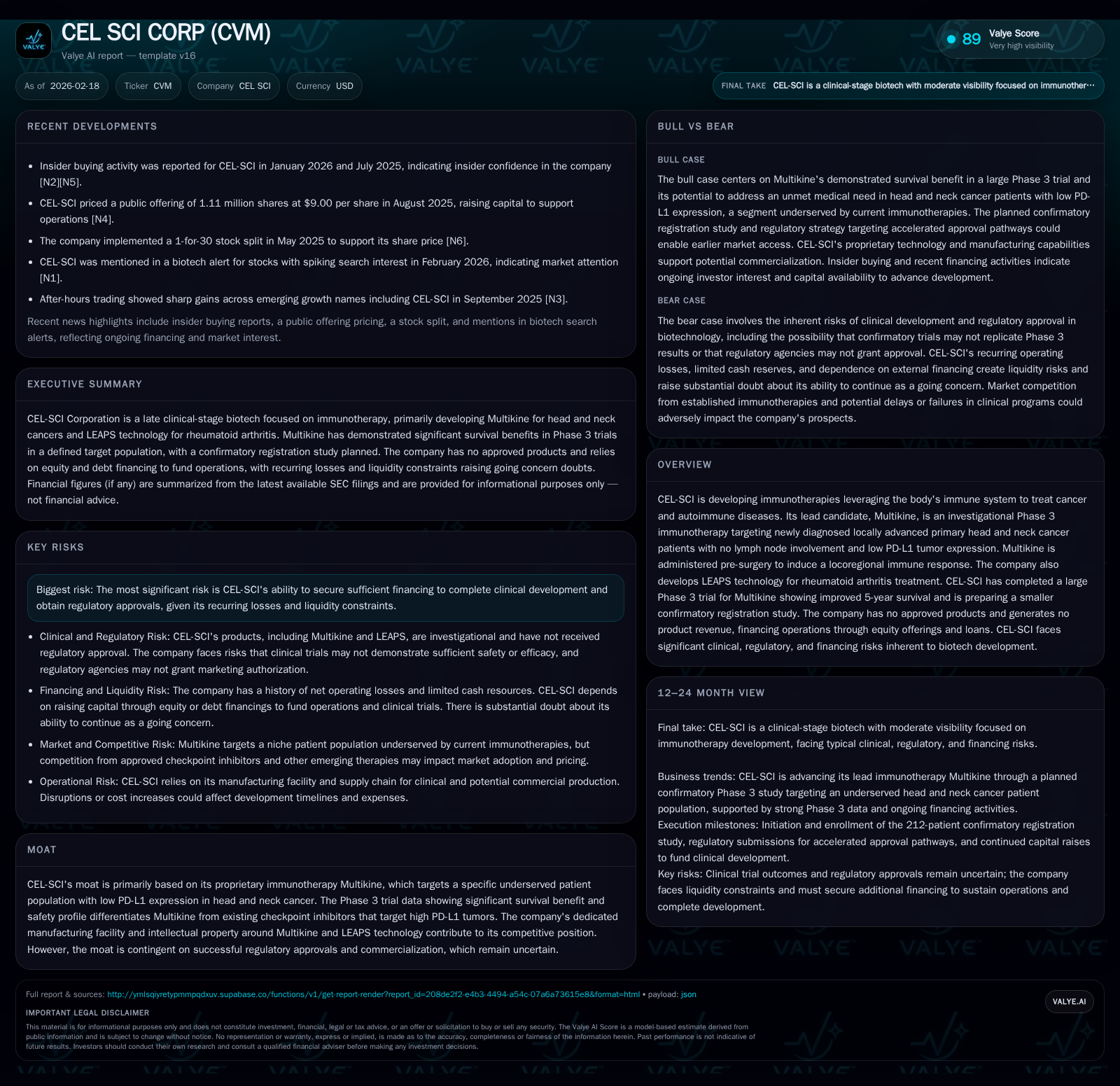

CEL-SCI's Strategic Gamble on Multikine Spurs Financial Strain and Regulatory Hurdles

CEL-SCI pursues regulatory approval of its novel pre-surgical immunotherapy Multikine while facing ongoing financial constraints and capital market dependence.

CEL-SCI Corp centers its biotechnology development on Multikine, an investigational immunotherapy targeting a specific subset of head and neck cancer patients. Despite promising Phase III data showing significant survival benefits, the company generates no product revenue and continues to operate at substantial operating losses. Its financial health remains precarious, hinging on successful capital raises to fund an upcoming confirmatory registration study with an estimated $30 million cost. Regulatory approval pathways are laden with typical biotech uncertainties, compounded by the company's liquidity challenges and absence of commercial products.

Tracing CEL-SCI’s Financial and Clinical Trajectory

CEL-SCI Corp has consistently operated without revenue generation from product sales. Its financial performance over recent fiscal years reveals substantial operating losses closely tied to its research and development (R&D) efforts on Multikine. From FY2022 through FY2025, operating income losses remained steep but displayed slight improvement; for instance, FY2025's net operating loss totaled approximately $24.8 million versus $26.4 million in FY2024 [F1], reflecting incremental operational efficiencies amid ongoing clinical investments.

The company owns a dedicated manufacturing facility, critical for producing Multikine given its biologic nature. This asset supports the clinical stage trials by ensuring proprietary control over production quality—a key strategic advantage in oncology biologics development [S1]. The absence of revenues enforces reliance on capital infusions to sustain operations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -25 | -17 | -25 | 38109 | +7.9% |

| 2024 | -28 | -19 | -26 | 94875 | +14.3% |

| 2023 | -32 | -23 | -31 | 361892 | +12.3% |

| 2022 | -37 | -18 | -36 | 637892 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -17 | -159.2 |

| 2024 | -19 | -214.3 |

| 2023 | -23 | -243.6 |

| 2022 | -19 | -114.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue data unavailable post-2017 due to no reported product sales; ROE approximated by net income divided by stockholders’ equity [F1].

Multikine’s Clinical Milestones and Differentiation in Immuno-Oncology

Multikine is CEL-SCI’s flagship investigational drug candidate—a leukocyte interleukin-based immunotherapy aiming to modulate the immune system pre-surgery in newly diagnosed locally advanced primary head and neck squamous cell carcinoma (HNSCC) patients who lack lymph node involvement (N0 status via PET imaging) and exhibit low PD-L1 tumor expression based on biopsy assays [S2]. This targeted demographic diverges from checkpoint inhibitors like pembrolizumab (Keytruda), which primarily benefit high PD-L1 expressors.

The Phase III pivotal trial enrolled approximately 928 patients worldwide by September 2016 and reached its primary endpoint with database lock in December 2020 [S1]. Unblinded results announced June 2021 revealed a pronounced overall survival benefit—five-year survival was elevated to roughly 73% versus about 45% in the standard-of-care control group within this specified population [S2][S24]. The hazard ratio was reported at approximately 0.35 (95% confidence interval upper bound at about 0.66), indicating a markedly reduced risk of death.

Critically, Multikine operates as a frontline immunotherapy administered before surgery to induce a locoregional immune response within the tumor microenvironment when immune intervention may be most effective at priming host defenses against residual disease progression [S2]. This timing contrasts with typical post-surgical administration of checkpoint inhibitors.

A confirmatory randomized controlled registration trial focusing exclusively on this target population is planned with FDA concurrence [S2][S24]. The planned sample size is approximately 212 patients intending to validate efficacy endpoints faster than the original larger trial [N1]. Success in this narrower enrollment cohort can leverage accelerated or conditional approval mechanisms acknowledging unmet medical need for low PD-L1 HNSCC subsets otherwise underserved by current therapies.

Dissecting Recent Research & Development Spending Trends

Total R&D expenses decreased from roughly $18.2 million in FY2024 to $15.9 million in FY2025 (-13%), driven predominantly by lower stock-based compensation costs dropping from about $2.9 million to under $0.9 million due to forfeitures and decreased option valuations amid share price shifts [S1][S3]. However, clinical trial expenses exhibited a modest increase signaling preparation activities for the confirmatory registration study; clinical trial costs increased from approximately $315K to $615K year over year.

Personnel-related costs remained relatively steady around $5.9 million annually [S3]. Supply chain expenses for materials used in manufacturing showed slight increases reflecting scale-up needs ahead of confirmatory trials [S7].

LEAPS platform-related expenses reflect early-stage development shifts with negative R&D expenses attributed to cost reversals mostly completed by FY2025 [S9], emphasizing that the bulk of corporate R&D now concentrates on Multikine.

These trends underscore CEL-SCI’s prioritization of advancing Multikine as its clinical centerpiece while managing expense structure amidst limited operational cash flow [S7].

Navigating Regulatory Pathways and Confirmatory Trials Ahead

Regulatory progress centers on initiating a randomized controlled confirmatory Phase III registration study focused on approximately 212 newly diagnosed locally advanced primary HNSCC N0 patients exhibiting low PD-L1 expression measured via biopsy combined with PET scans confirming nodal status [N1][S2][S24]. This trial aims to build upon robust retrospective Phase III data by prospectively validating survival benefit aligned with FDA feedback received circa mid-2024.

The total projected cost for this smaller pivotal study is roughly $30 million [S4][S5], underscoring considerable capital demands ahead—raising capital is prerequisite before enrollment launch.

CEL-SCI has also filed for Breakthrough Medicine Designation with Saudi Arabia’s SFDA via a local pharmaceutical partner—highlighting global regulatory ambitions beyond North America and Europe that may accelerate patient access timelines if approved [S1][S27].

As with biologics targeting oncology patients with distinct immune profiles, regulatory agencies weigh benefit-risk particularly carefully given novel presurgical administration timing compared to established therapeutic sequences among checkpoint inhibitors that primarily target post-surgical or metastatic populations expressing high PD-L1.

Regulatory unpredictability inherent in new drug applications remains acute where historical precedent for accelerated approvals hinges on strong surrogate endpoints; CEL-SCI’s extensive survival data alongside safety signals offers compelling evidence but confirmation through additional trials remains mandatory.

Financial Footing: Liquidity Pressures and Capital Market Reliance

At fiscal year-end September 30, 2025 CEL-SCI exhibited a current ratio near healthy levels (~1.39), denoting moderately sufficient short-term asset coverage over liabilities; however cash flow statements reveal persistent negative operating cash flow averaging nearly $17 million annually since FY2022 [F1][S4].

Capital expenditures have sharply declined from above $600K at peak investment phases toward just below $40K most recently—a normalization consistent with facility completion stages but offsetting high burn rates due to clinical program demands [F1][S3].

Financing strategies historically include public equity offerings complemented by convertible debt issuances alongside warrant exercises yielding incremental proceeds during favorable market conditions [S4][S5]. Despite raising approximately $25 million net proceeds in FY2025 alone via financing mechanisms stated above [F1], CEL-SCI recognizes substantial doubt about going concern status given recurring cash deficits absent product revenues [S12].

Short-term loans are deployed opportunistically but cannot substitute sustained equity or partnership transaction inflows essential to fund multi-year confirmatory trials alongside administrative overheads [S20]. This dependence underscores exposure to volatile capital markets fluctuating risk appetites common across biotech players without commercial assets.

Capital Allocation Patterns: Understanding the Absence of Dividends and Buybacks

CEL-SCI maintains no dividend policy nor engages in share repurchase programs reflective of its early-stage development lifecycle wherein available capital funds purely support ongoing R&D rather than returning cash to shareholders [F1][S23][S28].

The company’s reported book equity has shrunk sharply from over $32 million in FY2022 down toward $16 million as net losses accumulate [F1], translating into approximate negative return on equity exceeding -150%, internally coherent for firms reinvesting all valuations into pipeline advancement rather than profitability transitions.

Stock-based compensation constitutes material non-cash expense utilized principally as employee retention incentives aligned with long-term performance goals rather than cash distributions [S23].

This allocation strategy represents standard biotech practice where commercial traction has yet to begin constraining operating leverage metrics.

Investment Watchlist: Upcoming Catalysts and Risks

Key milestones warranting close monitoring include successful securement of near $30 million capital required to initiate the confirmatory registration study expected approximately within next fiscal quarters contingent upon market conditions [N1]. Enrollment metrics will matter equally due to tight patient eligibility criteria anchored on lymph node negativity confirmed through advanced PET imaging protocols alongside low PD-L1 biopsied tumors [S21][S24].

Additional pivotal catalysts encompass regulatory interactions leading toward possible conditional or accelerated approvals either after full enrollment or interim analyses that may validate benefit-risk ratios faster than standard submissions by agencies such as FDA or EMA [N1][S27].

Risks center notably around CEL-SCI’s capacity to raise sufficient funds timely amid fluctuating biotech investor appetite and general macroeconomic pressures impacting equity issuance windows [N2]; history shows such companies often face delays or dilutions absent clear positive readouts.

Clinical risks abound per typical industry patterns where despite promising signal-to-noise phase III data reflected statistically significant hazard ratios less impressive outcomes could emerge amid prospective studies or regulatory reviewers may require extended follow-ups adding temporal uncertainty [S11][S24].

Interestingly some insider buying reported recently suggests cautious optimism among management stakeholders regarding progress against these hurdles despite prevailing external uncertainties [N2].

This report summarizes key facets relating to CEL-SCI Corp's business model focused exclusively on currently disclosed information without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments