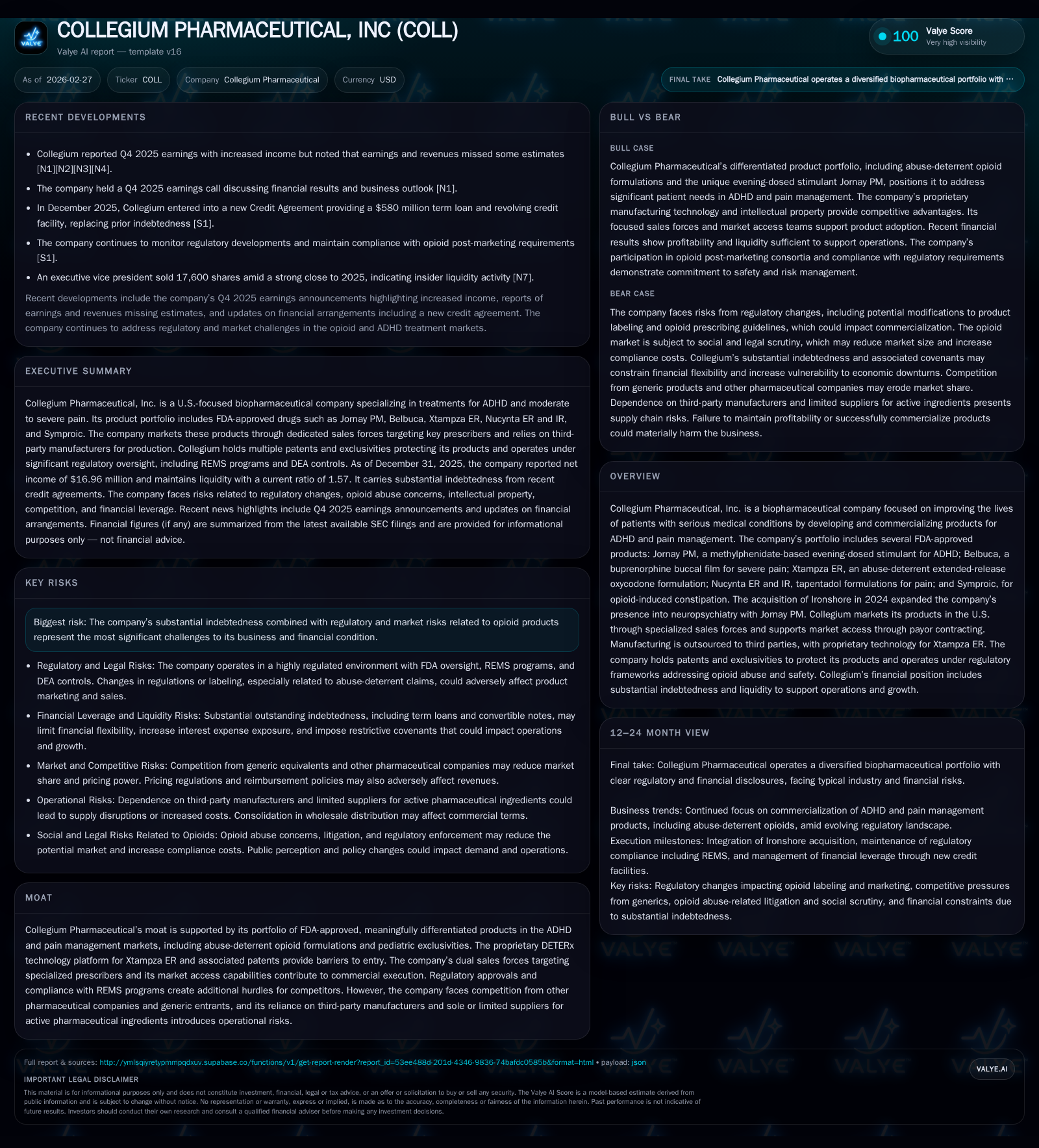

Collegium Pharmaceutical Leverages Niche Portfolio but Faces Regulatory and Debt Pressures

Strong product pipeline and strategic acquisition drive growth amid challenges from opioid regulation and leverage.

Collegium Pharmaceutical has expanded its footprint in ADHD and pain management through acquisitions and proprietary abuse-deterrent technologies. The company posted a significant rebound in operating income and cash flow in 2025, supported by its diversified product lineup including Jornay PM and Xtampza ER. However, ongoing regulatory scrutiny on opioid marketing, industry-wide pricing pressures, and substantial indebtedness constrain future profitability and operational flexibility. Monitoring payor reimbursement trends, legal developments, and supply chain resilience will be critical for assessing its growth trajectory.

Company Overview

Collegium Pharmaceutical operates primarily in the biopharmaceutical space focusing on treatments for ADHD and moderate to severe pain conditions. Its product portfolio includes FDA-approved therapies such as Jornay PM for ADHD — acquired through Ironshore in September 2024 — along with Belbuca, Xtampza ER, Nucynta ER and IR for pain management, and Symproic for opioid-induced constipation. Notably, Jornay PM is unique as the only stimulant dosed in the evening for ADHD treatment approved by the FDA. Xtampza ER uses a patented DETERx technology platform that provides extended-release oxycodone with built-in abuse deterrence through wax-based microspheres designed to thwart physical and chemical tampering.

Historical Financial Performance

From FY2022 to FY2025, Collegium demonstrated a trajectory marked by fluctuations tied to product commercialization advances and strategic acquisitions. Operating income surged from approximately $11.8 million in FY2022 to $61 million by FY2023 before dipping slightly and then achieving a new peak at $60.8 million in FY2025 [F1]. Net income followed a similar pattern: turning positive after losses in FY2022 (-$7.2 million), peaking at $31.9 million in FY2023 but declining to $16.9 million in FY2025 due to costs associated with acquisitions and integration.

Cash flows from operations exhibited robust growth from $124 million in FY2022 to $329 million in FY2025 indicating improvement in working capital management and sales collections. Capital expenditures remained below $2 million annually despite scaling operations. Free cash flow calculated as CFO minus capex was strong at approximately $328 million in FY2025 [F1]. Equity increased steadily from roughly $195 million in FY2023 to over $300 million by FY2025, reflecting retained earnings accumulation despite repurchases.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 17 | 329 | 61 | 1740000 | +35.3% |

| 2024 | 13 | 205 | 38 | 1652000 | -60.8% |

| 2023 | 32 | 275 | 62 | 461000 | +543.7% |

| 2022 | -7 | 124 | 12 | 1622000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 25 | 328 | 5.6 |

| 2024 | 60 | 203 | 5.5 |

| 2023 | 75 | 274 | 16.3 |

| 2022 | 14 | 123 | -3.7 |

Source: SEC companyfacts cache [F1].

Figures reflect operating & net income plus cash flows; revenues are not explicitly disclosed but can be analyzed further when available.

Growth Drivers and Strategic Initiatives

The acquisition of Ironshore enhanced Collegium's market position notably by bringing Jornay PM under its umbrella — allowing geographic expansion into neuropsychiatric indications apart from the traditional pain management focus. This transition introduces an additional specialized sales force leveraged on ADHD prescribers alongside the existing oncology and pain medicine teams.

Proprietary abuse-deterrent formulations like Xtampza ER create differentiation barriers against generic Schedule II opioids; continued promotion of these safety features backed by real-world surveillance data from RADARS® support sustained uptake.

Market access efforts via payor contracts remain central; evolving pharmaceutical pricing reforms led by administrative actions seek deeper rebates or alternative price-setting mechanisms which could cap pricing power but also incentivize preferential formulary placement if properly navigated [S14][S15][S18].

Expansion opportunities lie partially constrained by regulatory environments that govern marketing practices under FDA’s heightened scrutiny especially around opioid promotional claims where missteps risk warning letters or harsher penalties [S22]. Additionally compliance with REMS programs for opioid products increases complexity and cost structure.

Competitively the company faces headwinds as new classes of analgesics such as Vertex's suzetrigine enter the market representing non-opioid alternatives with FDA approval after decades without innovation — challenging reliance on traditional opioid frameworks [S24][S25]. Generic methylphenidate alternatives also pressure Jornay PM’s ADHD market share.

Operational Challenges and Risks

Substantial debt incurred mainly due to acquisitions demands vigilant covenant compliance with outstanding credit agreements carrying variable-cost borrowing linked to SOFR plus significant spreads around ~4.63%. Failure could trigger defaults risking collateral foreclosure [S23]. Interest expense volatility poses earnings pressure.

Manufacturing dependency on limited third-party suppliers potentially risks supply interruptions—particularly given dedicated facilities utilized for abuse-deterrent Xtampza ER—and any shortfall could impose costly delays or non-compliance exposures [S19].

Wholesale distributor consolidation necessitates astute contract negotiation amidst shifting purchasing patterns affecting revenue predictability [S10].

Opioid-related litigation persists albeit with historical settlements concluded; ongoing inquiries from state attorneys general over sales practices exact resource diversion with uncertain ultimate outcomes affecting reputational standing [S6][S13][S16].

Healthcare laws including anti-kickback statutes heavily govern promotional conduct requiring substantial compliance investment; even inadvertent off-label promotion risks false claims liability resulting in financial penalties or restrictions limiting commercial agility [S4][S14][S22].

Returns and Capital Allocation

Return on equity remains modest at approximately 5.6% for FY2025 reflecting moderate profitability balanced against equity base growth including retained earnings reinvestment [F1]. Despite positive net income trends following prior losses there remains scope for improving capital efficiency.

Free cash flow generation is robust partly due to low capital expenditure needs relative to operational cash inflows.

Management has allocated capital toward share repurchases totaling over $25 million in FY2025 after higher levels above $60 million previously—signaling ongoing efforts to return value but possibly tempered amid near-term liquidity focus given leverage considerations [F1]. Dividend payments are not reported indicating retention of earnings likely prioritized toward debt servicing or operational investments.

Key Milestones and What To Watch (Analysis)

- Integration success post-Ironshore acquisition measured by revenue contributions from Jornay PM segment growth.

- Continuing regulatory developments concerning opioid marketing compliance including any FDA warnings or enforcement actions impacting sales strategies.

- Outcomes related to opioid litigation or governmental investigations that could impose fines or restrictions.

- Evolution of payor reimbursement policies especially Medicare/Medicaid coverage levels impacting pricing flexibility.

- Competitor product launches particularly advances in non-opioid analgesics or generic stimulant therapies influencing market share dynamics.

- Management’s approach toward debt reduction or refinancing amid expected interest rate environment changes.

- Supply chain robustness including validation of sole-source manufacturers’ consistency amidst global disruptions.

Conclusion

Collegium Pharmaceutical stands at an inflection expanding beyond pain management into neuropsychiatry via the strategic acquisition of Ironshore while leveraging differentiated abuse-deterrent technologies for opioids that target entrenched markets with unmet needs for safer formulations. The solid financial performance across profitability metrics evidences commercial success although tempered by notable regulatory complexities tied to opioid litigation risk exposure compounded by substantial indebtedness shaping capital allocation decisions.

Navigating increasingly stringent healthcare policies governing drug pricing reimbursement as well as marketing compliance will be critical along with safeguarding supply chains amidst competitive pressures from both generics and emerging non-opioid therapies poised to reshape analgesic treatment paradigms.

This analysis is based on publicly available SEC filings dated up to February 26, 2026 ([F1], [S1]-[S29]) and recent news transcripts.[N1]-[N9] It does not constitute investment advice but provides a detailed overview of Collegium Pharmaceutical's business fundamentals within peer industry contexts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments