water jackups through deepwater semisubmersibles and drillships coupled with a global footprint. Nonetheless, industry cyclicality dictated by upstream capital expenditure cycles injects volatility into demand forecasting.

Ongoing regulatory tightening—especially in U.S. Gulf of Mexico operations—and potential climate litigation add layers of complex operational risk that influence cost structure and captive insurance spend [S10][S17].

Growth Drivers

Valaris’ growth prospects hinge on several measurable factors:

- Backlog expansion: Contract awards extending rig utilization into later years provide revenue visibility; leveraging large-scale contracts with NOCs such as Petrobras underscores this dynamic [N8].

- Pricing improvements: Sustained recovery in day rates driven by tightening available rig supply supports margin enhancement.

- Geographic diversification: Penetrating emerging offshore markets less saturated by competitors could offset region-specific regulatory constraints.

- Operational efficiency: Advances in rig automation and digital monitoring could reduce downtime enhancing profit margins.

- Merger synergies: Combining operations with Transocean promises cost reductions via fleet rationalization rationalizing duplicative administrative overheads.

These drivers are moderated by cyclical upstream capex cycles; however, fundamental demand for hydrocarbons remains steady enough over medium term to underpin investment in new offshore projects requiring specialized drilling capability.

Risks and Growth Constraints

Key challenges restricting Valaris’ growth trajectory include:

- Industry cyclicality: Oil price fluctuations influence customer exploration budgets directly impacting drilling contract volumes.

- Customer concentration: Reliance on few large customers elevates exposure if those customers alter procurement strategy unexpectedly.

- Regulatory pressure: Complex multi-jurisdictional environmental laws increase compliance costs while imposing liability risks; non-compliance could damage reputation or cause contract loss.

- Capital intensity & leverage: Maintaining aging rigs requires significant capital outlays while leverage remains elevated near $5.9 billion net debt posing refinancing risk [F1][S4].

- Supply chain disruptions: Material shortages or logistical delays can hamper rig readiness reducing contracted operational days.

- Labor relations: Expanding unionization or restrictive labor policies could escalate costs or reduce workforce adaptability particularly offshore where specialized crews are essential.

Additionally, pending completion of the Transocean deal introduces uncertainty around execution effectiveness maintaining customer loyalty during control transitions.

What to Watch Next

Investors should monitor:

- Progression of the Transocean merger approvals which will materially affect strategic direction and asset deployment [S7][S18].

- Contract renewal announcements especially among top five customers affecting near term revenue stability.

- Rig utilization rates disclosed quarterly as a proxy for demand strength.

- Day rate trends signaling pricing power amidst changing supply dynamics.

- Regulatory developments particularly new U.S. Gulf safety rules or international environmental mandates altering operating conditions.

- Liquidity management updates indicating refinancing plans or adjustments to capital expenditure budgets addressing leverage concerns.

Close attention to these metrics will provide early signs of valuation inflection points reflecting both sector fundamentals and corporate execution capability.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $578mm | |

| 2026-03-31 | ||

| Current assets | $1205mm | |

| 2026-03-31 | ||

| Current liabilities | $778mm | |

| 2026-03-31 | ||

| Current ratio | 1.55x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Valaris held cash & equivalents of approximately $578 million against current liabilities of $778 million yielding a current ratio near 1.55 suggestive of adequate short-term liquidity [F1]. Current assets stand at $1.2 billion supporting working capital needs but long-term net debt remains substantial around $5.9 billion reflecting ongoing financing obligations stemming from prior fleet investments [F1].[F1]

Operating income for calendar year-end 2025 was recorded at $477 million on revenues totaling $2.37 billion illustrating underlying profitability notwithstanding interim quarterly volatility.[F1] Net income was positive at $983 million for the same period.[F1]

Debt covenants embedded in credit agreements impose operational discipline but may restrict financial flexibility in pursuing opportunistic investments.[S4] Capital expenditure demands for rig maintenance require disciplined cash flow management balancing growth with financial prudence.

This analysis is based on publicly filed SEC documents including the latest Form 10-Q (May 5, 2026) as primary source supplemented by recent news releases up to May 2026 referencing Valaris Ltd’s operating results and corporate transactions. It avoids investment advice focusing instead on foundational business modeling insights relevant for industry participants assessing offshore drilling sector developments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments