Cardiff Oncology’s Onvansertib: Clinical Advances and Capital Challenges

The dual narrative of clinical progress with onvansertib contrasts with operational and governance hurdles amid cash burn pressures.

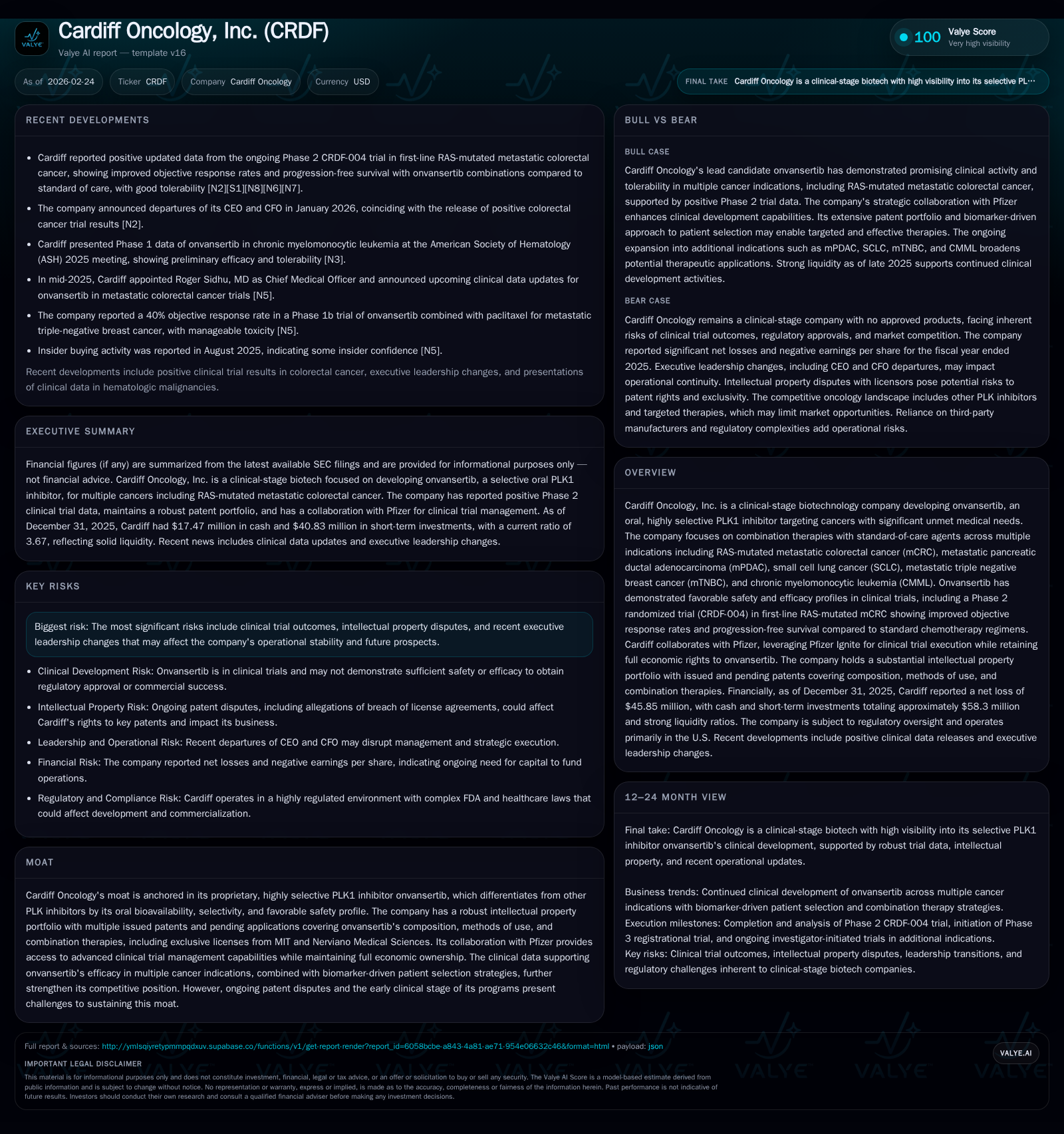

Cardiff Oncology is advancing its oral, highly selective PLK1 inhibitor, onvansertib, across multiple oncology indications with promising Phase 2 trial data in RAS-mutated metastatic colorectal cancer demonstrating improved objective response rates and progression-free survival. Despite scientific progress and a collaborative relationship with Pfizer Ignite enhancing clinical trial execution, Cardiff faces significant operational headwinds highlighted by recent CEO and CFO departures, persistent operating losses exceeding $48 million annually, and increasing R&D expenditures. The company maintains a solid intellectual property portfolio but operates amid patent disputes and regulatory risks that may constrain commercialization timing. Key upcoming milestones include finalizing Phase 3 trial designs and data readouts across pancreatic, lung, breast cancers and leukemia.

Historical Growth Trajectory and Operational Drivers

Over recent years, Cardiff Oncology's revenues have been modest but showed growth from $245 thousand in FY2019 to $366 thousand in FY2020, reflecting initial expansion of clinical activities. Although revenue data beyond FY2020 is not explicitly disclosed annually, the company reported approximately $86 thousand by September 2021, suggesting continued growth likely tied to collaboration milestones or service fees related to Pfizer partnership [F1].

Despite this revenue increase, operating losses have remained substantial and relatively stable, ranging from -$40 million in FY2022 to nearly -$49 million by FY2025. This reflects ongoing intensive investment in research & development primarily focused on advancing onvansertib across multiple oncology indications [F1].

Operating cash flow burn approximated $38 million in FY2025, consistent with sustained clinical program expenditures. Capital expenditures were minimal at about $44 thousand in FY2025, underscoring the company's focus on clinical development over fixed asset investment.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -46 | -38 | -49 | 44000 | -0.9% |

| 2024 | -45 | -38 | -49 | 80000 | -9.6% |

| 2023 | -41 | -31 | -45 | 582000 | -7.1% |

| 2022 | -39 | -34 | -40 | 1006000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -38 | -101.0 |

| 2024 | -38 | -54.8 |

| 2023 | -31 | -59.4 |

| 2022 | -35 | -36.4 |

Source: SEC companyfacts cache [F1].

Note: Revenues after FY2020 are not disclosed explicitly; YoY net income % omitted due to incomplete data.

This financial profile is typical for clinical-stage biotechs prioritizing pipeline advancement over near-term profitability.

Onvansertib’s Differentiation in Targeted Cancer Therapy

Onvansertib is Cardiff Oncology's lead compound — an oral small molecule inhibitor highly selective for Polo-like kinase-1 (PLK1), a validated target in oncology involved in mitotic regulation. It distinguishes itself by an IC50 of approximately 2 nM against PLK1 with negligible activity against related kinases PLK2/3 (>10 µM IC50), contrasting with prior pan-PLK inhibitors such as volasertib which exhibited broader kinase inhibition linked to safety concerns [S1][S25].

The drug's pharmacokinetics feature a ~24-hour half-life enabling flexible dosing schedules combined with oral bioavailability facilitating patient convenience. Preclinical studies demonstrate synergistic anti-tumor effects when combined with various chemotherapies including irinotecan-based regimens FOLFIRI or FOLFOX plus bevacizumab as well as targeted agents like PARP inhibitors [S1][S24].

Cardiff's collaboration with Pfizer Ignite enhances trial management efficiency while preserving full economic rights over onvansertib development [S19].

Clinical Trial Developments and Recent Positive Data

The pivotal Phase 2 CRDF-004 trial evaluates two doses of onvansertib (20 mg & 30 mg) combined with standard-of-care chemotherapy regimens versus standard-of-care alone for first-line treatment of patients harboring RAS mutations (KRAS or NRAS) in metastatic colorectal cancer—a population representing over half of CRC cases [S16][N1].

Recent results indicate:

- The higher dose arm achieved an Objective Response Rate of approximately 72%, markedly above the ~43% observed for SoC alone.

- Progression-Free Survival medians were not reached; hazard ratios suggested substantial risk reduction (~HR=0.37).

- Safety profiles confirmed tolerability without unexpected toxicities.

These data support accelerated approval pathways as discussed with FDA at a June 2023 Type C meeting where seamless Phase III designs using ORR as interim endpoints were deemed acceptable pending confirmatory outcomes such as PFS [N1][S29].

Additional investigator-initiated trials explore efficacy signals across metastatic pancreatic ductal adenocarcinoma combined with NALIRIFOX regimen; relapsed small cell lung cancer monotherapy showing disease control rate around 57%; triple-negative breast cancer; and chronic myelomonocytic leukemia [S23][S24].

Leadership Changes and Strategic Implications

In early 2026 Cardiff announced departures of both CEO and CFO amid positive trial data releases causing share price volatility and raising governance concerns during critical development phases [N1][S3].

Such turnover may impact strategic continuity especially as the company approaches registrational Phase III trials requiring coordination across regulators, investors and partners.

Financial Profile: Persistent Losses Amid Rising R&D Investment

Operating losses near $49 million annually reflect ongoing heavy spending to advance clinical programs without commercial revenues yet realized. Net income trends mirror these losses resulting in negative approximate return on equity exceeding -100% given shrinking equity base ($45 million end-FY25 down from $83 million end-FY24) [F1].

Operating cash flows remain deeply negative (~$38 million annually) consistent with cash-intensive clinical development activities while capital expenditures are minimal.

Cash & equivalents stood at about $17 million at year-end FY2025 against current liabilities near $16 million indicating liquidity exists but runway remains limited without additional financing sources.

No dividends have been declared or paid; share repurchases have not occurred recently — last notable buybacks date back over a decade ago — aligned with typical early-stage biotech capital allocation practices focused fully on pipeline investment [F1].

Pipeline Outlook and Upcoming Milestones

Key near-term catalysts include finalizing Phase III study design following CRDF-004 results under FDA guidance alongside continued enrollment and data readouts from investigator-sponsored studies in pancreatic cancer (mPDAC), small cell lung cancer (SCLC), triple-negative breast cancer (TNBC), and chronic myelomonocytic leukemia (CMML) [S23][N1].

Management has not provided explicit revenue or approval guidance nor definitive timelines for regulatory submissions.

Intellectual Property Positioning and Regulatory Risks

Cardiff holds an extensive intellectual property portfolio comprising over fifty issued patents plus sixty-five pending applications covering composition of matter for onvansertib along with methods of use including combination therapies targeting KRAS-mutated mCRC extending exclusivity into the early 2040s [S19].

Patent challenges represent a material risk potentially affecting commercialization timing or scope.

Regulatory risk spans compliance requirements throughout drug development lifecycle per FDA statutes including IND submissions through post-marketing surveillance. Additionally exposure exists under U.S. healthcare fraud statutes such as the Anti-Kickback Statute and False Claims Act imposing significant penalties if violated . Privacy laws including HIPAA also govern patient data protection during trials complicating international data sharing frameworks [S8].

Ongoing vigilance regarding evolving enforcement environments is necessary to mitigate legal/regulatory risks impacting market access.

This analysis reflects information publicly available through February 2026 without providing investment advice or price targets. Readers should consult original filings before making investment decisions related to Cardiff Oncology.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments