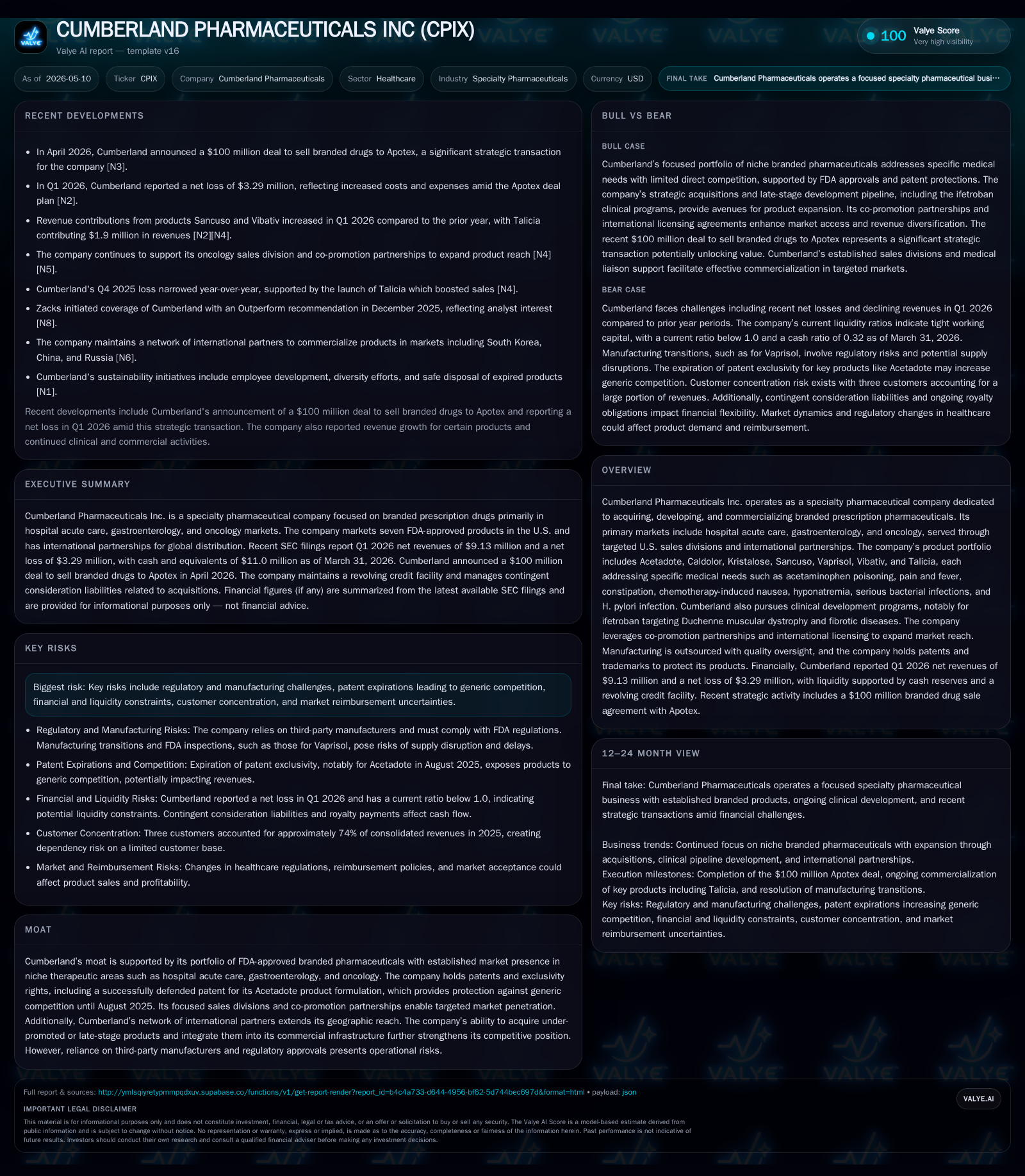

Cumberland Pharmaceuticals Commences $100M Apotex Sale Amid Declining Q1 Revenues

First-quarter revenue pressures and strategic brand portfolio sale define Cumberland's near-term pivot.

In its latest quarterly filing, Cumberland Pharmaceuticals reported a notable revenue decline of 22% year-over-year, reflecting ongoing challenges in its branded pharmaceutical portfolio. Concurrently, the company announced a landmark strategic transaction to sell its branded U.S. commercial businesses to Apotex for $100 million, signaling a significant recalibration of its business model. Cumberland’s specialty focus on hospital acute care, gastroenterology, and oncology has yielded a niche but patchy performance profile, with key products facing mature markets and competitive pressure. Moving forward, growth will hinge on successful clinical pipeline advancement, execution of the Apotex integration, and continued development of international partnerships.

Recent Operating Update

Cumberland Pharmaceuticals’ most recent quarterly filing dated May 8, 2026 reveals several pivotal developments reshaping the company's near-term trajectory [S2]. Net revenues for Q1 fell sharply by approximately $2.58 million (22%) versus the prior year quarter to $9.13 million. The contraction primarily reflects softer demand across its suite of branded prescription pharmaceuticals during intensifying competition and ongoing challenges in prescription volume [S2]. Operating expenses rose notably in selling and marketing (+$0.83 million) and research & development (+$0.16 million), consistent with efforts to support pipeline progression and marketing initiatives despite headwinds [S2].

Parallel with this financial backdrop, Cumberland announced a strategic transaction in early May wherein Apotex, Canada's largest pharmaceutical company, agreed to acquire Cumberland's entire portfolio of FDA-approved branded U.S. products for $100 million cash consideration subject to customary closing conditions including shareholder approval [S3][S7]. This one-shot monetization marks a critical pivot from a commercial-selling enterprise to one potentially focused more on clinical development, pipeline incubation at CET Life Sciences Center, and international partnerships.

Business Model

Cumberland operates as a specialty pharma entity reliant on acquiring, developing, and commercializing branded prescription drugs primarily targeting hospital acute care (e.g., Acetadote for acetaminophen poisoning), gastroenterology (Kristalose for constipation), and oncology supportive care (Sancuso to prevent chemotherapy-induced nausea/vomiting) [S1][S16]. Its revenue is generated from product sales driven by targeted field sales teams focused on concentrated prescriber bases within these specialties in addition to royalties from co-promotion agreements.

Revenue derives from hospital contracts and pharmacies purchasing these FDA-approved products. The company leverages IP assets including patents (recently lost exclusivity for Acetadote in Aug 2025) and regulatory exclusivities that provide limited protection against generics [S1]. Pricing power is modest given Medicaid pricing limitations and competitive generic threats post-exclusivity expiration.

Outsourced manufacturing reduces capital intensity but creates dependency risk; Cumberland retains quality control oversight but does not own production facilities [S1]. Internationally, rights are licensed or assigned selectively (excluding Sancuso) expanding geographic footprint without requiring heavy operational investment.

R&D investment focuses largely on advancing ifetroban—an investigational compound showing promise in Duchenne muscular dystrophy cardiomyopathy and systemic sclerosis—leveraging fast track designation achieved recently for DMD indication [S26]. This mix of marketed brands producing stable cash flow combined with clinical stage development forms the company's strategic operating framework.

Industry Structure and Competitive Position

Operating within specialty pharma niches characterized by relatively small prescriber populations (hospitalists, oncologists, gastroenterologists), Cumberland competes against both generic manufacturers post-patent expiry as well as larger branded pharma companies offering multi-indication portfolios [S1]. The company’s moat rests on niche market focus, moderate patent protection (now abated for Acetadote), targeted salesforce efficiency, and international distribution partnerships.

Competition varies by product: injectable NSAIDs like Caldolor compete with generics/alternatives; Sancuso faces generic granisetron versions despite its transdermal delivery advantage; Vibativ targets resistant bacterial infections in hospital settings facing established antibiotic providers [S1][S18]. As such, Cumberland faces structural pressures from both product lifecycle maturity and reimbursement dynamics typical of hospital acute care pharmaceuticals.

The company's strategy emphasizes acquisition of under-promoted or late-stage products coupled with integrating them into commercial infrastructure—a double-edged sword that can limit scalability but enable focused stewardship [S1]. The announced Apotex sale indicates recognition that scale limitations constrain long-term competitiveness in highly consolidated pharmaceutical markets.

Growth Drivers

- Ifetroban Clinical Development: The company’s Phase II programs targeting rare diseases—Duchenne muscular dystrophy cardiomyopathy and fibrotic diseases like systemic sclerosis—represent growth potential beyond legacy brands. FDA Fast Track designation supports accelerated regulatory review paths [S26].

- International Partnerships: Expanding registration and commercialization outside the U.S., particularly leveraging the Vibativ acquisition partners internationally broadens revenue avenues without direct commercial expense burden [S1][S16].

- Selective Brand Acquisitions: Despite the asset sale plans domestically, Cumberland signals intent to selectively acquire differentiated brands fitting its target specialties to replenish portfolio or secure late-stage assets [S1][S18].

- Pipeline Incubation at CET Life Sciences Center: Early-stage innovation activity co-located at CET offers potential novel candidates feeding into mid-late stage pipelines [S1][S18].

- Cost Discipline Amid Revenue Pressure: Efforts to modulate operating expenses aligned to declining revenues aim to protect positive cash flow generation capabilities under constrained conditions [S2].

Risks and Growth Constraints

- Regulatory Risks: FDA approvals remain uncertain for ifetroban indications along with any new product candidates. Changes in drug pricing policy or reimbursement could materially impact profitability.

- Patent Expiry / Generic Competition: Loss of exclusivity on core products (Acetadote expired Aug 2025) exposes revenues to erosion via cheaper generics across all major brands.

- Operational Execution: Transitioning commercial U.S. business integration following Apotex acquisition presents execution risk including employee retention disruptions.

- Liquidity Pressure: Working capital was negative at March quarter-end ($-1.7 million) with current ratio around 0.95 despite $11M cash reserve; reliance on revolving credit facility expiring October 2026 necessitates refinancing or strengthening cash flows [S2][F1].

- Customer Concentration: With sales focused in specialized hospital segments regulatory/reimbursement disruptions or shifts at major buyers could have outsized impacts.

- Supply Chain Reliance on Third Parties: Contract manufacturing arrangements limit control over production timelines or costs.

What to Watch Next

- Completion of the Apotex transaction contingent upon shareholder approval scheduled likely in mid-2026 - critical milestone defining firm’s structural shift [S7][N2].

- Clinical progress updates or data readouts from ifetroban Phase II studies addressing Duchenne muscular dystrophy cardiomyopathy and fibrotic indications impacting future value creation potential [N3][S26].

- Execution of cost controls amid transitioning commercial model post-Apotex sale impacting EBITDA trends.

- Management commentary during next earnings releases regarding liquidity strategies especially line-of-credit renewal or alternative financings ahead of October 2026 term end [S6][F1].

- International partnership expansion progress especially new market approvals for Vibativ strengthening multinational revenues.

Financial Profile Highlights (Q1 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $11mm | |

| 2026-03-31 | ||

| Total debt | 0 USD | |

| 2025-12-31 | ||

| Net debt | $-11mm | |

| 2025-12-31 | ||

| Current assets | $33mm | |

| 2026-03-31 | ||

| Current liabilities | $34mm | |

| 2026-03-31 | ||

| Current ratio | 0.95x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Cash & Cash Equivalents | $11,007,245 | |

| 2026-03-31 | ||

| Current Assets | $32,789,257 | |

| 2026-03-31 | ||

| Current Liabilities | $34,488,051 | |

| 2026-03-31 | ||

| Current Ratio | 0.95 | |

| 2026-03-31 | ||

| Total Debt | $0 | |

| 2025-12-31 | ||

| Revolving Credit Availability | ~$25M (up to $25 million facility, $20 million initially drawn) | |

| 2026-03-31 |

Liquidity remains supported predominantly by roughly $11 million cash reserves supplemented by an undrawn revolving credit line up to $25 million expiring October 2026 but not yet tapped significantly during Q1 [F1][S2][S6].

Net loss pressured by revenue declines will continue until either clinical assets mature or the new ownership structure post-Apotex fully materializes operational synergies.

This analysis relies solely on publicly filed SEC documents through May 8th, 2026 and widely reported news items up through May 10th, 2026. It does not constitute an investment recommendation but intends to provide an informed perspective rooted in available disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments